Buy cheap? Even in the stock market, buyers like to find a bargain. Defining a bargain, however, can be tricky. There’s a stigma that gets attached to low stock prices, based on the reality that most stocks don’t fall without a reason. And those reasons are usually rooted in some facet of poor company performance.

That said, you can still find stocks trading at deep discounts, stocks whose share price has been pushed down – perhaps by fundamentals, perhaps by market conditions, perhaps by plain bad luck – and those discount prices are linked to some of the best upside potentials in the market.

Using TipRanks’ database, we identified two stocks that feature both low prices now – and powerful upside potential for the coming year. Not to mention each one gets a “Strong Buy” consensus rating from the analyst community. Let’s dive in and find out what’s driving that prospect.

Luminar Technologies (LAZR)

The first stock we’ll look at is Luminar Technologies, a Palo Alto-based Silicon Valley high-tech firm working in the autonomous vehicle segment. Luminar is a designer and manufacturer of Lidar systems, the cutting-edge sensor tech that acts as the ‘eyes’ for self-driving cars. Luminar is involved in all levels of Lidar tech, from the semiconductor chips in the guts of the hardware to the sensors, transceivers, receivers, and electronics that make it all work.

Luminar went public via a SPAC merger in December 2020, and in that time the company’s shares peaked above $40. Since then, however, the shares have dropped by 77%. During that time, the company’s net loss has also deepened in five consecutive quarters. Revenues have remained low, reflecting the company’s low-level sales as it positions itself to supply an industry that is not yet ready for mass production.

Not everything is doom and gloom however. Luminar does offer some high potential for investors. For starters, Lidar is essential in autonomous vehicle tech – and Luminar’s systems are well-regarded. Furthermore, the company’s revenues, while modest, are moving in the right direction; the 2Q22 top line, at $9.9 million, was up 45% quarter-over-quarter and 57% year-over-year – and beat the forecasts by 12%. EPS was reported at a negative 18 cents, on a non-GAAP net loss of $65 million. Luminar was able to finish the quarter with plenty of cash in the bank, $605.3 million as of June 30.

On another positive note for investors, Luminar raised its forward revenue guidance for the full-year 2022, from $40 million to the range of $40 million to $45 million.

Overall, Luminar shares are down 49% year-to-date. The drop, however, has not discouraged Austin Russell, the president and CEO of Luminar, from increasing his holding. Russell has made a series of buys in the last two weeks, each one for a six-figure sum. Taken together, Russell has spent over $1.6 million on several blocs of LAZR, totaling 175,000 shares.

Deutsche Bank analyst Emmanuel Rosner is also bullish on Luminar and its prospects, writing: “We are impressed with LAZR’s ongoing success in winning new business and growing order book by the magnitude of +60% this year. The company also continues to form partnerships with leading OEMs and mobility providers, which should give it a clear path to scale toward profitability and market expansion. We forecast revenue to be $44m/$133m in 2022-23E and then rising to >$385m by 2024E… We continue to believe LAZR is one of the best positioned LiDAR suppliers to capture large business wins for L3+ autonomy in the near-term.”

All of this prompted Rosner to rate LAZR shares a Buy along with a $15 price target. This target conveys his confidence in LAZR’s ability to climb ~74% higher in the next year. (To watch Rosner’s track record, click here)

The Strong Buy analyst consensus rating on LAZR shows that the Street is in general agreement on that bullish view. The 8 recent analyst reviews break down 6 to 2 in favor of Buys over Holds, and the stock’s $15 average price is practically the same as Rosner’s. (See LAZR stock forecast on TipRanks)

AppLovin (APP)

Next up, AppLovin, is a software platform providing optimization tools for mobile app developers. The proliferation of mobile smart devices, and their attendant apps, has opened up a huge opportunity for app creators – and these, in turn, form AppLovin’s customer base. In addition to app creation tools, AppLovin offers advertising, analytic, and publishing services.

Some numbers will tell the story. AppLovin has seen more than 4 billion downloads over the past 12 months, and brought in $776 million in top line revenue for the recent 2Q22. That top line value was up 16% year-over-year, and included a massive 118% y/y increase in Software Platform revenue, which made up $318 million of the total.

On earnings, the story was different. AppLovin reported a net loss of $22 million, compared to a year-ago gain of $14 million. The company faced serious headwinds in the mobile app industry, including reduced consumer spending, and changes to overall privacy policies that have impacted app discovery rates.

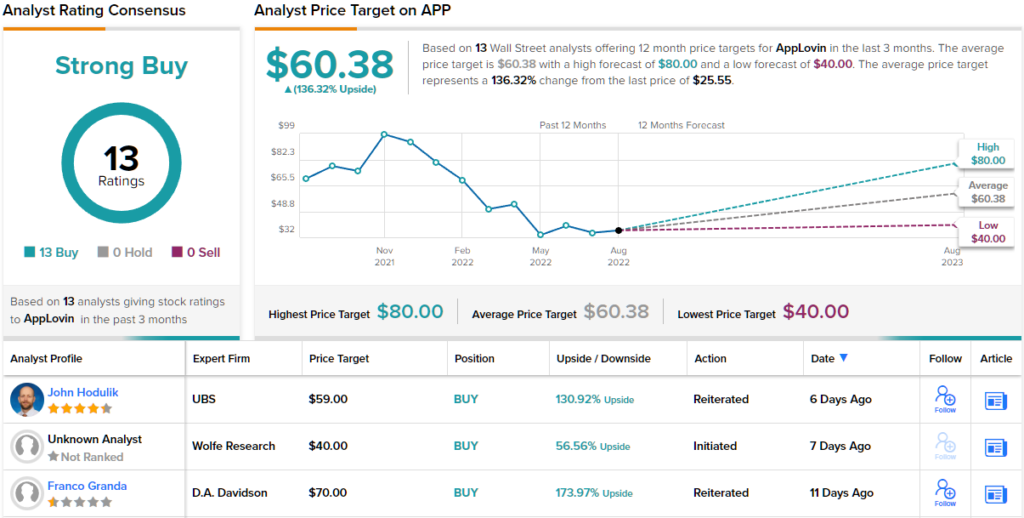

Overall, investors are wary, and the stock is down 73% this year. However, AppLovin has been attracting positive attention from Wall Street analysts, who see the low price as an attractive entry point.

Among the bulls is 5-star analyst Youssef Squali, of Truist, who writes: “The Software segment was again the bright spot in 2Q22 as APP’s ML engine AXON continues to fuel its growth. This was offset by weakness in Apps revs, impacted by softer consumer demand/optimization of mktg spend to drive up margins while this segment remains under strategic review. This mix shift should lead to higher quality revenue/margins, which over time should help re-rate the stock and drive shareholder value, in our view.”

To this end, Squali puts a Buy rating on APP, and adds to it a $65 price target that indicates room for a 12-month upside of 154%. (To watch Squali’s track record, click here)

The mood on the Street is just as bullish as the Truist view, with 13 positive analyst reviews giving a unanimous Strong Buy consensus rating. The current trading price is $25.55 and the average price target of $60.38 implies gains approaching 136% on the one-year horizon. (See AppLovin stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.