Costco Wholesale Corporation (COST) specializes in leveraging membership warehouses to offer its member base competitive prices powered by high sales volumes and quick inventory turnover.

Costco currently operates 828 warehouses all over the world, including 572 locations in the United States, Washington, D.C., and Puerto Rico, 105 in Canada, 40 in Mexico, 30 in Japan, 29 in the United Kingdom, and a few more in seven other counties. Costco utilizes e-commerce channels as well, though the company is mostly cherished for its physical retail sales.

Costco’s investment case is truly unique. Its business model sounds simple, though management’s phenomenal execution has differentiated the company massively in the space.

What contrasts Costco from the rest of traditional retailers is its membership plan, which leads to a stable stream of membership revenues for the company.

As a result, Costco can offer goods at a notable discount, which in turn maximizes customer retention, leading to one-of-a-kind economies of scale.

Costco’s expanding presence and growing financials have produced extraordinary shareholder returns over the years. Investors truly love this stock, with shares breaching new record highs continuously. However, this has resulted in an ever-expanding valuation multiple in Costco’s shares, which I believe is hardly sustainable.

While the company features some of the greatest qualities in the space, I believe there will come the point at which investors wake up to the reality that the stock is simply too expensive. Accordingly, I find it difficult to jump on Costco’s bullish train, and hence I am neutral on the stock.

Ever-Lasting Expansion

Costco’s ever-lasting expansion was once again demonstrated in its Q2 2022 results, which came in quite strong. Revenues rose 16.1% year-over-year to $50.94 billion, compared to $43.89 billion last year.

Adjusted comparable sales (which exclude impacts from changes in gasoline prices) in the U.S., Canada, and internationally were 11.3%, 12.4%, and 9% higher year-over-year, respectively, amid strong consumer spending.

Comparable sales were boosted by increased store traffic, which increased 9.3% worldwide, or 8.3% in the U.S., year-over-year in Q2. Average transaction or ticket growth of 4.6% worldwide and 6.9% in the U.S. also boosted results for the period. Costco also grew its e-commerce sales by 12.6%.

Out of total revenues, $967 million were attributed to membership fee income, which comprises Costco’s high-margin cash flows.

All catalysts led to net income growing to $1.29 billion (EPS of $2.92), compared to $951 million (EPS of $2.14) in Q2 2021.

That said, note that last year’s results included $246 million or $0.41 per diluted share in costs resulting mainly from premium wages related to COVID-19.

Despite Costco’s business model being notorious for razor-thin margins in the actual goods sales, the company managed to maintain its gross margins in the double digits.

Still, amid rising costs all across the board, they came in at 12.31%, compared to last quarter’s 12.73%. Net income margins came in close to their usual levels, at 2.5%.

Strong Performance Post-Q2

Costco’s performance subsequent to the quarter-end remained robust, with February’s total comparable sales growing 10.6%. In fact, growth seems to be accelerating lately. Costco shared its March sales recently, with total comparable revenues growing by a remarkable 17.2% year-over-year.

Following its ongoing growth trajectory, Wall Street now expects the company to deliver EPS close to $13.04 for Fiscal 2022, implying year-over-year growth of 17.73%.

Valuation Peak?

The stock has been on a never-ending rally, with no signs of a turnaround.

However, one thing has been changing during this time: how much investors have been paying for the underlying value/growth. As a result of the stock’s extended rally over the past decade, the forward P/E ratio has expanded continuously, inflating from the low 20s to 42.6x.

Could Costco’s perpetual expansion justify this multiple? Maybe. After all, growth remains in the double-digits, while profits are likely to develop if costs come down in the medium term.

However, Costco is a discount retailer at the end of the day. Sure, the qualities of its business model do deserve a premium. For perspective, if Costco’s forward P/E stood at 30x, it would still imply a premium of over 50% versus its industry peers that would reflect these qualities.

A premium north of 100% compared to the industry and net margins standing at 2.5%? That’s a tough proposition for me as an investor.

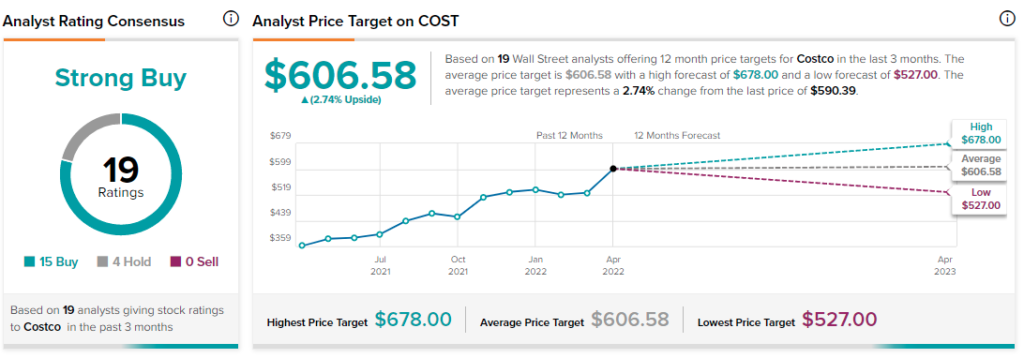

Wall Street’s Take

Turning to Wall Street, Costco has a Strong Buy consensus rating based on 15 Buys and four Holds assigned in the past three months. At $606.58, the average COST price target implies 2.7% upside potential.

Takeaway

Wall Street, apparently, loves Costco stock. Even today, analysts keep assigning Buy ratings with the stock’s valuation at ultra-premium levels. Don’t get me wrong, Costco is likely (one of) the greatest companies in the industry, without a doubt.

However, I believe that the upside could be rather limited at its current price levels. If anything, the case for a valuation compression should be quite strong, in my opinion. Hence, I will remain on the sidelines for now.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure