The rollercoaster ride continues in the stock market, and equities have been falling across the board this week. The S&P 500 is down 3.5%, and the Dow has lost some 870 points. The market drop was fueled by uncertainty; recent economic data has been unexpectedly positive, and it’s clouded the forecast for the Fed’s interest rate decision next week.

The central bank’s twin mandates, to rein in inflation and to moderate unemployment, frequently run counter to each other, and with inflation running high and unemployment running low, it’s hard to know what to expect.

The logical move right now, for investors wanting to stay in stocks, is a move into defensive plays. That’s the thesis behind Jefferies equity strategist Steven DeSanctis’ recent note. He noted, “We were pleased to see a turn in sentiment towards High Yield… Defense is the name of the game these days.”

With this in mind, Jefferies analysts have picked out two stocks with high dividend yields, including one that pays as high as 13%, as the right moves going forward. These are the traditional defensive plays, as they ensure a steady return, and with reliable dividends yielding way above average, they can beat inflation, too.

Opening up the TipRanks database, we examine the details behind these tickers to find out what else makes them compelling buys.

Global Ship Lease (GSL)

The first dividend stock we’re looking at is Global Ship Lease, an independent owner-operator in the global shipping industry, with a fleet of 65 small- to mid-sized containerships, the workhorses of the world’s ocean trade routes. These ships types carry cargoes of virtually any type, and make up more than 70% of the global containerized trade volume. Global Ship generally charters its vessels out, and receives an income stream from daily lease rates over each vessel’s contract period. As of the end of Q3 this year, the company had charter contracts worth $2.2 billion, and an average of 2.9 years remaining on its contracts.

In early November, GSL released its 3Q22 financial results, and showed gains at both the top and bottom lines. Total revenues came to $172.5 million, up 11.6% from Q2 – and up 24.4% from the year-ago quarter. These top-line results are part of a strong trend in 2022 toward increased revenues; for the nine-months ending on September 30, the company saw a 63% year-over-year increase in revenues.

At the bottom line, the net income of $92 million represented a 41% y/y increase. The net income available to common shareholders was reported at $89.6 million, up 42% y/y. On a per-share basis, the EPS of $2.44 was up 41% from the $1.73 reported in 3Q21.

These solid gains supported the company’s dividend, which was declared at 37.5 cents per common share, and was paid out on December 2. At this rate, the dividend annualizes to $1.50 per share, and gives a yield of 9.2%. This yield is more than 4x higher than the average found among S&P-listed firms, and is a 1.5 points higher than the last reported rate of inflation.

Jefferies’ 5-star analyst Omar Nokta is impressed with GSL’s execution in recent months, writing, “The company sits in a very solid position with a sizable revenue backlog, boosted during the quarter with the fixing of 10 ships on term charters, and has plenty of flexibility going forward… With a conservative and disciplined approach, we see GSL as having ample flexibility to take advantage of opportunities that are likely to arise going forward…”

The yield is compelling in our view as the payout represents just one-fourth of the company’s ongoing free cash flow. Management also bought back $15.1 million of its outstanding shares during September and October,” the analyst added.

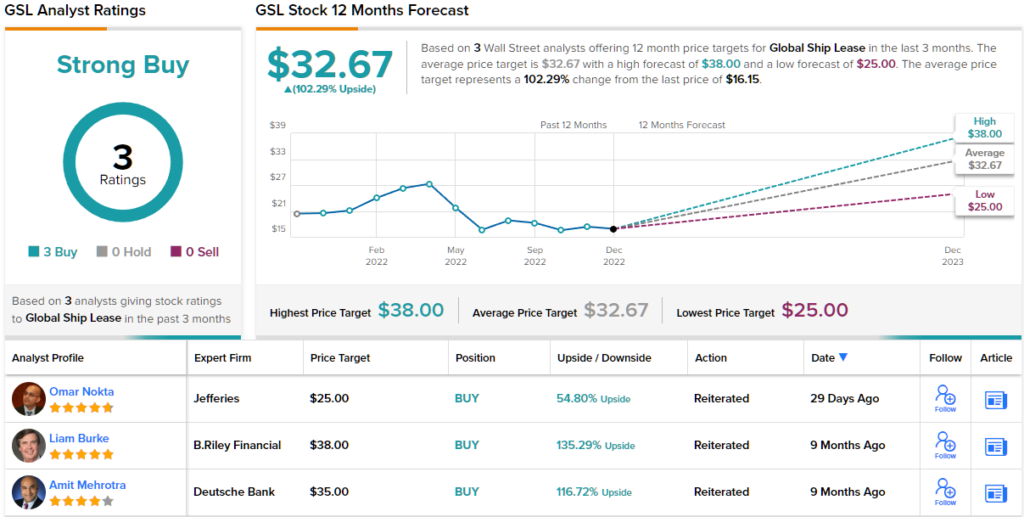

To this end, Nokta sets a Buy rating here, along with a $25 price target implying room for ~55% share appreciation on the one-year timeline. Based on the current dividend yield and the expected price appreciation, the stock has ~64% potential total return profile. (To watch Nokta’s track record, click here)

Turning now to the rest of the Street, other analysts are on the same page. With 3 Buys and no Holds or Sells, the word on the Street is that GSL is a Strong Buy. The stock has a $32.67 average price target and a share price of $16.15, for a one-year upside potential of ~102%. (See GSL stock forecast on TipRanks)

Chesapeake Energy (CHK)

Now we’ll turn to the energy industry, where Chesapeake is a large-cap player in the hydrocarbon exploration and development sector. The company operates across North America, and counts major assets in several of North America’s most productive natural gas regions, including the Texas Eagle Ford formation, the Marcellus shale of Pennsylvania, and especially the Haynesville formation of Louisiana. At the end of last year, Chesapeake’s confirmed reserves were mainly in natural gas, at 69%, but included substantial amounts of natural gas liquids (8%) and petroleum (23%).

Chesapeake’s strong foundation in real-life assets supports the company’s solid financial results. Revenues and earnings have both been on an upward trajectory since the second quarter of last year; in the 3Q22 report, the last one released, the company reported over $4.1 billion in total revenues. Cash from operations came in at more than $1.3 billion, and the net income of $883 million meant an earnings per share $6.12. On an adjusted basis, the income of $730 million led to an adjusted diluted EPS of $5.06, up 112% from 3Q21.

Of particular interest to investors, because it directly supports the company’s dividend policy, Chesapeake reported a quarterly record in free cash flow in Q3, of $773 million. Chesapeake managed this end result even as it returned $1.9 billion in shareholders during the quarter, through a combination of share repurchases and dividend payments.

The last declared dividend, counting both regular and supplemental payments, totaled $3.16 and was paid out this past December 1. At the current payment, the dividend annualizes to $12.64 per common share and yield is an impressive 13.4%. It’s a rare stock that pays out a total dividend more than 6x the average.

In his coverage of Chesapeake for Jefferies, Lloyd Byrne, another of Jefferies’ 5-star analysts, sees several reasons for continued optimism on the stock, stating: “We continue to like CHK on valuation, well-positioned assets, solid shareholder returns and continued progress on Haynesville strategy… CHK has a solid and balanced shareholder returns framework. For ’22, CHK will return ~$2.3bn, or ~17% of the current market cap.”

“We believe the company will continue to opportunistically add basis / hedges / physical contracts with set differentials to their profile for 2023, helping protect returns in a likely volatile gas market,” the analyst added.

Looking forward, Byrne gives CHK a Buy rating, with a price target of $150 pointing toward ~56% upside in the coming 12 months. (To watch Byrne’s track record, click here)

Overall, Chesapeake has picked up 6 recent reviews from the Street’s analysts, and their takes include 5 Buys against a single Hold – for a Strong Buy consensus rating on the shares. The stock has a current trading price of $146.33, suggesting a one-year upside potential of 53%. (See CHK stock forecast on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.