Eastman Kodak (KODK) provides analog and digital innovations. It operates through the following segments: Print Systems; Enterprise Inkjet Systems; Flexographic Packaging; Software and Solutions; Consumer and Film; Advanced Materials and 3D Printing Technology; Eastman Business Park, and All Other.

We are neutral on the stock due to its terrible fundamentals.

Eastman Kodak Lacks a Competitive Advantage

There are a couple of ways to quantify a company’s competitive advantage using only its income statement. The first method involves calculating a company’s earnings power value (EPV).

Earnings power value is measured as adjusted EBIT after tax, divided by the weighted average cost of capital, and reproduction value (the cost to reproduce the business) can be measured using total asset value. If the earnings power value is higher than the reproduction value, then a company is considered to have a competitive advantage.

For KODK, the calculation is as follows:

EPV = EPV adjusted earnings / WACC

$480 million = $48 million / 0.1

Since Eastman Kodak has a total asset value of $2.19 billion, we can say that it does not have a competitive advantage. In other words, assuming no growth for Eastman Kodak, it would require $2.19 billion of assets to generate $480 million in value over time.

The second method to determine if a company has a competitive edge is by looking at its gross margin. This is because the gross margin represents the premium that consumers are willing to pay over the cost of a product or service. An expanding margin indicates that a sustainable competitive advantage is present.

If a company has no edge, then new entrants would gradually take away market share, leading to decreasing gross margins as pricing wars ensue to remain competitive.

In Eastman Kodak’s case, its gross margin contracted in the past decade. It peaked in Fiscal 2016 at 24.6%, dropping to 15.7% just a year later. Now, its gross margin sits at 13.4%. As a result, this trend indicates that a competitive advantage is not present in this regard either.

Risk Analysis

To measure risk, we will start off by analyzing the company’s earnings quality. We want to determine if the earnings figures are reliable or if they are being manipulated by the accountants. To do this, we will employ a method known as the Beneish M-Score, which can help us identify if a company is an earnings manipulator.

The interpretation is quite simple. If the M-Score is greater than -1.78, then the company is likely an earnings manipulator. In contrast, if the M-Score is less than -2, then the company is not likely an earnings manipulator. Lastly, a score that is between -1.78 and -2 is a possible manipulator.

Although the interpretation is simple, the calculation is not and requires many steps. The formula for this method is as follows:

M-Score =

-4.84

(+) 0.92 × DSRI

(+) 0.528 × GMI

(+) 0.404 × AQI

(+) 0.892 × SGI

(+) 0.115 × DEPI

(+) -0.172 × SGAI

(+) 4.679 × TATA

(+) -0.327 × LVGI

Where:

DSRI = Days Sales in Receivables Index

DSRI = (Net Receivablest / Salest) / (Net Receivables t-1 / Sales t-1)

GMI = Gross Margin Index

GMI = [(Sales t-1 – COGS t-1) / Sales t-1] / [(Sales t – COGS t) / Sales t]

AQI = Asset Quality Index

AQI = [(Total Assets – Current Assets t – PP&E t) / Total Assets t] / [(Total Assets – Current Assets t-1 – PP&E t-1) / Total Assets t-1]

SGI = Sales Growth Index

SGI = Sales t / Sales t-1

DEPI = Depreciation Index

DEPI = (Depreciation t-1/ (PP&E t-1 + Depreciation t-1)) / (Depreciation t / (PP&E t + Depreciation t))

SGAI = Sales General and Administrative Expenses Index

SGAI = (SG&A Expense t / Sales t) / (SG&A Expense t-1 / Sales t-1)

LVGI = Leverage Index

LVGI = [(Current Liabilities t + Total Long Term Debt t) / Total Assets t] / [(Current Liabilities t-1 + Total Long Term Debt t-1) / Total Assets t-1]

TATA = Total Accruals to Total Assets

TATA = (Income from Continuing Operations t – Cash Flows from Operations t) / Total Assets t

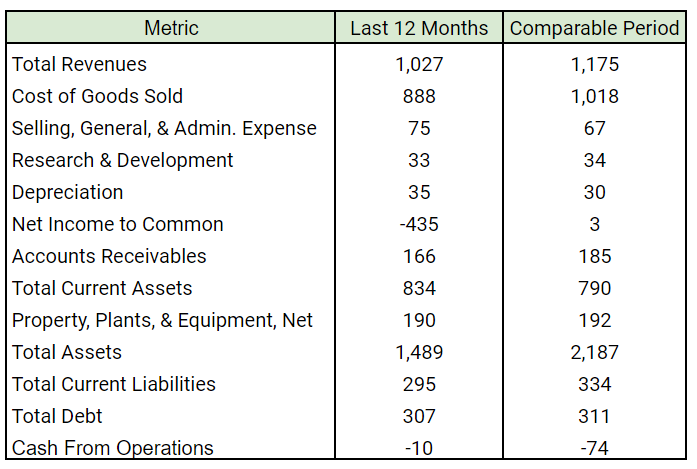

Now that we have defined the formula, we need to gather the data to input into the equations, which you will find in the image below:

Using the above data, we can carry out the calculations, which we have summarized in the image below:

Therefore, Eastman Kodak is likely to be an earnings manipulator because it has an M-Score of -1.76.

A quick comparison between the company’s EBITDA and free cash flow metrics adds further evidence to the company’s sketchy accounting. Since 2013, KODK has delivered positive EBITDA numbers each year. However, free cash flow has been very negative.

The differences between these two metrics tend to range in the hundreds of millions of dollars. A similar discrepancy can be found when looking at EBIT and net profit in some years.

Although its net profit is volatile, with some positive and negative years, the positive years are simply paper profits that don’t generate any actual cash. As a result, the company’s cash pile has dwindled steadily in the past 10 years, falling from $1.1 billion in 2012 to $300 million in the past 12 months.

Furthermore, there are other risks associated with the company. According to Tipranks’ Risk Analysis, Eastman Kodak has disclosed 41 risks in its most recent earnings report. The highest amount of risk came from the Finance & Corporate category.

The total number of risks has remained relatively flat over time, as shown in the picture below.

Smart Score Rating

Currently, no analysts are following Eastman Kodak. Therefore, we will take a look at TipRanks’ Smart Score Rating, which scores the company as 1 out of 10. This is consistent with its poor fundamentals and shrinking cash pile due to the lack of cash profits.

Based on its Smart Score, KODK will likely underperform, going forward.

Final Thoughts

Eastman Kodak has terrible fundamentals and a shrinking cash pile. It is likely an earnings manipulator, meaning that the EPV figure that we used earlier is probably inflated if existent at all.

As a result, we are neutral on the stock because its volatile price action makes shorting the company very risky. Thus, it’s probably best for investors to simply avoid it completely.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure