Whether markets move up or down, every investor loves a bargain. There’s a thrill in finding a valuable stock at a low, low price – and then watching it appreciate in the mid- to long-term. Portfolio growth of that sort is one of the reasons investors are in the investing game to begin with.

So, how are investors supposed to distinguish between the names poised to get back on their feet and those set to remain down in the dumps? That’s what the pros on Wall Street are here for.

Using TipRanks’ platform, we pinpointed three beaten-down stocks the analysts believe are gearing up for a rebound. Despite the hefty losses incurred in 2022, the two tickers have scored enough praise from the Street to earn a “Strong Buy” consensus rating.

Magnite (MGNI)

The first stock we’ll look at is Magnite, a billion-dollar, independent, sell-side ad-tech platform. The company formed through a merger of equals between Rubicon and Telaria in April of 2020, and quickly registered both impressive revenues and impressive revenue growth. In the company’s first year as its own entity, 2020, Magnite saw $221.7 million at the top line; that number grew by 111% to reach $468.4 million in 2021. The company offers customers ad publishing across a wide range of available formats, from CTV to desktop and mobile computing devices to audio channels.

Magnite has continued that growth in 2022. The company’s revenues typically slide from Q4 to Q1, and the recent 1Q22 was no exception – but the top line total of $118.1 million was up 94% year-over-year. EPS was reported at 8 cents. Like the revenue total, this was down sharply from 4Q21 but up sharply year-over-year, being more than double the 3 cents reported in 1Q21. Magnite will report 2Q22 numbers on August 8.

Despite these positive results, Magnite’s shares are down 57% so far this year. Several factors have been putting headwinds in front of MGNI, including global supply issues as advertisers pulled ads when they were unable to bring products to market; travel-related ad spends that have yet to return to pre-pandemic levels; and the combination of high inflation and rising interest rates, which are eating into thin profit margins.

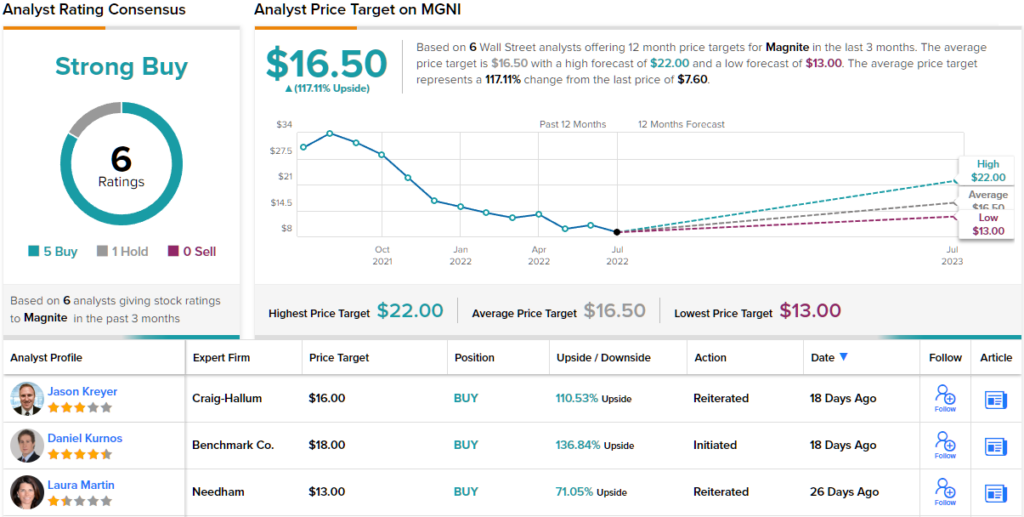

Even though it’s facing hard times, Benchmark analyst Daniel Kurnos keeps a Buy rating on Magnite shares, along with an $18 price target. If correct, the analyst’s objective could deliver one-year returns of ~141%. (To watch Kurnos’ track record, click here)

Backing his bullish stance, Kurnos writes: “We expect Magnite will continue to be a winner in what is likely to be a consolidating ecosystem… We continue to believe that being closest to the ad exchange has material advantages, which may become more emphasized with the move towards server-side bidding. And while CTV is expected to be the growth engine with most of the catalysts, mid-teens revenue ex traffic acquisition cost (TAC) growth rate for non-CTV operations appears sustainable, in our view.”

The Benchmark view is clearly bullish, but it’s also far from an outlier. Of the 6 recent analyst reviews on record for MGNI, 5 are to Buy against just 1 to Hold, for a Strong Buy consensus rating. The shares are trading for $7.60 and their $16.50 average price target indicates room for share growth of 117% in the next 12 months. (See MGNI stock forecast on TipRanks)

Ranpak Holdings (PACK)

Next up is Ranpak, an industrial stock that lives in the packaging field. We may not think about packaging much, but most of the products we use in our daily life come to us wrapped up in one way or another, and Ranpak operates in that niche. The company develops and produces a full range of packaging solutions using environmentally sound manufacturing processes to generate products that are biodegradable, recyclable, and renewable, with the long-term goal of ameliorating the very real problem of plastic-based debris and litter in our landfills and landscapes.

To meet these goals, Ranpak has over 40 years of practical experience in the field, more than 250 global distribution partners, and over 400 relevant patents to protect its intellectual property.

While this is a viable niche to work in, Ranpak’s results in 2022 have disappointed the market. In the most recent quarterly results, 2Q22, the company showed a year-over-year drop in revenue of 3.6%, from $90 million in the year-ago quarter to $86.8 million in the current report. Earnings, which have been running at a net loss since 2Q21, came in at minus 14 cents per diluted share. This was double the loss seen in the year-ago quarter.

What really impacted the stock, however, was the forecast miss. Ranpak’s EPS loss came in 4 cents worse than the 10-cent forecast. The company attributes the whiff to a deteriorating economic environment, especially in Europe, where energy shortages are starting to impact economic activity. With that in mind, we can see why the stock peaked in November of last year, and has been sliding ever since. Year-to-date, the loss comes in at 86%.

At the same time, Ranpak can boast a solid foundation on which to find its footing for future operations. The company has no net debt drawn from its revolving credit facility, which is worth $45 million, and better, it has a cash balance on hand of $59.2 million.

The combination of available cash and a leading position in its niche have 5-star analyst Ghansham Panjabi, of Baird, sanguine on this stock’s future.

“While 2022 is shaping up to an extreme transition year for the company, we revert back to our previously published view that the shares have already deeply discounted the latter—with the stock at/below March 2020 lows even with a higher machine installed base (indicative of franchise value) and a stronger liquidity profile,” Panjabi noted.

“We believe that the stresses of the current operating environment will ease over the next few quarters, noting that PACK has considerable franchise value based purely on its installed machine base—with the company an attractive asset in a consolidating industry,” the analyst added.

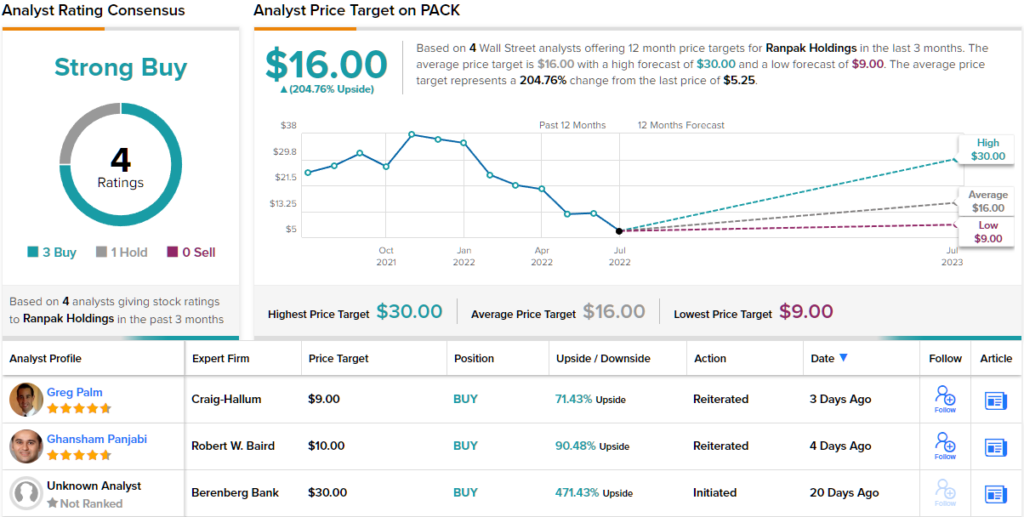

Following this line of thought, Panjabi gives PACK shares an Outperform (i.e. Buy) rating, and sets a price target of $10 to imply an upside potential of ~90% on the one-year time frame. (To watch Panjabi’s track record, click here.)

Overall, the Street agrees with the bullish take on this stock’s potential. The 4 recent analyst reviews break down 3 to 1 in favor of Buy over Hold, to support the Strong Buy consensus, and the average price target of $18 suggests a robust 205% upside from the current share price of $5.20. (See PACK stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.