Americans love their pets, as demonstrated by the $126 billion in pet-related expenditures recorded in the U.S. in 2021. With pet ownership dramatically rising over the last couple of years, the space looks ripe for investment, especially with the possibility of a recession right around the corner. In this piece, we used TipRanks’ Comparison Tool to evaluate two pet-related stocks — Chewy (NYSE:CHWY) and Freshpet (NASDAQ:FRPT).

As the overall trends for Chewy and Freshpet are mixed, a long-term bullish view may be appropriate for Chewy, while Freshpet may be better suited to a neutral view.

State of the Pet Care Market

During the pandemic, pet ownership in the U.S. skyrocketed, with the American Society for the Prevention of Cruelty to Animals (ASPCA) estimating that almost one in five American households adopted a pet during the pandemic. That amounted to more than 23 million households.

Of course, the significant increase in pet ownership has also driven demand for pet care products through the roof. This presents opportunities for companies like Chewy, an online retailer that sells all types of pet care products, from food and treats to medications that require a prescription.

One bit of good news right now is that the pet care industry is recession-resistant. In fact, some experts suggest that Americans spend more on their pets during a recession, with one study indicating that consumer spending during the Great Recession declined 3% overall, but spending on pets continued to rise at an annual rate of 5%.

These trends could make some pet care companies look attractive as the threat of a recession looms. However, not all pet care firms are created equal.

Chewy

For investors with a long-term mindset, a bullish view looks appropriate for Chewy. The online retailer appears to be executing well and moving into profitability, but it could take some time for its stock to recover and for its profitability to become secure. As a result, it’s important to emphasize that a long-term view is advisable if considering Chewy stock.

Of that $126 billion Americans spent on their pets in 2021, $50 billion was for pet food and treats, making it the largest category of spending. Online shopping trends show that e-commerce purchases of pet care products ballooned during the pandemic, with 60% of pet owners shopping at brick-and-mortar stores before the pandemic and 86% shopping online in 2021.

Additionally, pet owners have increasingly been buying premium food for their pets, with 40% opting for premium food in 2020. Studies have also found that pet owners who buy premium food typically buy it online. Of course, Chewy is well-positioned to be a key beneficiary of all these trends.

Unfortunately, Chewy’s valuation leaves much to be desired, which is why it may be better as a long-term holding because the business model, trends, and execution look attractive. Chewy reported net sales of $2.43 billion for the second quarter of 2022, a 12.8% year-over-year increase.

Chewy’s gross margin expanded 60 basis points year-over-year to 28.1%, but its net margin remains ultra-low at 0.9%, which was still an expansion of 170 basis points. It’s important to note that e-commerce giants often operate on razor-thin margins, but it’s clear that this is one area Chewy needs to improve.

That said, the online retailer was profitable in the second quarter, reporting $22.3 million in net income and $83.1 million in adjusted EBITDA, an increase of $59.8 million year-over-year. Chewy reported $0.05 per share in earnings, compared to the -$0.12 in losses that had been expected. However, while the company has been growing exponentially on the top line, it hasn’t been profitable on a full-year basis since its initial public offering.

For this reason, many investors will give pause on Chewy, especially at a time when Wall Street is punishing unprofitable companies. Chewy shares are down more than 40% year-to-date. Chewy slashed its full-year sales guidance due to inflation, which is why its stock sold off, presenting a more attractive entry point for a company that appears to have a bright future.

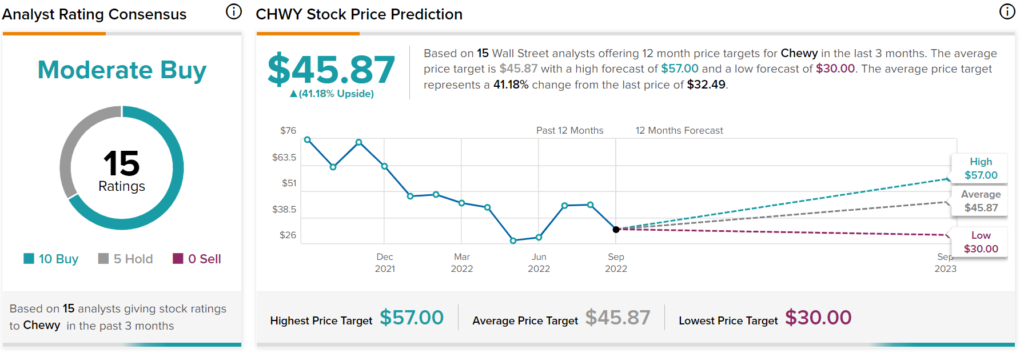

What is the Target Price for Chewy Stock?

Chewy has a Moderate Buy consensus rating based on 10 Buys, five Holds, and zero Sells assigned in the last three months. At $45.87, the average Chewy stock price target implies upside potential of 41.2%.

Freshpet

Chewy addresses the entire pet care industry, but unfortunately, Freshpet only addresses the food market — and only the fresh food market at that. As a result, a neutral rating may be more appropriate for Freshpet, at least until the direction this company will go in becomes clear.

The fresh pet food market in the U.S. is expected to record a compound annual growth rate of 23.62% between 2020-25 on the back of growing new product launches. However, fresh pet food has a significantly shorter shelf life than other foods, reducing the potential growth for the market. The good news is that Freshpet is one of the top two fresh pet food brands dominating the market, with Mars’ Cesar Fresh Chef being the second.

However, other trends are not as attractive for Freshpet. Despite the fact that overall spending on pets increased during the Great Recession, a recession could be bad specifically for Freshpet because it only offers fresh pet foods. In a presentation at the Petfood Forum 2021, a Jefferies analyst reported the results of her survey of pet owners. She found that 81% were feeding dry kibble, while only 17% bought fresh pet food.

However, cost was a significant factor, as 34% of pet owners would buy fresh food if cost were not a factor. Thus, even if spending on pets continues to rise in the next recession, owners may be more inclined to buy more dry food than pay more for fresh food. As far as the Chewy versus Freshpet comparison, Chewy does sell Freshpet’s products, giving it a share of the company’s sales.

Freshpet remains unprofitable, so it’s not as far along as Chewy in its lifecycle. Freshpet reported net sales of $146 million for the most recently completed quarter, a 34.4% increase, although it posted a net loss of $20.6 million compared to the year-ago net loss of $7.5 million. In fact, the company’s full-year losses have been widening over the last few years.

What is the Price Target for FRPT Stock?

Freshpet has a Moderate Buy consensus rating based on 12 Buys, two Holds, and one Sell assigned in the last three months. At $69.85, the average FRPT stock price target implies upside potential of 75.1%.

Conclusion: Bullish on CHWY, Neutral on FRPT

History shows that pet care is a recession-resistant industry, which is something investors should really be thinking about right now. However, Wall Street is displeased with unprofitable companies right now, which is why both stocks are underperforming. Chewy looks closer to profitability than Freshpet, potentially warranting a bullish view for Chewy and a neutral view for Freshpet due to overall industry trends.