I am neutral on ChemoCentryx (CCXI) as Wall Street analysts are overwhelmingly bullish on it and the average price target indicates strong upside potential over the next year, but the company is not yet profitable and therefore highly speculative.

ChemoCentryx was founded in 1996, and it is headquartered in California. The company operates in the biopharmaceutical industry, and its primary focus remains orally administered therapeutics for rare and orphan diseases. The company has developed a specialization in drugs for cancer, autoimmune diseases, and inflammatory disorders.

According to the company website, ChemoCentryx strives to provide medications and therapeutic solutions to fill the gaps within the current pharmaceutical landscape.

The clinical-stage company also expanded its focus on immuno-oncology and chronic kidney diseases, making its portfolio extensively broad. Although a relatively small team of 133 employees, ChemoCentryx has a significant role in its industry.

Strengths

ChemoCentryx has successfully launched and scaled new products, offering itself a leadership position in the industry. Additionally, the company’s robust associates and dealer network bring it to the forefront with exceptional services, competitive edge, and geographic presence. The company has also created diversified revenue streams with its long line of products catering to various customer segments.

Because of its strong brand image and awareness in the industry as well as markets, ChemoCentryx can charge a premium on its products and maintain an upper hand amongst several competitors.

The company’s growing market share will also prove advantageous in the coming years, and although the company might face downward pressure from time to time, compared to its competitors, it’s still making higher profit margins.

Recent Results

According to Q3 2021 results from September 2021, the company earned revenues totaling $17.7 million. Despite the revenues more than quadrupling from the previous year’s quarterly results, the company faced a net loss of $22.3 million. The basic and diluted per common share data also presented a net loss of $0.32.

The comprehensive loss in 2020’s quarter was $24.3 million, and in 2021 it lowered to $22.3 million. The company increased its research and development expenses from $18.6 million in 2020 to $19.9 million in Q3 2021.

Valuation Metrics

CCXI stock is very difficult to value as it is not profitable, has high growth potential, and is very speculative given the research and development focused orientation of its business model.

Nonetheless, analysts have a highly bullish view of the company’s growth potential as they expect revenue to increase by 132.9% in 2022, and to accelerate even more in the years following the company finally reaching profitability in 2024.

Wall Street’s Take

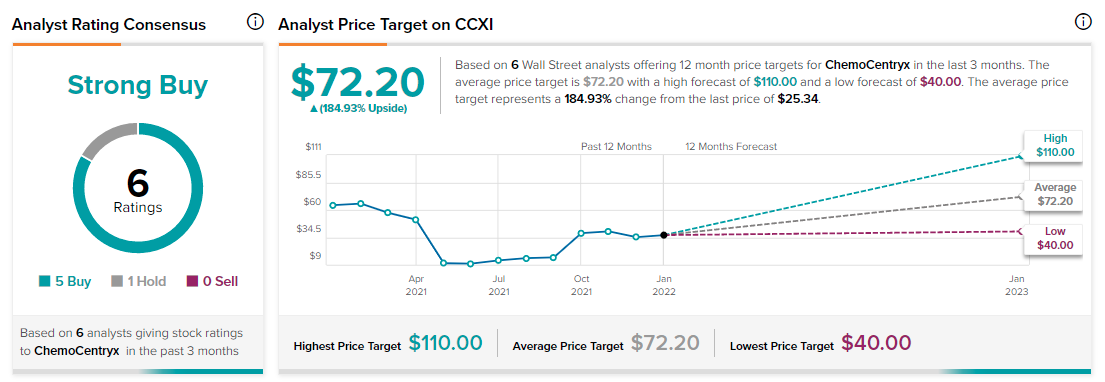

According to Wall Street analysts, CCXI earns a Strong Buy analyst consensus based on five Buy ratings, one Hold rating, and zero Sell ratings in the past three months. Additionally, the average CCXI price target of $72.20 puts the upside potential at 184.9%.

Summary and Conclusions

CCXI stock is backed by a highupside business that is not yet profitable. As a result, it is a very speculative investment as the thesis entirely depends on the research and development team successfully bringing the company’s pipeline to market in order to make company profit.

That said, analysts are nearly unanimously bullish on the stock and the average price target implies massive upside could be in store for shares.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure