Cava Group (NASDAQ:CAVA) stock more than doubled out (117%) of the gate, as its shares went live on the NYSE on Thursday. Indeed, investors seemed to be starved for a tasty IPO amid the market’s recovery, but at these heights, investors would likely be better off taking a bite out of almost any other restaurant stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

For those unfamiliar with Cava, it’s a Mediterranean-themed fast-casual restaurant that’s been a hit among many consumers. Some may be inclined to compare it to the likes of Chipotle Mexican Grill (NASDAQ:CMG), which has been a sensational performer over the decades. Undoubtedly, if Cava is the next Chipotle Mexican Grill, the stock may stand to double up again, perhaps many times over.

The big debut of Cava Group was applaud-worthy, but a tad on the euphoric side. It’s been a while since we’ve had such a red-hot IPO. Also, although stocks seem to be back into bull market mode, I’m not one to believe that the booming debut of Cava will end well for investors looking to punch their ticket at near $40 per share.

Though I am a fan of Cava, the business, I’m not one to chase IPOs after a boom. Those keen on the name may wish to take a raincheck and let the stock come back down to Earth. IPOs can bust as quickly as they boom. So, those patient enough to wait for things to settle down may be in a great spot to get a better entry point. However, at this juncture, it’s doubtful that the IPO price will be hit anytime soon.

Therefore, in this piece, we’ll use TipRanks’ Comparison Tool to look at two other restaurant stocks with a better risk/reward ratio as the economy looks to steer into a recession year.

1. Domino’s Pizza (NASDAQ:DPZ)

Domino’s Pizza was a former Bill Ackman holding that he sold out of almost a year ago. Ackman’s sale turned out to be well-timed, as DPZ stock eventually shed nearly half of its value from peak to trough. The pandemic lockdown days of ordering pizza day after day seem to be over.

Call it a post-lockdown pizza delivery hangover, if you will, but I do believe it’s nearly over after more than a year of post-pandemic levels of normalcy. That’s why I’m staying bullish on Domino’s stock, as I think the top carryout play has room to run once the pizza appetite normalizes.

On Cava’s big debut day, Domino’s stock rocketed more than 6% higher, thanks to a timely upgrade from Stifel, which hiked the name from Hold to Buy, noting that sales could stabilize as carryout numbers begin to heal over the next year. I think Stifel is right on the money. Domino’s stock is fresh off a 52-week low with a forward price-to-earnings (P/E) multiple of just 24.5 times and a price-to-sales (P/S) of 2.4 times, both of which are well below the restaurant industry average of 28.4 times and 6.5 times, respectively.

What is the Price Target for DPZ Stock?

Domino’s Pizza has a Moderate Buy rating, with 12 Buys, eight Holds, and two Sells. At the time of writing, the average DPZ stock price target of $347.05 implies a 4.7% gain for the year ahead.

2. Yum! Brands (NYSE:YUM)

Yum! Brands is the firm behind such names as KFC, Taco Bell, and Pizza Hut. The trio of reliable restaurant brands alone is worth a premium price of admission. However, when you also consider management’s willingness to experiment with new products, I do think Yum! stock makes for a terrific defensive growth play to ride out a rocky economic environment.

Cowen went as far as to call Taco Bell a “crown jewel” in the Yum! portfolio. I couldn’t agree more. Though Yum! isn’t exactly a steal at these levels, I’m staying bullish as many investors may be underestimating recession risk amid the market’s latest run.

It’s not so easy for a mature fast-food firm to give growth a jolt in such a competitive environment. Still, as more budget-constrained folks head to value-rich fast-food restaurants to save money, Yum! may have a chance to lure hungry consumers with intriguing menu items such as Taco Bell’s new vegan Crunchwrap. New offerings don’t always hit the spot, but they’re at least enough to get people in the doors.

At 26.2 times forward P/E and 5.6 times P/S, YUM stock is a quality name at a somewhat reasonable price.

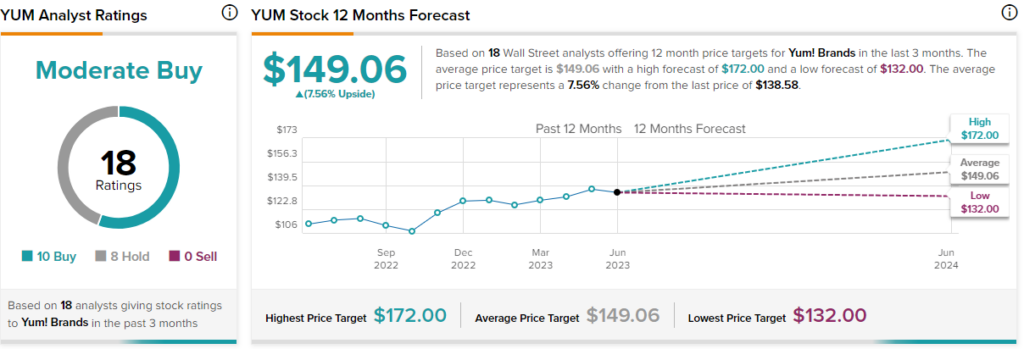

What is the Price Target for YUM Stock?

Yum! Brands is a Moderate Buy, with 10 Buys and eight Holds assigned in the past three months. The average YUM stock price target of $149.06 entails a 7.6% gain from here.

Conclusion

Restaurant stocks are terrific additions to batten down the hatches ahead of a turbulent economic contraction. Cava is the hottest new player on the scene, but after doubling in a day, I’d much prefer one of its more affordable restaurant peers.