Finding the right stocks is always a challenge – the retail investor can never expect to have the detailed knowledge needed to make the best decisions. That’s where the Street’s pros come in, the stock experts who do have that knowledge. They’ll sift and sort the stock markets, publishing their comments, and generally providing the raw information that investors need.

But there is still one missing datum – and that’s a knowledge of which stock analysts to trust. There are nearly 8,000 pros out there watching the markets, but some stand taller than others. We can follow these champs, and use their picks to make our own strong choices.

The Top Analysts tool at TipRanks make it easy to sort through the Wall Street stock experts. Every analyst gets a rating based on his or her success rate and the average return their recommendations would have brought in for the past year, and the tool lets investors sort through the analysts before choosing one or more to follow. The data can be parsed many ways, including by stock sector, and those results can sometimes change the rankings.

A good example is analyst John Freeman, from Raymond James, who is rated #4 overall.

Freeman, who focuses on energy firms, has recently been picking out companies in the North American hydrocarbon sector. With his expertise, he’s piled up a record that includes a solid 33% average return over the past year, making him worth listening to. Running the tickers through the TipRanks database, it’s clear Freeman is not alone in thinking these stocks have plenty to offer investors; all 3 are also rated as Strong Buys by the analyst consensus.

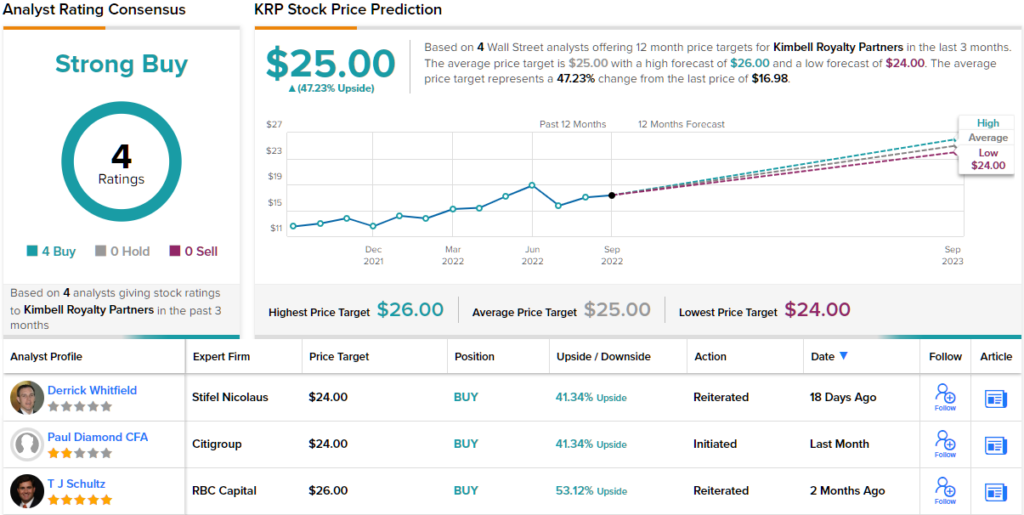

Kimbell Royalty Partners (KRP)

We’ll start in Texas, where Kimbell Royalty Partners is a land and mineral rights company operating in the Permian Basin. Kimbell also has extensive holdings out-of-state, particularly in the Bakken Shale of Montana/North Dakota and in the gas fields of Appalachia; overall, Kimbell has over 16 million acres of land holdings with mineral rights. The company’s holdings are based over some of North America’s richest energy basins, and play host to more than 122,000 gross wells, of which 74 currently have active rigs.

For investors, the best part of Kimbell’s ops may be its status as a royalty company. Kimbell owns the lands on which the wells operate, and it collects payments – royalties – from the operators – but it does not have to bear the cost of actually producing oil and gas from its holdings in order to make a profit. The result is high revenues and earnings relative to the effort invested, and those revenues and earnings have been growing over the past couple of years.

In the recent 2Q22, the company’s top and bottom lines hit record levels. Revenue came in at $72.7 million, and generated a net income of $43.3 million. Cash for distribution also hit a record level, at 74 cents per common share; this metric should interest investors, as it funds the dividend, which was set at a company-high of 55 cents per common share, up 17% from Q1 and representing an impressive 74% of the cash available for distribution.

John Freeman, turning his eye to Kimbell, says there are ‘too many records to count’ in the Q2 results, and describes the quarter as ‘one for the books.’ He goes on to write, “The best part? All quarter/quarter production growth (~4%) came organically, without the need for acquisitions. Given the production bump, along with a higher pricing environment Q/Q, KRP distributed a whopping $0.55/unit, surpassing RJ/Street by roughly 15%! Annualized, this equates to a ~13% distribution yield.”

This earns Kimbell a Strong Buy from the 5-star analyst, who sets his price target at $26, implying a one-year gain of 53% for the stock. (To watch Freeman’s track record, click here.)

While this mineral royalty company has shown it can generate the returns, it has still only picked up 4 recent analyst reviews. They all agree that it’s a Buy, however, making for a unanimous Strong Buy consensus rating. The shares are trading for $16.98 and their average target of $25 suggests a potential upside of ~47% for the year ahead. (See KRP stock forecast on TipRanks)

Viper Energy (VNOM)

Next up is another mineral rights company from Texas, Viper Energy. Viper’s collection of assets includes over 26,000 net royalty acres, with approximately 275 wells paying royalties. Those wells are generating strong production of 19,758 barrels of oil per day, up 20% since the second quarter of last year. Almost all of Viper’s assets are in Texas’ famous Permian Basin.

In 2Q22, Viper’s assets generated a net income for the company of $34 million. This came to 44 cents per common share, the highest in the past two years. Cash for distribution was higher, at $1.16 per common share. Viper has benefited from the relatively high oil prices this year; even the fall in crude prices hasn’t prevented the company from posting these solid results.

And the solid results have allowed Viper to boost its distribution to stockholders. The company increased its common share dividend to 81 cents, a jump of 21% quarter-over-quarter. The dividend has been increased 8 quarters in a row, and the current payment, which annualizes to $3.24 and gives a yield of 11.4%.

The dividend, and the company’s ability to generate cash for higher and higher capital returns, have caught the interest of Raymond James’ Freeman. The analyst says of Viper, “The strong production figures flowed through to their quarterly distribution, with VNOM announcing a distribution of $0.81/share. VNOM bumped their cash payout to 75% from 70% previously. The structure of VNOM’s dividend also changed, with the company choosing to implement a base+variable/buyback strategy. We anticipate VNOM leaning into the buyback for Q3 and Q4. The base has been introduced at $1/share annualized. We currently estimate a 2023 total shareholder yield of ~11.5% (dividends+buyback). VNOM has a competitive advantage with their FANG relationship, this combined with top tier assets in the Permian provide investors with a compelling yield vehicle.”

Following from this bullish outlook, Freeman puts an Outperform (i.e. Buy) rating on the shares, and a $41 price target that indicates potential for 43% appreciation in the coming year.

Overall, Viper gets a Strong Buy consensus rating, based on 10 positive reviews set over the past 3 months. The stock’s $28.66 trading price and $39.30 average price target give VNOM a 37% upside potential. (See VNOM stock forecast on TipRanks)

Hess Corporation (HES)

We’ll wrap up with Hess, and with this one we’ll be leaving both Texas and the mineral rights niche. Hess is still a hydrocarbon player – but the NYC-based firm is an exploration and extraction company with a global reach. Hess’s ops are located in the Bakken Shale, in the waters of the Gulf of Mexico, and off the coast of Guyana and Surinam in South America. The company has additional offshore operations in Thailand and Malaysia, and in Africa, in the Libyan desert. All of these are strong production regions in the global petroleum network.

In the most recent quarter, for 2Q22, excluding Libya, Hess’s ops produced 303,000 barrels of oil equivalent; almost half of that total came from the Bakken, which saw 140,000 boepd. This production generated a net income of $667 million, or $2.15 per common share; y/y, this represented a hefty gain from a $73 million net loss in 2Q21. Hess’s windfalls allowed it to finish 2Q22 with $2.16 billion in cash and liquid assets.

Deep pockets prompted Hess to begin a common stock repurchase program in 2Q22, when the firm bought back 1.8 million shares for $190 million. Adding dividends to the mix, Hess returned some $306 million to shareholders.

The dividend is not new, but it is sound. At 37.5 cents per common share, the payment annualizes to $1.50 per common share. The yield is modest, at 1.37%, but Hess has a 14-year history of keeping up reliable payments.

Freeman, in his notes on Hess, is impressed by the company’s upcoming projects going forward.

“Hess posted solid beats on per-share metrics this quarter, beating CFPS by 12%/9% over RJ/Street estimates and EPS by 4%/1%. Capex too came in under expectations, at $694M, beating RJ/Street by 7% and 9% respectively,” the analyst wrote. “HES’s FCF outlook is improving rapidly with Guyana ramping, with a 9% FCF yield projected in 2023 and a massive 23% in 2024. Given their strong anticipated production (and cash flow) ramp and lowered operating costs (thanks to Guyana), we reiterate our Outperform (Buy) rating.”

That rating is backed by a $140 price target, suggesting a 28% upside from current levels.

These shares have attracted notice from 9 of the Street’s analysts, whose reviews include 8 Buys and 1 Hold for a Strong Buy consensus. The stock is selling for $108.99 and its $143.88 average target implies a 32% gain in the next 12 months. (See HES stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.