Video game stocks have been in a vicious bear market alongside nearly everything else these days. Therefore, in this piece, we used TipRanks’ Comparison Tool to look at two video-gaming juggernauts — EA and TTWO — that seem to have too much recession risk factored into their share prices. With all the industry consolidation we’ve witnessed in recent years, I’d also be unsurprised if either of the two stocks is gobbled up by a firm looking to make a gaming splash. Of the two stocks, analysts are most bullish on TTWO, but let’s dig deeper.

Though video games tend to be viewed as “nice-to-haves” in times of economic turbulence, I view them as some of the most affordable forms of entertainment on a per-hour basis. In simple terms, games are a great value proposition for consumers looking to be cautious with their spending.

Gaming consoles may be a hefty expenditure, but gamers who’ve finally gotten their hands on the latest Xbox Series X or PlayStation 5 are eagerly awaiting the latest slate of next-generation titles.

Indeed, the video-gaming market is growing quite fast. The looming recession has taken a stride out of the step of video game stocks. However, it seems like there’s too much pessimism baked in, given a recession-driven rise in unemployment could pave the way for consumers to substitute “going out” for staying in and playing a game. Without further ado, let’s take a look at EA and TTWO.

Electronic Arts (NASDAQ: EA)

Electronic Arts is one of the oldest gaming juggernauts out there. The firm, well-known for its slate of annual sports titles, has seen its shares hit a brick wall in recent years. The stock has been stuck in a $120-140 consolidation channel since mid-2020.

It’s not easy to thrive in gaming. Like big-budget films, there’s a lot of risk in spending great sums for a title that’s not even guaranteed to draw a crowd. With disappointing titles like Battlefield 2042, firms like EA are bound to think twice before committing to new projects.

Indeed, risk-taking on big-budget titles can come with huge rewards (think hit game Apex Legends), but it’s proven tough to stay on the content-spending wheel these days, especially with growing competition from the likes of gaming behemoth Microsoft (NASDAQ: MSFT).

Given the hit-or-miss nature of gaming, the market seems to favor firms with the deepest pockets and the least to lose. Now, EA is no slouch, with its $34.1 billion market cap. However, it may ultimately be in better hands under the umbrella of a tech or media behemoth.

Even without a suitor, EA is pushing into the higher-growth mobile gaming market with its hit title, Apex Legends. Further, EA has been participating in industry-wide consolidation itself – with Codemasters and Glu Mobile.

The future is quite hazy, especially if Microsoft continues wheeling and dealing in the gaming space. Regardless, EA stock is priced with not much in mind.

The stock trades at 39.1x trailing earnings and 4.8x sales. The multiple seems rich relative to its growth, likely due to its scarcity premium (the number of publicly-traded gaming stocks has been falling) and the market growth potential in gaming.

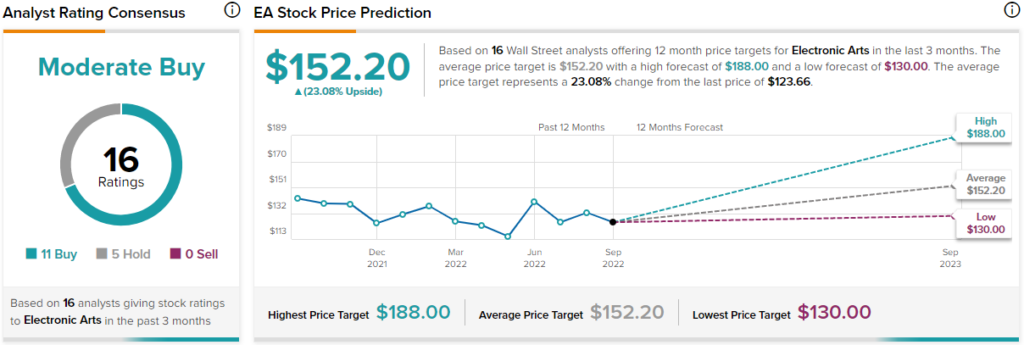

What is the Price Target for EA Stock?

Wall Street remains upbeat on EA shares with a “Moderate Buy” rating. The average EA stock price target of $152.20. That implies 23.1% upside from current levels. An impressive gain for a firm that would be a very attractive takeover target for any entertainment heavyweight.

Take-Two Interactive (NASDAQ: TTWO)

Take-Two Interactive stock has been decimated in recent years, now off more than 43% from its all-time highs just shy of $215 per share. While there have been a handful of intriguing titles like Tiny Tina’s Wonderland to keep gamers entertained before the much-anticipated Grand Theft Auto (GTA) VI, it’s clear that investors simply cannot wait any longer.

With a reported $2 billion budget for GTA VI, it certainly seems like Take-Two is putting most of its eggs in one basket. For an investor, that’s not a good thing. Regardless, I do view TTWO stock as a cheap high-upside play for those willing to be patient.

As I noted in a prior piece, GTA VI cannot afford to rush production and risk a rocky launch day. Budget overruns and delays wouldn’t surprise me. Though such setbacks could add further downside pressure on the stock. In any case, GTA seems like one of the few franchises that are nearly guaranteed to be a smash hit once ready.

Like EA, Take-Two is eager to diversify itself into mobile. The Zynga deal gives Take-Two a nice foundation in the mobile-gaming scene. Though Zynga and other titles can help power a rebound in TTWO stock, GTA VI still seems to be a “make or break” for the firm.

Industry insiders pin a GTA VI launch in the 2024-25 range. That’s a long time to wait in a stock that can’t seem to catch a break. At just 5.3x sales, though, I think the stock is depressed enough that it can rally under its own feet well before GTA lands.

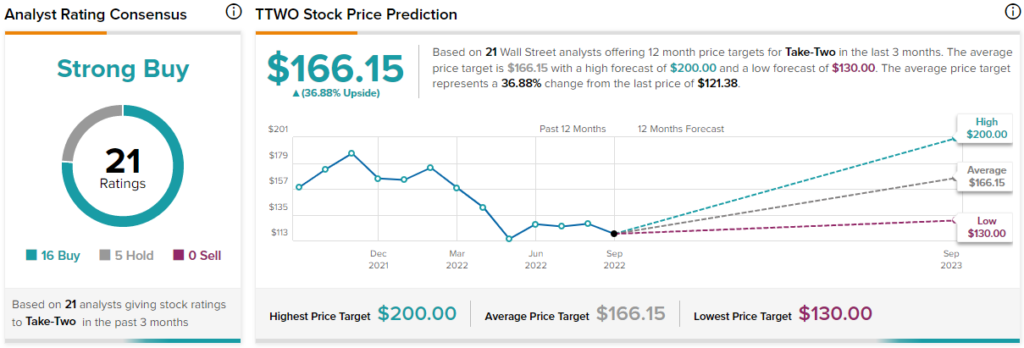

What is the Price Target for TTWO Stock?

Wall Street is staying patient with TTWO shares, with a “Strong Buy” rating. The average TTWO stock price target of $166.15 implies 36.9% upside over the year ahead. That’s a solid gain for a firm likely to be much higher in three years’ time.

Conclusion: Wall Street Expects Higher Upside from TTWO Stock

EA and Take-Two are under pressure, but their long-term outlooks seem solid. Both firms have full pipelines and robust mobile businesses. Between the two names, Wall Street prefers Take-Two stock.