CVS Health Corporation (NYSE: CVS) and Walgreens Boots Alliance (NYSE: WBA) have dominated the retail pharmacy industry for decades. Additionally, the two companies feature respectable dividends, which, combined with the overall qualities attached to their business models, could present attractive investment opportunities in the current environment. However, due to Walgreens Boots Alliance’s juicier dividend yield, more robust dividend growth track record, and cheaper valuation, I support that its shares could outperform those of CVS Health.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Therefore, I am bullish on WBA stock and neutral on CVS stock.

Why Pharmacy Stocks Should Remain Solid in Uncertain Times

Before comparing the two companies based on the metrics stated above, let’s establish why retail pharmacy stocks have an advantage during the current highly-uncertain economic environment. Essentially, WBA and CVS are well-positioned to maintain stable cash flows even during a recessionary climate. Due to the two companies dominating the market, holding market shares of 24.5% and 18%, respectively, they enjoy relative strength compared to their industry.

However, most importantly, their financial performance is mostly uncorrelated with the underlying condition of the overall economy. People need to buy their indispensable medicines and relevant products regardless of their discretionary income.

This necessity-type business model is what distinguishes them from most cyclical companies these days. This was demonstrated both during the Great Financial Crisis and during the pandemic. In fact, both companies generated record revenues last year despite enjoying a one-off boost from COVID-19 in 2020.

Which is the Better Dividend Stock?

While both companies are attractive in the current environment due to their quality revenues, WBA’s investment case appears significantly more attractive. WBA appears to be the better dividend stock by most metrics, as well.

Walgreens Boots Alliance’s Dividend Prospects

To begin with, Walgreens boasts a 47-year-long dividend growth track record. This means the company has attained a Dividend Aristocrat status. While its latest dividend hike this past summer was by an insignificant 0.5%, the stock’s yield is currently hovering at roughly 5.8%.

Thus, Walgreens is among the highest-yielding members of the Dividend Aristocrats Index. This is a massive yield, and considering how prolonged and mature this track record is, WBA instantly becomes quite an attractive stock for conservative income-oriented investors.

Here’s what makes WBA’s dividend even more enticing, though. Even if we assume a decline of around 5.2% regarding earnings per share (EPS) this year, in line with consensus EPS estimates, WBA’s payout ratio will stand close to 38%. Therefore, the sizable dividend is well covered.

Sure, WBA’s dividend growth pace is not that attractive right now, as management is being prudent. However, with the payout ratio at such low levels, dividend growth could accelerate at some point in the future.

CVS Health’s Dividend Prospects

When it comes to CVS, the company doesn’t feature the same consistency in terms of growing the dividend, but it has still never cut it since 1996. Instead, dividend-per-share increases have only occurred whenever management saw CVS reaching a new, higher profitability plateau to ensure that dividend payments remain well-covered during economic downturns. For instance, between Fiscal Years 2017-2021, payouts remained steady.

CVS’s latest dividend hike was by a satisfactory rate of 10% – considerably higher than that of WBA. Still, the next hike may not occur until two or three years ahead, which should be kept in mind when comparing the two companies in that regard.

Similar to WBA, CVS has maintained a healthy payout ratio. Based on the midpoint of management’s adjusted EPS guidance of between $8.40 to $8.60, the stock features a payout ratio of just 25.8%. However, CVS stock currently yields just under 2.5%, which is not even half as high as WBA’s, despite WBA’s <40% payout ratio. This is due to CVS’ considerably higher valuation multiple.

Speaking of which, CVS and WBA trade at forward P/E ratios of 9.7x and 7.1x, respectively (using 2023 estimates). Thus, CVS’s valuation thus implies a 37% premium over that of WBA.

Is CVS Stock a Buy, According to Analysts?

Turning to Wall Street, CVS has a Strong Buy consensus rating based on 11 Buys and two Hold ratings appointed in the past three months. At $122.31, the average CVS Health stock forecast suggests 35.75% upside potential.

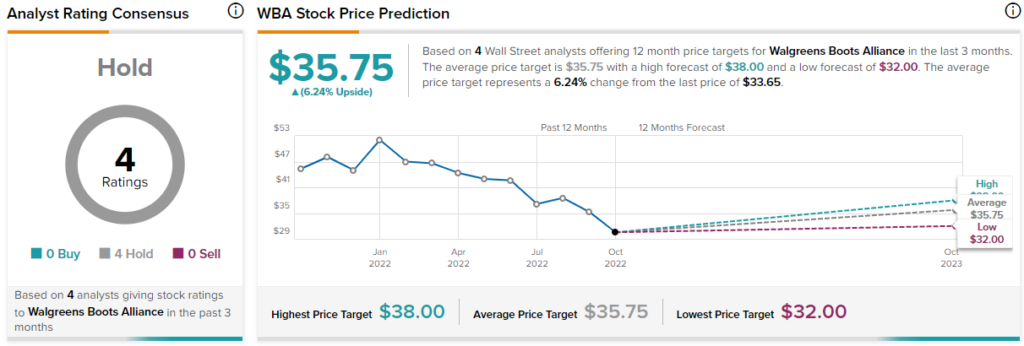

Is WBA Stock a Buy, According to Analysts?

Despite Walgreens Boots Alliance trading at a cheaper valuation, the stock has obtained a Hold consensus rating based on four Holds assigned in the past three months. The average Walgreens stock forecast of $35.75 suggests 6.2% upside potential.

Conclusion: WBA Likely Offers a Better Opportunity

Both CVS and WBA are quality stocks, in my opinion, whose dominance in the retail pharmacy, along with their necessity-type business model, should continue yielding long-lasting financial results.

However, with shares of WBA having corrected violently lately, I believe the stock offers a superior opportunity compared to its biggest competitor. With its mid-single digits valuation and its high yield, WBA offers a wider margin of safety compared to CVS in the current environment. Besides its yield, the stock should offer further upside potential amid a possible valuation expansion once the capital markets cool down.