The truth will set you free? Perhaps – or perhaps it will disillusion you.

In late August, Federal Reserve Chair Jerome Powell issued a hawkish update at the Jackson Hole Symposium. Powell was brutally honest on the subject of inflation, more so than anyone had thought he would be beforehand. Powell said, simply, that neither inflation nor higher interest rates are going away any time soon.

The markets did what they are wont to do when faced with unwelcome news – they crashed across the board. However, that drop opens up the opportunity for investors willing to do a bit of bottom fishing.

For now, the Street’s analysts are up to the challenge, tagging the stocks that should be on investors’ ‘buy lists’ this fall. We’ve looked up the details of two of those stocks on the TipRanks database; they’re Strong Buy-rated, and show plenty of upside in the current conditions.

PGT Innovations (PGTI)

We’ll start in the construction sector, where PGT offers a specialized product that meets a need: impact resistant, energy efficient, door and window systems. The company advertises its products as a way to ‘be ready’ and to ‘be safe;’ and promotes their ability to protect customers’ homes from wind damage due to all types of storms, from spring thunderstorms to Atlantic hurricanes. PGT operates through a line of 8 brand-name window and door makers, offering solutions for a full range of entry-related issues: ease of access, energy and insulation efficiency, and impact resistance and storm protection.

Homeowners are always keen to protect their property, and this has helped to push PGT’s revenues and earnings up over the past year or more. The company has seen 6 quarter-over-quarter gains in a row, and the most report, for Q2 of fiscal 2022, the quarter ending on July 2, showed a top line of $407 million. This was up 42% year-over-year. Net income grew even more, rising an impressive 240% y/y to reach $36 million as Adj. EPS came in at $0.67 – up from the $0.18 reported in the same period last year.

Covering PGTI shares for Deutsche Bank, analyst Joe Ahlersmeyer sees a clear path forward for the company, writing: “Sales growth should persist despite national new construction slowdown. PGTI’s R&R exposure can be considered ‘discretionary non-discretionary’ as homeowners make choices to prevent repairs later. And while we’re less bullish on California’s new resi outlook, markets like Arizona, Texas and Florida should outperform.”

“Bottom line, we are bullish on growth and margins for this business given favorable R&R exposure, structural tailwinds related to home hardening (Southeast) and outdoor living (Western) and are encouraged by near-term momentum displayed in recent results,” Ahlersmeyer summed up.

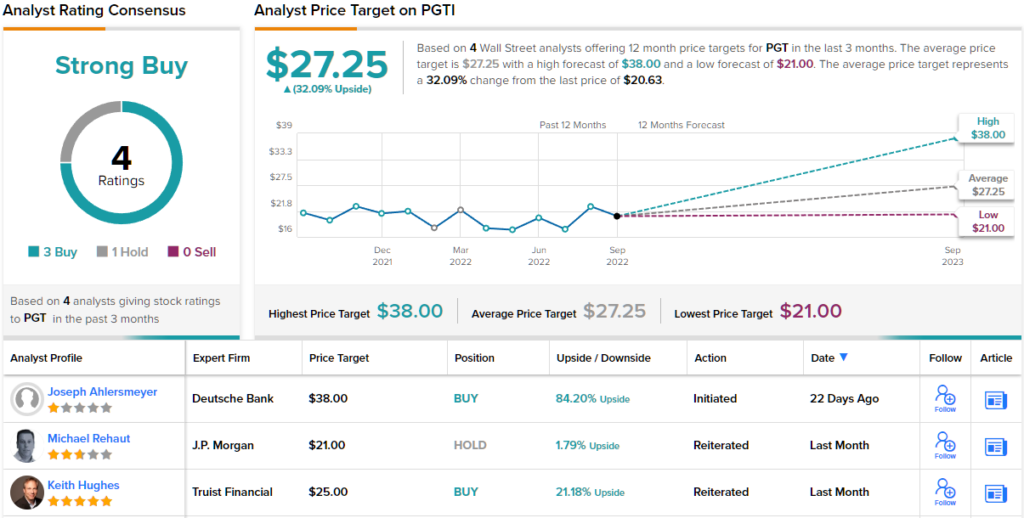

To this end, Ahlersmeyer rates PGTI shares a Buy, and supports that with a $38 price target, indicating potential for an 84% upside in the year ahead. (To watch Ahlersmeyer’s track record, click here)

Overall, this specialty construction firm has picked up 4 recent analyst reviews, and they break down 3 to 1 in favor of Buys over Holds, for a Strong Buy consensus rating. The shares are priced at $21.53 and their $27.25 average price target implies a gain of 32% in the next 12 months. (See PGTI stock forecast on TipRanks)

MoonLake Immunotherapeutics (MLTX)

For the next stock we’ll shift our focus to the biopharmaceutical realm. MoonLake Immunotherapeutics is a new company in the clinical-stage research world. MoonLake kick-started itself into the public eye earlier this year, when it went public on the NASDAQ through a SPAC transaction. The business combo, with Helix Acquisition, was completed in April and raised approximately $230 million in new capital for the company’s research projects.

The SPAC transaction coincided with MoonLake’s in-licensing of Sonelokimab, a tri-specific investigational nanobody currently being evaluated as a treatment for inflammatory diseases of the skin and joints. MoonLake acquired the license from pharma giant Merck.

Sonelokimab is currently undergoing several human clinical trials, with the two most advanced being for the treatment of psoriasis and hidradenitis suppurativa. The psoriasis track is currently ready to advance to Phase 3 trials, based on positive data from the earlier Phase 2b study, while the hidradenitis suppurativa track began its Phase 2 trial in May of this year. The trial aims to enroll as many as 200 patients.

Analyst Thomas Smith covers MoonLake for SVB Securities and sees this company with a clear path forward based on its solid research program.

“We view SLK development as relatively de-risked, based on compelling Phase 2b results in psoriasis (PsO)… Overall, we see pipeline-in-a-product potential for sonelokimab and believe MLTX can leverage the drug’s differentiated attributes and innovative clinical development strategies—informed by the experiences with bimekizumab and other IL-17 antibodies—to effectively showcase SLK’s optimal balance of efficacy and safety across multiple inflammatory conditions,” Smith opined.

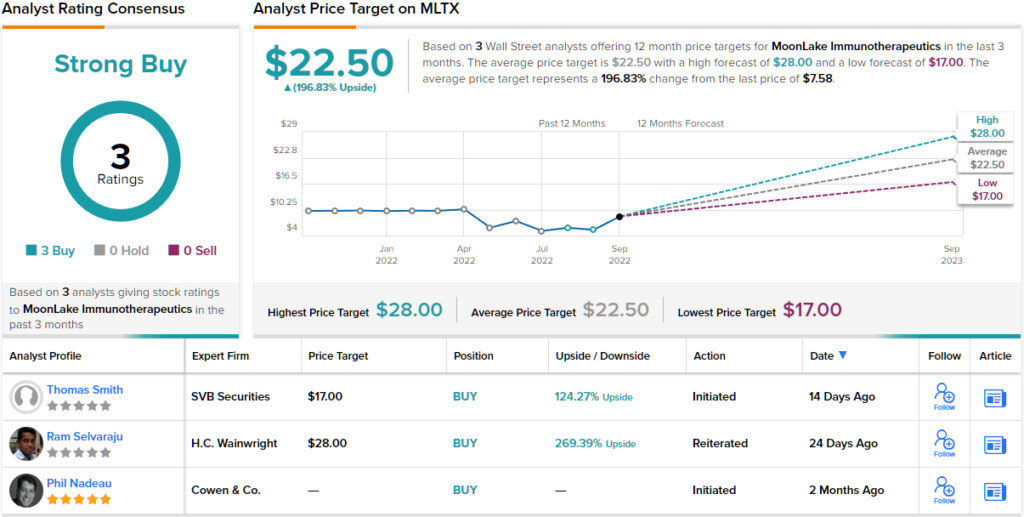

In-line with his optimistic commentary on the company’s program, Smith rates MoonLake shares an Outperform (i.e. Buy), with a $17 price target to suggest a 124% upside in the coming year. (To watch Smith’s track record, click here)

The Strong Buy consensus rating on these shares is unanimous, based on 3 recent positive analyst reviews. The stock’s average price target of $22.50 implies a robust 197% upside from the current trading price of $7.58. (See MoonLake stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.