Investing in the volatile aviation industry takes guts. Airlines are highly sensitive to economic cycles and fuel prices, while intense competition constantly squeezes margins. However, two names stand out in this challenging landscape: Delta Air Lines (NYSE:DAL) and United Airlines (NASDAQ:UAL). Using TipRanks’ stock comparison tool below, these two companies are distinguished by their Strong Buy ratings on Wall Street and strong Smart Scores.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Considering their best-in-class margins per unit among U.S legacy airlines and trading at de-risked valuations, I believe both of these airlines deserve their Strong Buy ratings. Therefore, I am bullish on DAL and UAL.

Delta Airlines (NYSE:DAL)

Delta Airlines stands out in the industry mainly due to the high quality of its balance sheet, given the company’s relatively low debt levels. In addition to its competitive position in lucrative domestic and international markets, the Atlanta-based company had a debt-to-assets ratio of 97% in 2020 at the height of the pandemic, which it has managed to stabilize at around 80% in the last two years.

Delta’s high-quality margins also stand out. In 2023, Delta reported a passenger revenue per available seat mile (PRASM) of $17.98. After subtracting the cost per available seat mile, excluding fuel and one-time expenses (CASM-ex) of $13.17, the result was a per-unit margin of $4.81. In other words, for every available seat mile, the airline generated an operating profit of nearly $4.81 after covering its operating costs— tied with UAL for the highest among U.S. legacy airlines.

Moreover, Delta’s stock has appreciated strongly over the last six months due to a sharp turnaround in earnings despite costly fuel and labor, especially since October of last year. Over the past 12 months, DAL stock has risen by 44%.

More recently, in the quarter ending in March, Delta flew 54.2 billion seat miles, a 9% increase compared to the same period last year. The company attributed this achievement to best-in-class operations, leading the industry in on-time performance and operating 26 days without cancellations during the quarter.

In addition, strong demand for domestic corporate travel, continued international travel, and diversified revenue streams from Loyalty, Premium, Cargo, and MRO (maintenance, repair, and overhaul) enabled Delta to end the last quarter with record revenues in the March quarter. The company reported $11.3 billion in revenue and reversed a net loss of $277 million from last year to a net income of $614 million.

These great results in its most recent quarter demonstrate Delta’s excellent execution in addressing surging demand post-pandemic despite a challenging global economic scenario. The company has effectively seized the opportunity at the right moment.

To further support the bullish thesis, Delta trades at a P/E multiple of only 6.6x (compared to an industry average of almost 20x). This valuation looks even more attractive considering the company’s EPS guidance of $6-7 for 2024, implying bottom-line growth of 6%.

What Is the Price Target for DAL Stock?

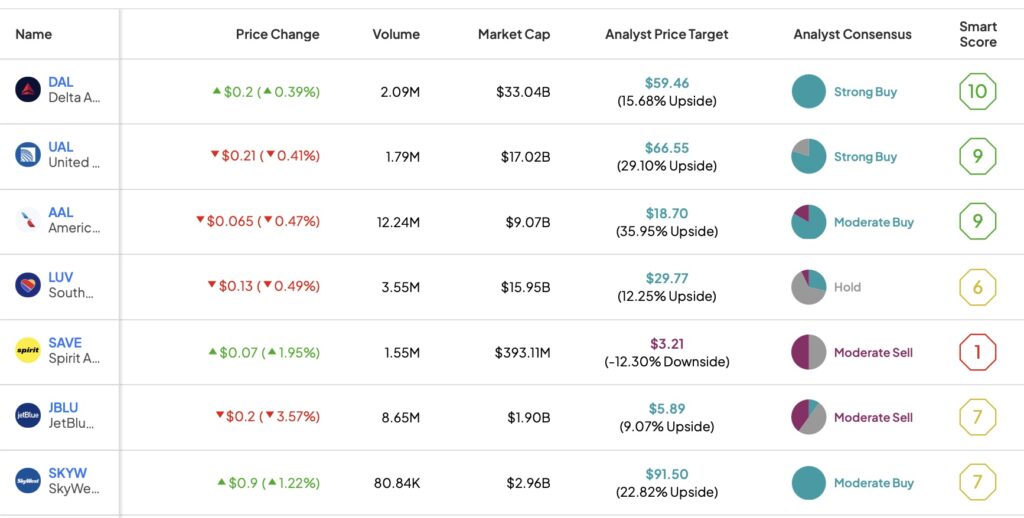

Considering the aforementioned points, it’s understandable that analysts consider DAL stock a Strong Buy, with 18 unanimous Buy ratings assigned in the past three months. The average DAL stock price target of $59.46 implies 14.7% upside potential.

United Airlines (NASDAQ:UAL)

In recent years, United has transitioned from being a growth-oriented company among U.S. legacy airlines to focusing on improving margins and bolstering its balance sheet. Like Delta, United stands out as one of the best U.S. airline stocks in terms of quality today. Examining its balance sheet, the company has effectively managed its leverage, currently at 87% debt-to-assets, as you can see below.

Notably, United avoided issuing additional debt, thanks to a cash infusion from a stock sale in 2020, a strategically sound move that contributed to this achievement.

United’s robust balance sheet is a testament to its stellar operational performance throughout 2023. During this period, United emerged as the world’s largest airline by available seat miles, reporting a total of 73.7 billion.

Furthermore, alongside Delta, United maintained the highest margin per unit among all U.S. legacy airlines. This was demonstrated by its passenger revenue per available seat mile (PRASM) of $16.84, minus its operating cost per unit excluding fuel (CASM-ex) of $12.03, resulting in a $4.81 per unit margin. United’s margins notably outshine those of its U.S. legacy peer, American Airlines (NASDAQ:AAL), which reported a per-unit margin of just $4.32 last year.

In the first quarter of 2024, United increased its capacity by 9.1% compared to the same period in 2023, resulting in total operating revenue of $12.5 billion, up 9.7% yearly. United’s business fundamentals appear to be evolving well, and the valuation multiples the company is trading are attractive, similar to DAL’s.

United trades at a P/E ratio of 6.4x. Moreover, with a projected bottom-line growth rate of around 16% by the end of 2025, the company trades at an appealing PEG ratio of 0.6x (1.0x and under is generally seen as undervalued).

What Is the Price Target for UAL Stock?

Much like Delta, UAL is also viewed as a Strong Buy by Wall Street analysts. Of the 15 analysts who have covered the stock in the last three months, 12 are bullish. The average UAL stock price target is $66.55 per share, implying upside potential of 28.65%.

The Bottom Line

The bullish thesis for Delta and United rests on the balance sheet and margin quality of these two U.S. legacy airlines, which operate in a very risky, high-cyclical sector, particularly sensitive to fluctuations in oil prices.

Given the sector’s characteristics, I don’t consider Delta and United to be ideal long-term investments, given the intense volatility commonly observed in airline stocks. However, among their peers, I believe both stocks stand out as winners today, combining robust fundamentals with de-risked valuations.