Are higher interest rates bad? Not if you’re Coinbase (COIN), says J.P. Morgan’s Ken Worthington.

Based on the 1-month Treasury yield reaching ~3.75% by the year’s end, the analyst thinks the leading crypto exchange has a “substantial revenue opportunity that originates from higher interest rates.”

How much and how so, then? $1.2 billion, to answer the former question. As for the latter, Worthington explains, “The Coinbase revenue opportunity is more substantial than we see at other financial institutions reflecting some unique investments (USDC) and idiosyncrasies with crypto accounts. The biggest opportunity is from Coinbase’s investment in USDC, but we also expect Coinbase to generate substantial income from customer fiat. We expect Coinbase could keep nearly all interest income, unlike financial peers that pass on some interest income to clients.”

Let’s examine Worthington’s thesis.

USDC represents a $700 million opportunity which stems from the company’s 50/50 JV with Circle in the Centre Consortium which controls the digital stablecoin USDC. The analyst reckons Coinbase has been the recipient of a 25%- 30% revenue share on interest income on USDC reserves. By integrating the USD/USDC order books in July and making a bid to take custody of MakerDao’s $1.6 billion in USDC, Coinbase has taken steps to raise this payout.

The other $500 million will come from ”incremental revenue from interest income” originating from customer cash in fiat ($300 million) and on Coinbase’s corporate balance sheet cash ($200 million). As Coinbase does not seem “poised to rebate higher interest income back to clients,” Worthington thinks the fiat opportunity is not the same as at orthodox brokerage peers. “This leads to particularly high revenue margins as well as operating margins on this incremental revenue,” the analyst explained.

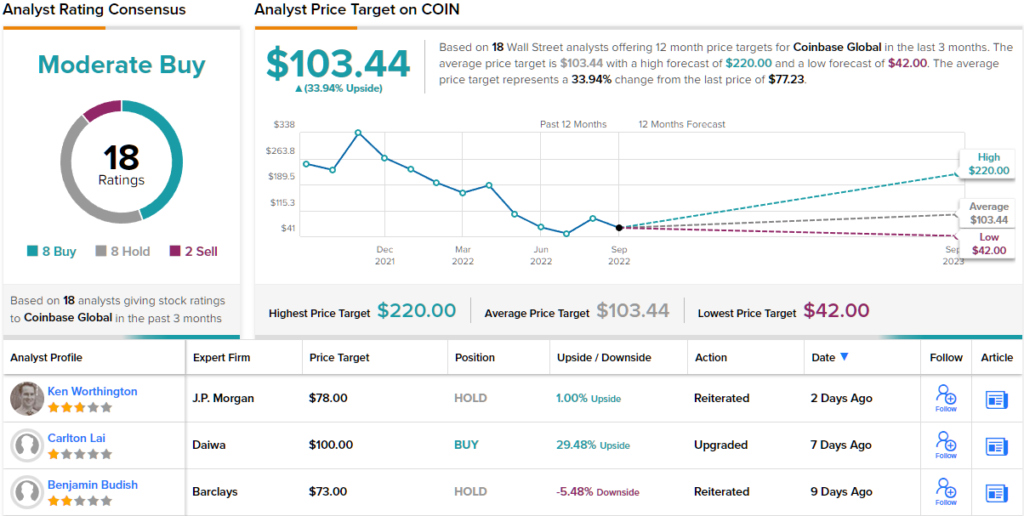

Factoring in these new opportunities, Worthington raises his price target from $64 to $78. Yet, with COIN currently trading at $77.23, the new figure implies shares will remain rangebound for the foreseeable future. Therefore, there’s currently no change to the analyst’s rating, which stays a Neutral. (To watch Worthington’s track record, click here)

Turning now to the rest of the Street, where based on 8 Buys and Holds, each, plus 2 Sells, the consensus view is that this stock is a Moderate Buy. Should the $103.44 average target be met, a year from now, investors could be sitting on returns of ~34%. (See Coinbase stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.