General Dynamics (GD) is one of a handful of prominent aerospace and defense companies in the United States, specializing in high-end development, engineering, and manufacturing of state-of-the-art solutions, primarily for the U.S. government and its allies.

Specifically, 70% and 10% of the company’s consolidated revenue last year was from the U.S. government and non-U.S. government customers (allies), respectively. The remaining 12% and 8% were from U.S. and non-U.S. commercial customers, respectively.

General Dynamics’ expansive portfolio of products and services contains business aviation, shipbuilding, land combat vehicles, weapons systems, munitions, as well as technology services.

The company’s competitive advantage, besides its proprietary technologies in the above products and services, lies in each of its business units being responsible for optimizing its own operating results. As a result, the company functions with minimal friction and considerable flexibility when it comes to each division’s CapEx and all-around capital allocation needs.

On the one hand, the company numbers several other qualities, including an exceptional track record of capital returns and shareholder value creation. Further, being a defense contractor, General Dynamics is set to benefit from the current, unfortunate war in Ukraine.

On the other hand, with the stock’s valuation hovering at relatively elevated levels, investors’ total-return prospects moving forward could be somewhat limited. Accordingly, I am neutral on the stock.

Current Trading Landscape

Aerospace & defense contractors like General Dynamics are currently experiencing strong tailwinds as a result of the ongoing unfortunate war in Ukraine. As Western governments keep providing Ukraine with all types of weaponry and relevant equipment, companies in the space are set to grow their backlogs and future revenues.

The current situation should not be a temporary event, as Western allies will eventually need to restock their arsenal due to the constant deliveries, which in military terms could imply years’ worth of future backlog for contractors. In fact, in its Q4 earnings call (prior to the war’s outbreak), General Dynamics’ CEO had noted that demand for combat vehicles in Eastern Europe has been at elevated levels for quite some time now.

This just goes to show that defense contractors usually benefit prior, during, and after a conflict, which means that the current war could translate to prolonged tailwinds for the company.

Recent Performance

General Dynamics’ most recent results once again exhibited the company’s mastery of successfully meeting its order backlog and producing resilient financials.

Quarterly revenues remained flat at $9.4 billion, though earnings per share rose 5.6% year-over-year to $2.63. Note that since General Dynamics is a defense contractor, revenue growth is not much of a meaningful metric. Investors should mostly pay attention to General Dynamics’ ability to extend its backlog and its all-around capabilities to deliver on it.

As far as the backlog develops, the company’s revenues and profitability should gradually do as well, as has been the case historically.

Indeed, General Dynamics’ order book growth momentum remains quite strong, with the company reporting a book-to-bill ratio of roughly 1.7x. What this means is that General Dynamics’ cash flows over the next 1.5 to two years should be relatively secured by its customers, provided, of course, the company delivers these projects.

Overall, as long as General Dynamics’ backlog growth foregoes its delivery volumes, the book-to-bill ratio should remain healthy. Thus, the company’s medium-term revenues should remain rather predictable as well. With the ongoing war in Ukraine presumably to lead to increased military budgets moving forward, this should most likely continue to be the case.

Dividends & Valuation

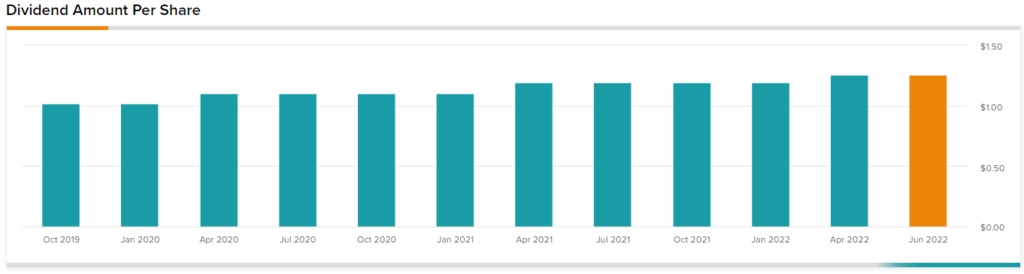

Due to General Dynamics’ book-to-bill ratio remaining healthy historically, as I mentioned earlier, the company’s performance features little to no volatility. This has enabled General Dynamics to grow its capital returns gradually over time. Particularly, the company exhibits an impressive dividend growth track record, counting 27 years of consecutive annual dividend hikes.

This places the company amongst the elite constituents of the S&P 500’s Dividend Aristocrat Index. The company features a five-year dividend growth CAGR of 9.13%, which is rather noteworthy considering how mature General Dynamics’ dividend growth record is. The most recent dividend increase was also quite substantial, raising the quarterly payout rate by 5.9% to $1.26. The stock currently yields close to 2.15%.

Management did not update its guidance, which targets full-year revenues to be between $39.2 billion and $39.45 billion. EPS is also expected to be between $12.00 and $12.15 for Fiscal 2022. The midpoint of management’s ESP outlook suggests that the stock is currently trading at a forward P/E of 18.8x at its current price levels. On an NTM basis, this figure drops to under 18x.

While this seems like a relatively fair valuation considering the macro environment for the aerospace & defense industry appears quite bright, the current multiple is at the high-end of the stock’s historical forward P/E range.

Wall Street’s Take

Turning to Wall Street, General Dynamics has a Strong Buy consensus rating based on seven Buys and two Holds assigned in the past three months.

At $275.67, the average General Dynamics stock projection implies 21.5% upside potential.

Takeaway

On the one hand, Mr. Market likely forecasts above-average EPS growth in the coming years due to the ongoing tailwinds benefiting the industry. The market’s enthusiasm is confirmed by the stock’s premium valuation and the confident price target, which even implies notable upside potential from here.

On the other hand, as we mentioned earlier, the company’s results are derived from its backlog and its ability to deliver on it. Thus, even if the backlog expands going forward, which is certainly positive news, General Dynamics’ production capabilities are likely to only increase at a softer pace each and every year.

Based on the company’s historical growth rates and valuations, current trading environment, most recent results, and outlook, I would consider shares more reasonably valued at a forward P/E of roughly 17.

Thus, while General Dynamics remains a quality company with a strong case in its ability to keep delivering robust shareholder value creation over the long run, investors should consider that its short-term upside could be likely exhausted at the stock’s current price.