Online pet products retailer Chewy (NYSE: CHWY) recently faced several challenges following accelerated growth due to the rapid shift to online channels when the pandemic unfolded.

Shares have tumbled 32.2% year-to-date amid a flight from growth to value stocks, inflation woes, disappointing Q4 FY21 results, and a weak outlook.

Financial Snapshot

Q4 FY21 (ended January 30, 2022) net sales grew 17% to $2.39 billion, lagging the Street’s forecast of $2.42 billion. Moreover, the company swung to an adjusted net loss per share of $0.11 from adjusted EPS of $0.11 in Q420. Analysts were expecting a smaller loss per share of $0.08.

Meanwhile, active customers as of December 31, 2021, grew 7.6% to nearly 20.7 million and net sales per active customer came in at $430, up 15.6% year-over-year.

Q4 FY21 results were adversely impacted by cost inflation, higher inbound freight costs, labor challenges due to Omicron, and the larger-than-anticipated impact from lost sales due to weakened supply chains.

Chewy’s Q1 FY22 net sales guidance of $2.4 billion-$2.43 billion also came in below analyst forecasts of $2.51 billion. Moreover, the FY22 net sales forecast of $10.2 billion-$10.4 billion implies growth in the range of 15%-17%, marking a deceleration from the 24.4% growth seen in FY21.

Growth Strategies

Chewy is pursuing several initiatives to capture additional business, including increasing its penetration into the $35 billion pet healthcare market. The company’s healthcare efforts include Practice Hub (a veterinarian-only marketplace) and the launch of a suite of pet health insurance, wellness, and preventative plans.

Further, Chewy is gearing up to launch its membership program, Chewy Loyalty, in 2023 to drive customer engagement. It will also be introducing sponsored ads on Chewy.com, which will enable its suppliers to advertise to the company’s 21 million active customers.

Wall Street’s Take

Following investor meetings with Chewy’s management, JPMorgan analyst Doug Anmuth noted that despite some near-term “choppiness” related to COVID, the economic reopening, and cost inflation, management was confident it would drive revenue and customer growth, margin expansion, and new initiatives over the next few years.

Anmuth projects 16% revenue growth in FY22 and expects active customer growth to reaccelerate toward the end of 2022.

Based on his optimism, Anmuth reiterated a Buy rating on Chewy with a $55 price target.

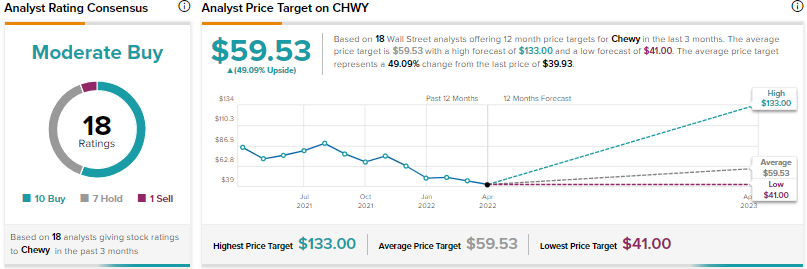

Other analysts on the Street are cautiously optimistic, with a Moderate Buy consensus rating that breaks down into 10 Buys, seven Holds, and one Sell. Given the significant dip in the stock price, the average Chewy price target of $59.53 implies 49.09% upside potential from current levels.

Conclusion

Though the addressable market for pet products and related services is huge, Chewy is facing intense competition from several players, including e-commerce giant Amazon (AMZN). Several analysts seem to be treading cautiously as growth investments, soaring inflation, and supply-chain issues are expected to impact the company’s profitability this year.

Further, TipRanks’ Website Traffic Tool, which uses data from SEMrush Holdings (NYSE: SEMR), indicates that the total estimated visits to Chewy’s website have declined 34.64% sequentially in Q122.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure.