Cathie Wood made her name by backing growth-oriented and cutting-edge stocks with her Ark Innovation ETF (ARKK) delivering huge returns for investors before and during the Covid-era. That all changed, however, as market sentiment shifted, and the past two years have seen the once-lauded investor’s reputation take a hit with the ARKK fund posting huge losses.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

But, so far, 2023 is turning out to be a turnaround story. ARKK is up nearly 20% since the turn of the year.

Meanwhile, Wood has been loading up on the equities she sees as game-changers. With this in mind, we decided to track down two stocks she’s been snapping up in recent times. With help from the TipRanks database, we can also gauge general Street sentiment toward these names. Here are the details.

Ginkgo Bioworks Holdings (DNA)

Innovation, you say? Well, Ginkgo Bioworks is a good place to start. Touting itself as the “Organism Company” and likening DNA to computer code, the company’s synthetic biology platform is designed to allow the programming of cells to be as easy as programming computers. The objective is for the company’s cell programming platform to facilitate the growth of biotechnology across a host of different markets, from pharmaceuticals to food to tech and cosmetics.

Synthetic biology is a fast-growing emerging segment with myriad use cases. Between 2030-2040, from bioengineered products used across different end-markets, the company anticipates an aggregate ~$4 trillion yearly direct economic impact.

Right now, however, the numbers are more modest. In its latest quarterly report – for 3Q22 – the company generated revenue of $66.4 million, amounting to a 14.4% year-over-year drop, yet beating Wall Street’s forecast by $5.97 million. There was less luck on the bottom-line, with EPS of -$0.41 falling short of the -$0.20 consensus estimate. The company raised its total revenue outlook for the year from $425 – $440 million to $460 – $480 million (consensus had $435.31 million), a figure Ginkgo said it expects to meet when it provided a 2022 preliminary revenue update recently.

Following the text book for innovative stocks in 2022, Ginkgo shed 80% of its value last year. Wood, though, has been getting the checkbook out; over the past 3 months, she purchased 10,775,507 shares, bringing ARKK’s total holdings to 92,599,090 shares. These are currently worth over $162 million.

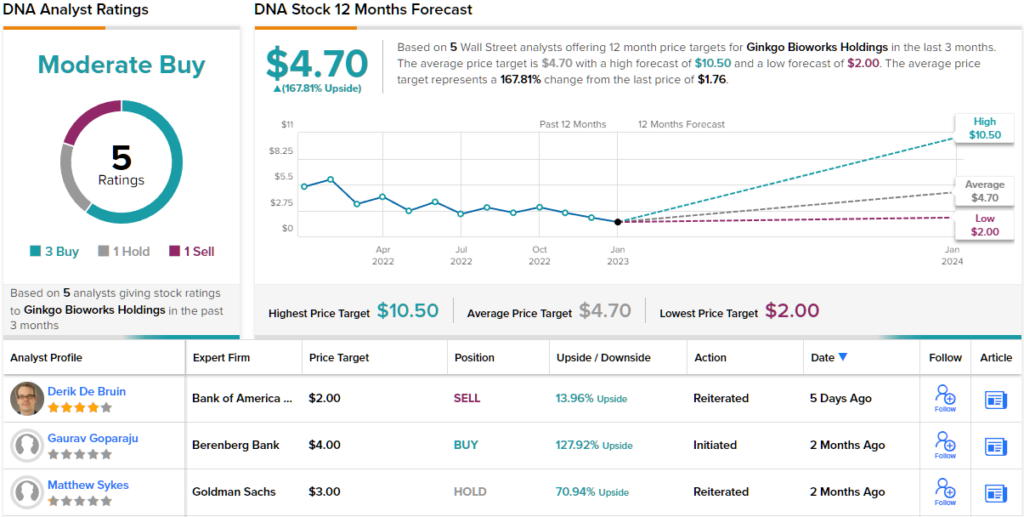

Mirroring Wood’s confidence in Ginkgo, Berenberg analyst Gaurav Goparaju believes the market is “overlooking its horizontal platform execution.”

“Ginkgo has over 130 cumulative programs and 85 active programs across different end-markets as of Q322,” the analyst explained. “Ginkgo leverages both inorganic and organic platform development to both expand its horizontal capabilities and increase its vertical R&D expertise. While other synthetic biology players are vertically integrated, we believe Ginkgo’s horizontal platform is positioned to be the first to effectively industrialize the space at scale, realizing efficiencies from economies of scale.”

Backing up these comments with a Buy rating and $4 price target, Goparaju sees the shares generating returns of a handsome 128% in the year ahead. (To watch Goparaju’s track record, click here)

That figure is no anomaly; the Street’s average target stands at $4.70, making room for one-year gains of ~168%. With a ratings breakdown of 3 Buys, and 1 Hold and Sell, each, the analyst consensus rates the stock a Moderate Buy. (See DNA stock forecast)

Teladoc Health, Inc. (TDOC)

Wood specializes in disruption and the next stock we’ll look at offers just that. Targeting a new way for people to access healthcare, Teladoc is a pioneer of the telehealth industry, making medical care available remotely. By doing so, users can avoid the tedious process of waiting rooms, pricy fees and schedule mix-ups, with the benefit of on-demand video calls with doctors.

Such a value proposition was tailor-made for the Covid-era and the stock was a big winner during the pandemic. While there have been fears that in a post-pandemic world, the solutions will lose their luster, the latest 3Q22 results offer a counter argument.

Revenue increased by 17.2% year-over-year to $611 million, while slightly beating the Street’s call by $2.41 million. The reopening doesn’t seem to have dampened visits, which grew by 14% to 4.5 million in Q3. And for the first nine months of the year, total visits reached 14 million, well above the 7.6 million seen during the same time in 2020, the year when demand for telehealth services last spiked.

At the bottom-line, EPS of -$0.45 beat the -$0.57 anticipated by the analysts. However, the lack of profitability was a big no-no for investors in 2022 and the stock hit the skids to the tune of 74%. That said, the company has taken steps to address that issue and recently announced a restructuring plan, whereby the company will cut the workforce and reduce office space in an effort to lower operating costs and attain profitability.

Meanwhile, Wood has been loading up. She bought 279,131 shares over the past 3 months, making ARKK’s overall holding total 11,329,465 shares. At the current price, these are worth more than $304 million.

Addressing recent developments, RBC analyst Sean Dodge notes the restructuring plans’ potential impact on sentiment. He writes, “While we still believe investors very much view TDOC as a growth story, we do appreciate the effort to balance that growth with margin expansion and expect investors to be more receptive in this market.”

Standing squarely in the bull camp, Dodge rates TDOC an Outperform (i.e. Buy), and his $35 price target implies a ~30% upside for the next 12 months. (To watch Dodge’s track record, click here)

Most on the Street are taking a more skeptical view; the stock claims a Hold consensus rating, based on 14 Holds vs. 4 Buys. Nevertheless, the $32.63 average target is set to yield returns of 21% over the coming year. (See TDOC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.