Corsair Gaming (NASDAQ: CRSR) has had a rough year, falling over 57% from the all-time high set in February 2021, roughly five months after its IPO.

General pessimism seems to have overtaken the post-IPO excitement, causing the stock to sit just above the initial public trading price.

The market-driven logistic issues are the primary cause of price decline, and will likely be resolved within the year. The underlying product offerings of Corsair are still strong. I am bullish due to the subdued price, and growing product lineup.

Shrinking Margins are Temporary

Supply constraints in many PC components, most notably GPUs, are hindering Corsair. The manufacturers of underlying PC components are feasting on the heightened prices, while system integrators such as Corsair are being hit with cost increases leading to lower margins.

In Corsair’s case, gross margin dropped to 25.92% in Q3 2021 from 27.99% in Q3 2020. Net profit margin has declined more dramatically to 0.45% from 7.95%.

Corsair’s Gaming Components and Systems segment were hit slightly harder than the Peripherals segment; revenue has declined year-over-year by 14.78% and 13.80% respectively.

The overall drop in revenue is 14.4% year-over–year. Due to the difficulties of acquiring and price increases of the core components for PCs, many consumers have foregone purchasing new PCs, which leads to a drop in Corsair products. It is fair to say demand has diminished during the last year.

Temporary Market Issues

Logistic issues have created heightened prices for complementary products, reducing demand for Corsair products. The same logistic issues have increased costs for Corsair.

The double-prong attack of logistic issues has resulted in a gloomy outlook for Corsair’s financials, however, these issues should be resolved in 2022.

The GPU is the key component for any gaming PC, and is the most constrained component at this time, triggering a reduced demand across the industry. Once GPUs are able to hit retail consumers — either through pre-built computers or stand-alone — a rise in demand for Corsair’s products should occur.

Consumers have pent-up demand, many paying significantly higher than MSRP prices for various products. Demand will be able to absorb supply as it increases and returns to pre-COVID levels.

Many investors may be discounting Corsair heavily due to the absence of growth in the last quarter, and lower growth for year-to-date. Investors will return once the broad market issues are relieved, and market catalysts occur.

Major market catalysts which should occur in 2022 are: Intel’s (INTC) launch of GPUs in Q1 2022, the possible end of Ether mining in Q2 2022, and new releases of GPUs by both Nvidia (NVDA) and AMD (AMD), as well as CPUs for AMD in the latter half of 2022.

The company’s value proposition is still strong, even expanding product lines in the stock price downturn.

Notable product lines include: Corsair’s first monitor, the XENEON 32QHD165, an updated popular Dominator RAM lineup for the recently released DDR5, and Elgato FaceCam for content creators.

Over 100 new products have been launched from the start of 2021 to September 30.

Downside Risk is Priced In

Price-to-book is 3.7x, well below industry competitor Logitech’s (LOGI) price-to-book of 6.1x. Downside risk is minimized as the price approaches the underlying book value.

Management has quelled some of the market-driven symptoms by refinancing to a lower coupon rate for long-term debt, as well as increasing inventory in locations closer to consumers. The refinancing of debt has decreased outward cash flows by $2 million a quarter.

An issue which management can’t solve is passing on the additional costs to consumers, who are price sensitive for most of the company’s offerings.

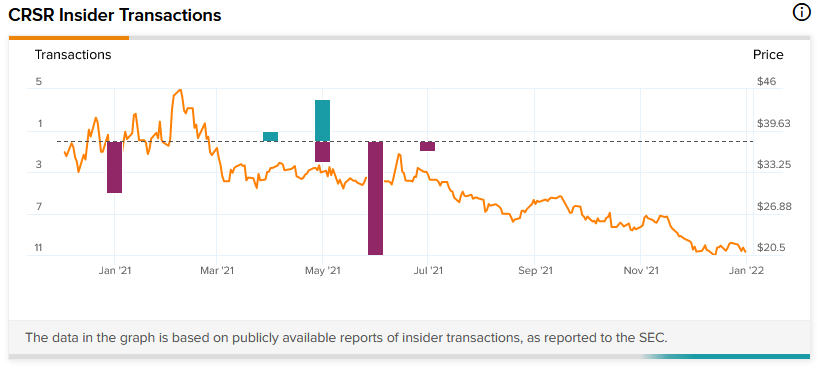

Insiders Are Holding

Insider selling ceased shortly after the initial IPO lock-up ending in July, however no buying has occurred either. Downward pressure may still occur from the private equity company Eagletree Capital, who owns 57% of outstanding shares, and will most likely attempt to exit its position.

You can track insider selling using TipRank’s insider trading tool.

Eagletree has not closed its position, so it is reasonable to assume it values Corsair at a price higher than what it is currently traded at.

Wall Street’s Take

Turning to Wall Street, CRSR stock earns a Moderate Buy consensus rating based on three Holds and three Buy ratings assigned during the past three months.

The average CRSR stock price target of $32.50 implies 54.7% upside potential.

Overall

Corsair has been a victim of market conditions, and while management has attempted to mitigate decline; it is ultimately a price taker and can have a minor impact on market conditions.

Once the logistic issues are resolved in 2022, Corsair should return to greener pastures.

Download the mobile app now, available on iOS and Android

Disclosure: At the time of publication, Brett Rodway did not have a position in any of the securities mentioned in this article.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates Read full disclaimer >