Since the onset of the pandemic, Costco Wholesale (COST) has had a wonderful time.

The shares of the company have gained close to 55% in the past year, and about 17% in the last six months. The high-octane growth company is famous for its simple business model, and has become a household name by providing a large variety of goods at low prices.

Costco Wholesale operates a chain of membership-only big-box retail stores around the world, and offers branded and private-label products. The company is the fifth-largest retailer in the world, and when it comes to items like prime beef, organic foods, rotisserie chicken, and wine, it is the world’s largest retailer of choice.

As of August 2021, the company operated 815 membership warehouses, of which 564 are in the United States, and the rest are spread across Europe, Asia and North America.

The best thing about Costco is its solid business model that allows the company to generate sizeable profits in any kind of economic environment. The company’s main focus is on the buying power of certain products, which it utilizes to gain the advantage of purchasing leverage and thereafter pass on the savings to customers.

People continue to be drawn to Costco’s Membership cards because of the huge availability of low-cost quality products in its stores. The company has been easily able to retain millions of loyal customers year after year.

These membership cards, which costs at least $60 a year, are a must for anyone who wants to purchase Costco’s low-cost products.

I am bullish on the stock.

Great Financials

Costco has some exceptional financials, and has been outperforming the market in a big way since last year. Its strong financials make it an even more worthy investment.

In Q2 2022, the company was able to generate net sales of $50.9 billion, translating to a 16.1% year-over-year growth. Its net income was $1.29 billion, compared to the net income of $951 million a year ago, and its earnings per share of $2.92 too demonstrated a good 36% yearly hike.

Similarly, in the previous quarter, its sales rose 16.7% and its net income too increased to $1,166 million, translating to earnings per share of $2.62.

As per the second quarter report, its cash position of $11.8 billion is much higher than its total debt of $9.2 billion, thereby ensuring enormous liquidity in the company’s operations.

The best thing about the company’s financials, is the debt-to-equity ratio of 46%, which indicates that the company will have it much easier than most of its peers to sail through economic storms.

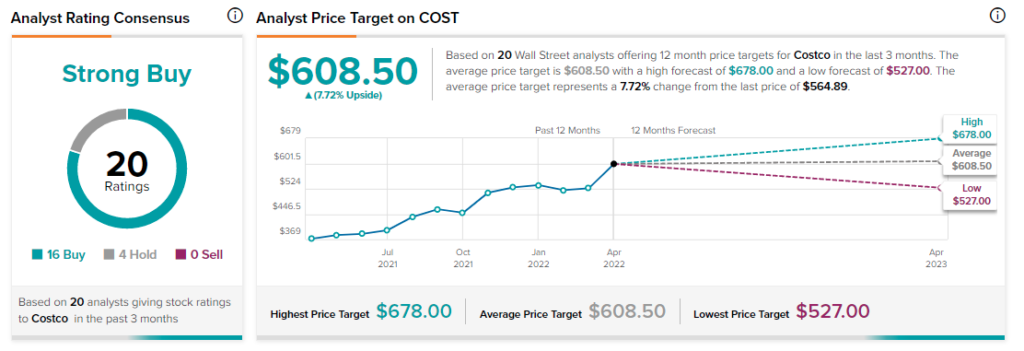

TipRanks gives COST stock a Strong Buy rating, based on 16 Buys and four Holds assigned over the past three months. The average Costco price target of $608.50 suggests 7.7% upside potential.

Possibility of Revenue Hikes

Costco’s customer base has been steadily increasing, which is undoubtedly helping the company increase its sales numbers organically. The company is already a membership retailer, having over 63.4 million paying members worldwide. In the previous quarter, that number was up by a whopping 900,000.

The retention rate of 89.6% is also stellar. This has been possible because the company is literally nailing in its cost leadership strategy by selling bulk sizes at competitive prices.

Other than the general organic growth, Costco’s shares benefitted largely during pandemic restrictions and rising inflation levels. With the threat of another wave of COVID-19 because of the Omicron BA.2 and XE variants, there is a possibility that the company’s sales might get another chance to enjoy some respectable momentum.

The business prospects of Costco are great both in the near and long term. Considering the unpredictability of today’s market, stable investments like Costco shall always be preferred.

The only concern is its high valuation, as the shares are trading at a substantial premium compared to contemporaries.

If one considers the company’s membership model, and robust economic moat, paying a premium for its shares is justified. Still, investors need to decide for themselves if Costco is worth buying at the current price level.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure