While the banking industry could face headwinds in the coming quarters, high-quality companies trading at inexpensive multiples could present fruitful buying opportunities. Two such high-quality picks, in my view, are JPMorgan (NYSE: JPM) and Citigroup (NYSE: C). Nonetheless, amid a highly speculative medium-term capital markets setup moving forward, however, I am neutral on both names.

The banking industry is currently being pulled by two opposing forces. On the one hand, while rising interest rates hurt most businesses, banks are likely to generate higher net investment spreads.

On the other hand, with the economy projected to slow down in the coming quarters and inflation raging, banks will have a much harder time growing. Their valuation multiples are also being compressed. These are things to consider before purchasing bank stocks.

Putting JPMorgan’s Latest Results in Context

The ongoing brutal macroeconomic and overall market landscape has already started impacting the banking industry’s performance. This has been the case with JPMorgan’s recent performance.

In its Q2-2022 results, JPMorgan reported revenues of $30.7 billion, largely unchanged compared to last year. However, net income plummeted by a substantial 28% to $8.6 billion during this period. While such a steep decline rightfully rattled investors, some context is needed to understand why it’s not as dire as it seems at first glance.

Basically, last year’s profits of all banks were uplifted significantly by reserve releases, leading to net income levels nearly doubling compared to Fiscal 2020 at the time. This was because the majority of bank balance sheets were bolstered last year amid the release of COVID-era credit loss allowances.

These credit loss allowances contain the reserves financial institutions piled up since the pandemic began in order to absorb the possible scenario of some borrowers being incompetent in fulfilling their debt commitments. Thus, it makes sense that the year-over-year decline this year is only to be expected.

In Q2, JPMorgan reported a net credit reserve build of $428 million against a net credit reserve release of $3.0 billion in the comparable period last year. Therefore, the massive net income decline is only synthetic and should not spur unnecessary worries.

Overall, Q2 results were somewhat mixed, nonetheless. In Consumer & Community Banking, deposits expanded 13% while client investment assets fell 7%, primarily due to negative net flows. Then, you have combined debit and credit card spending growing 15% as JPMorgan continues to see robust spending in traveling and dining. It’s truly a very mixed picture.

For this very reason, investors face uncertainty on multiple fronts. That said, investors ought to realize that Fiscal 2022 should still be a significantly profitable year for JPMorgan when taking into account the all-around circumstances.

Wall Street analysts anticipate the company to deliver EPS of $11.14 for the year, indicating a fall of around 27.2% compared to Fiscal 2021 due to the reasons mentioned above. Nevertheless, this indicates a robust 25.3% increase compared to Fiscal 2020, which embodies the upbeat earnings growth trajectory when last year’s reserve release is put into context.

Citigroup’s Results Also Were Better Than Most Investors Think

Citigroup shares have also declined notably since the company’s latest results release, as net income came in at $4.5 billion, a decline of 27% compared to Q2 2021. Again, however, putting results into context paints a different picture.

Essentially, the bank recorded a net credit reserve build of $400 million against a net credit reserve release of $2.4 billion in the comparable period last year. Excluding this, the company’s net income would have actually grown, as revenues advanced by 11% to $19.6 billion.

I am particularly impressed by this revenue increase, considering that it was driven solely by higher interest rates, as investment banking activities slowed down amid a shaky equities market environment. Thus, with rates still on the rise, a recovery in investment banking is likely to accelerate Citigroup’s overall revenues quite substantially.

Which Stock is More Reasonably Valued?

Based on analysts’ estimates for Fiscal 2022, JPMorgan and Citigroup trade at P/Es of about 10.5x and 6.7x, respectively. From another point of view, Citigroup reported a tangible book value per share of $80.25 in its latest results, implying that shares are currently trading at a tangible P/B of around 0.6x – that’s close to half their book value! JPMorgan reported a tangible BVPS of $69.53, implying a tangible P/B ratio of 1.67x.

Citigroup is clearly cheaper on both metrics. In my view, this is due to JPMorgan’s more diverse and larger operation and excellent management over the years. Still, Citigroup appears to offer investors a higher margin of safety and larger upside potential at its current stock price levels. This is also supported by the stock’s 4.0% yield against JPMorgan’s lesser 3.3%.

What are the Price Targets for JPM and Citigroup Shares?

Turning to Wall Street, JPMorgan has a Moderate Buy consensus rating based on ten Buys, seven Holds, and one Sell assigned in the past three months. At $138.33, the average JPMorgan price target implies 17.4% upside potential.

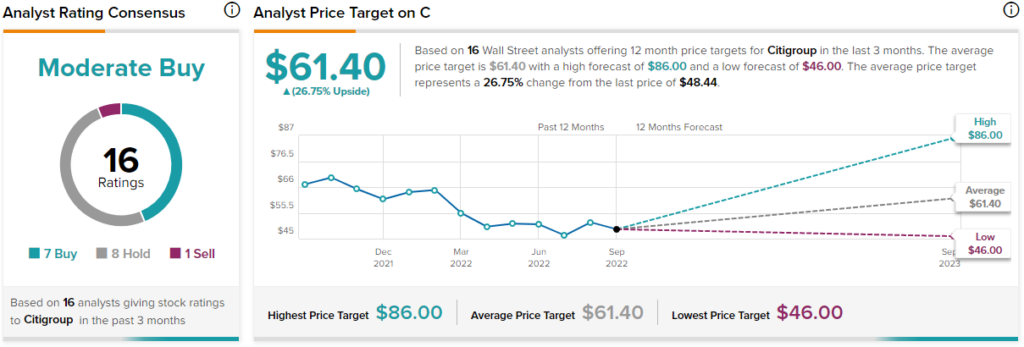

Despite Citigroup appearing considerably more undervalued on paper, as mentioned earlier, analysts’ expectations for Citigroup aren’t too different from JPM’s. Specifically, Citigroup also has a Moderate Buy consensus rating based on seven Buys, eight Holds, and one Sell rating assigned in the past three months. At $61.40, the average Citigroup price target implies a 26.75% upside potential.

Conclusion: Attractively Priced Banks, but Uncertainty Lies Ahead

In my view, both banks are relatively undervalued against their current and future net income generation potential – especially Citigroup, which trades at a discount to its book value. Both companies also feature great capital return track records, and while both have suspended buybacks, their dividend yields are quite attractive.

Still, with much uncertainty regarding the medium-term outlook of the economy, investors should expect the ongoing pressure imposed on the two stocks by the capital market to be sustained.