Delta Air Lines (NYSE:DAL) is scheduled to announce its third-quarter earnings on October 12, before the market opens. Strong demand for both leisure and corporate travel is expected to have positively impacted the U.S. airline’s quarterly performance. The demand was supported by robust employment levels, rising wages, and hybrid work facilities during the July-September period. It is worth mentioning that several analysts have reaffirmed their Buy ratings on the stock, remaining optimistic ahead of the Q3 earnings release.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Overall, the Street expects Delta to post Q3 earnings of $1.96 per share, showing a 29.8% jump over the prior-year quarter. Similarly, sales estimates are pegged at $14.53 billion, representing a smaller 4% increase over the same period last year.

However, last month, the company provided a rather disappointing update for its third-quarter expectations. Delta expects a negative impact on its bottom line due to rising fuel prices and increasing aircraft maintenance costs during the to-be-reported quarter.

As a result, Delta has adjusted its per-share earnings estimate to a range of $1.85 to $2.05, down from the previously guided range of $2.20 to $2.50. In addition to this, the company anticipates a decrease in its unit revenue of 2-3%.

Q3 Earnings: Here’s What Analysts Are Saying

Among the bullish analysts, Duane Pfennigwerth of Evercore ISI believes the industry’s load factors have strengthened during the past two weeks, suggesting a potential uptick in demand. Furthermore, the analyst anticipates that Delta’s Trainer refinery, which has been offline for much of the fourth quarter of 2023 for maintenance, will resume its contributions beginning in 2024.

Next, in a research note to investors last week, Barclays analyst Brandon Oglenski noted that higher fuel prices and capacity growth-related costs have weighed on the airline sector. Looking ahead, he anticipates that 2024 will bring its own set of challenges and foresees slower growth in domestic capacity compared to 2023.

Is DAL a Good Stock to Buy Now?

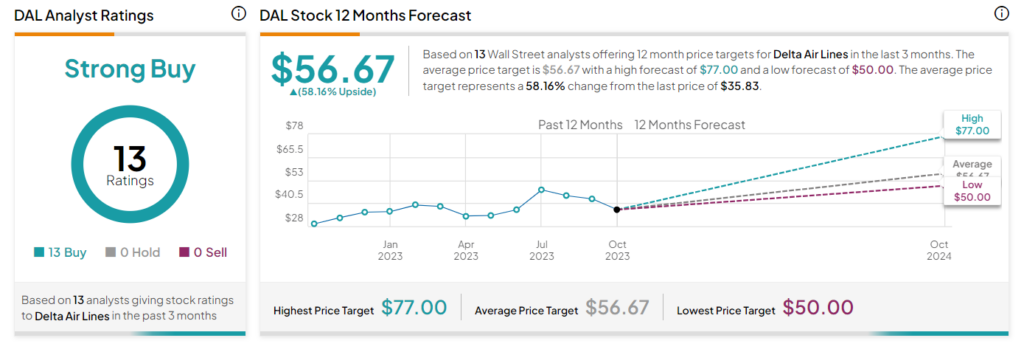

Overall, Delta has a Strong Buy consensus rating based on 13 unanimous Buys. The average DAL stock price target of $56.67 implies 58.2% upside potential. The stock has gained nearly 10% so far in 2023.

Insights from Options Trading Activity

TipRanks now presents options activity to help investors plan their trades ahead of earnings releases. Options traders are expecting that DAL stock will move by +/-4.58% after reporting earnings. The anticipated earnings move is determined by computing the at-the-money straddle of the options closest to the expiration after the earnings announcement.

Ending Thoughts

Delta has been expanding its portfolio by partnering with Certares and Knighthead, tourism-focused investors, as well as with Wheels Up Experience (UP), an on-demand private aviation provider. Furthermore, the airline’s efforts to fortify its balance sheet, generate cash flow, and provide value to its shareholders through dividend payouts are encouraging.