The Amarin (AMRN) vs the Generics drama has entered a new stage. For the uninitiated, a quick recap: In March, Amarin lost a patent trial against two generic drug makers (Dr Reddy’s and Hikma Pharmaceuticals) seeking to sell their own versions of Amarin’s high triglycerides treatment, Vascepa.

Amarin has now filed its appeal with the U.S. Court of Appeals for the Federal Circuit. As Vascepa is Amarin’s sole product, much hinders on the appeal’s outcome.

Taking the opportunity to assess Amarin’s case, H.C. Wainwright analyst Andrew Fein consulted a patent attorney for an “initial perspective” on Amarin’s opening appeal brief.

“We point out that the appeals court reviews issues of law de novo and issues of fact for clear error. The clearly erroneous standard is highly deferential to the district court, while the de novo standard permits the appellate court to substitute its own judgment for that of the district court,” Fein explained.

So basically, Amarin will have the upper hand, if it can convincingly argue the district court made a mistake when reaching its conclusion.

According to the patent attorney, Amarin has presented its case in the “best way possible,” with the brief laying out Amarin’s tech, the background to the invention, the reason it was needed and the company’s approach when trying “to solve the problem of lowering triglycerides (TGs) in patients with severe hyperlipidemia without raising LDLs.”

Scouring the content, Fein notes Amarin’s appeal rests on two lines of argument: “(1) that the court erred in finding a prima facie case of obviousness because it did not apply the correct analytical framework; and (2) that the court erred in its approach to secondary considerations.”

Fein notes the attorney found Amarin’s second line of argument particularly persuasive, “both on the merits and on the clarity and force of argument.”

Fein concludes optimistically, “The company only needs to be right on one.”

The saga now awaits the generics’ response brief, which is anticipated by June 16, with Amarin’s reply brief expected by June 26. The appeal court’s ruling is anticipated by the end of 2020 or early 2021.

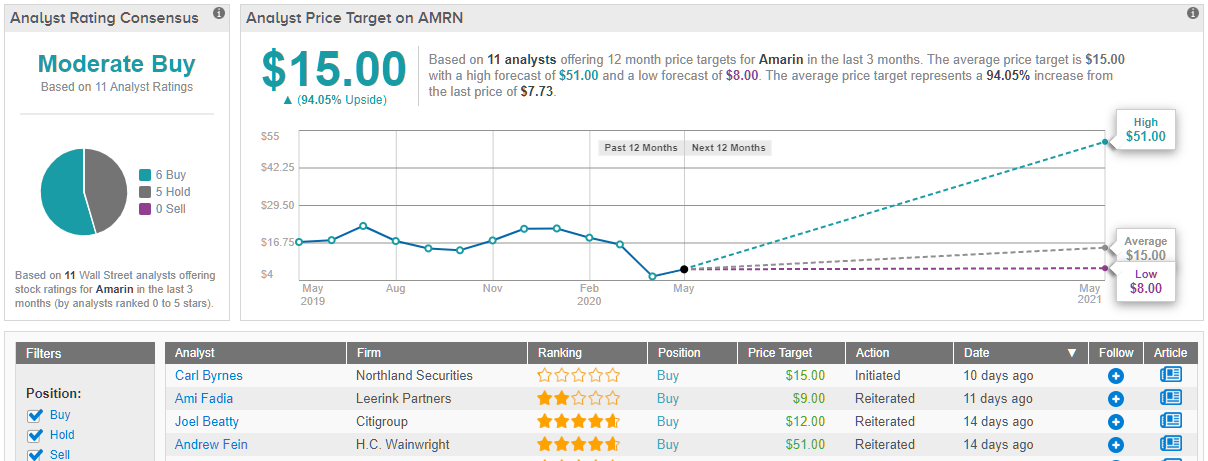

Until further developments, Fein stays with the bulls. The 5-star analyst rates Amarin shares a Buy, along with a $51 price target. The implication for investors? Upside of a generic busting 560% from current levels. (To watch Fein’s track record, click here)

Overall, Wall Street is split between the bulls and those choosing to play it safe. Based on 15 analysts polled in the last 3 months, 6 rate AMRN stock a Buy, while the other 5 remain sidelined. Notably, the 12-month average price target stands at $15, marking about 94% upside potential. In other words, even the analysts that are hedging their bets have some optimism reflected in expectations. (See Amarin stock analysis on TipRanks)

To find good ideas for healthcare stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.