The semiconductor chip industry has been in the news of late – but mostly due to the global chip shortage that is impacting a multitude of downstream industries worldwide. The computer chip backlog is exacerbated by the heavy crimps in the supply chain, and the result has been lower production and headaches for production managers.

So let’s look at the bright side. It’s earnings season, and several semiconductor companies will be reporting this week – and from their end, the picture’s not so gloomy. Annual chip sales rose more than 10% in 2020, and are projected to rise another 17% in 2021. The chip industry is estimated to be worth some $527 billion this year, and is projected to reach $600 billion by 2025.

Among the factors boosting semiconductor chips are the global shift to the new 5G wireless platform, the newest iteration of X86 server chips, and increased sales of notebook computers, game consoles, and smart home systems. All of these will need silicon chips.

Checking in on some of the chip companies that will be reporting this week is 5-star analyst Hans Mosesmann of Rosenblatt Securities. Mosesmann has turned his eye particularly on three stocks that he sees as winners in the current environment. We’ve used the TipRanks database to pull up the details on his picks; these are Buy-rated stocks that have seen share price gains in recent weeks. Let’s see what else they have to offer, and take a look at Mosesmann’s commentary, too.

Monolithic Power Systems (MPWR)

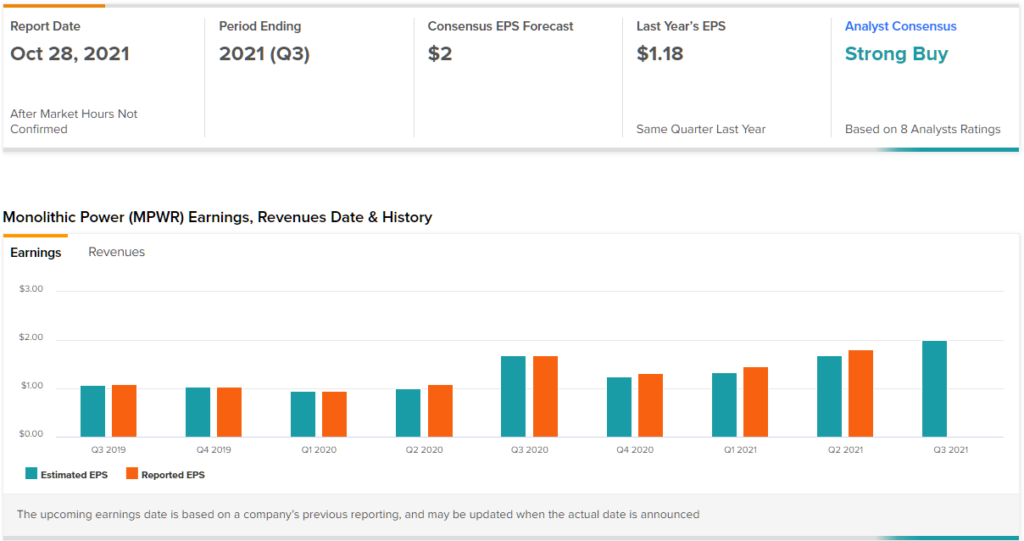

First up is Monolithic Power Systems, Washington State-based tech company that specializes in power circuits and converters. Monolithic’s products are found in a wide range of devices, both digital and analog, and have applications in portable electronics, cloud computing, telecom infrastructure, wireless handsets, medical equipment, and automobiles. Monolithic saw more than $844 million in total revenues in 2020, and it has already reached more than half that level, $547 million, in 1H21.

After a volatile start to the year, shares in MPWR have been rising steadily since mid-May. The stock is up an impressive 63% for the last 12 months, nearly double the NASDAQ’s 34% gain in the same period. These gains have come as the company posted its 55% year-over-year revenue gains for the first half of 2021.

It wasn’t just revenues that grew. Monolithic’s Q2 EPS came in at $1.81, up 67% from the $1.08 posed one year earlier – and also beating the expectations by 7%. The company credited strong demand – and increased revenues in all of its end user markets – for the gains. Monolithic is scheduled to report its Q3 earnings on October 28, after the markets close.

Rosenblatt’s Mosesmann is upbeat about Monolithic’s upcoming earnings, writing: “We expect sales to be above our/consensus estimates of high-single-digit q/q growth and EPS of $1.99/$1.99. We see the September quarter being driven by broad-based growth, especially in Compute & Storage, Automotive, and Consumer… We see the December guide coming in above our/consensus estimates of a low-single-digit sequential decline and EPS above our/ consensus $1.78/$1.82 estimate.”

“We see positive tailwinds continuing for MPS surrounding several end-markets including continued momentum in Industrial & Automotive, as well as catalysts including, new platform ramps in servers (Intel and AMD), 5G, and the automotive new model year (old-school players realizing that to catch up, they need to adopt more flexible and innovative power/ management solutions based on MPWR technology),” the analyst added.

In line with these comments, Mosesmann rates the stock a Buy, and his $620 price target suggests a one-year upside of 19%. (See MPWR stock analysis on TipRanks)

Advanced Micro Devices (AMD)

Next up is AMD, one of the industry’s top companies, measured by sales. AMD saw $9.5 billion in chip sales in 2020, up 41% from the $6.7 billion in 2019. AMD offers a range of products, including X86 microprocessors, accelerated processing units (APUs), and graphics processing units (GPUs). The company’s GPUs are in particular demand by the PC gamer market, as well as datacenter managers.

Heading into AMD’s Q3 earnings – due out on October 26 – it can be beneficial to check in with the last quarterly report. The company brought in $3.85 billion at the top line, up 99% year-over-year, and marking the fifth consecutive quarter of sequential gains. The company’s EPS, at 63 cents, was more than triple the 18 cents reported in the prior year’s Q2.

In recent weeks, AMD’s product lines have been making some headlines. The company announced on September 30 that it had entered a collaboration with Google Cloud, providing EPYC 7003 series processors to deliver 30% better price-performance. This was followed on October 5 by a joint notice with Microsoft that 175 of AMD’s top chip lines are compatible with the Windows 11 operating system. And most recently, on October 21, AMD and Nvidia announced a collaboration on new, faster, gaming systems – powered by AMD’s Ryzen Threadripper processing chips.

Turning to Mosesmann’s view, the analyst lays out a series of solid reasons to take a bullish stance on AMD, writing, “We continue to believe AMD can capture 50% of the entire x86 CPU market in coming years on technology/product roadmaps, accelerating design pipelines, increasing attach rates of GPUs to optimize EPYC server CPUs, etc. Execution, TAM, roadmap, and a benign competitive environment are tailwinds for AMD.”

The Rosenblatt analyst gives AMD shares a Buy rating with a $150 price target indicating room for 23% share appreciation in the next 12 months. (See AMD stock analysis on TipRanks)

Texas Instruments (TXN)

Last up is a venerable name in the chip industry, Texas Instruments. TI, based in Dallas, is one of the world’s largest producers of analog technology, and is a major manufacturer of semiconductors and integrated circuits. TI is especially well known for its educational products, including one of the market’s best-selling graphics calculator. Analog chips and embedded processors make up the lion’s share of the company’s revenue, which in 2020 totaled nearly $13.1 billion. That total made TI the ninth-largest chip company by sales volume.

The company’s revenues and earnings have been growing steadily since the fourth quarter of 2019. In the last reported quarter, TI showed $4.58 billion at the top line, up 41% yoy, and earnings of $2.05 per share, which was up from $1.48 in the year-ago quarter. Looking ahead to the October 26 Q3 release, the company is guiding toward a revenue range of $4.4 billion to $4.76 billion, and an EPS range of $1.87 to $2.13.

For more than a decade, TI has averaged approximately 12% annual fee cash flow growth, and FCF in Q2 hit $6.5 billion. The company has a long-standing policy of returning cash and profits to shareholders, via buybacks and dividend payments. TI this month declared its Q4 dividend, at $1.15 per common share, up 13% from the previous quarter. At the annualized rate of $4.60, the dividend gives a yield of 2.2%.

Hans Mosesmann takes a sanguine view of TI ahead of earnings, writing of the outlook, “We see the Street focusing on the 4Q21 guide, which we see TI reporting sales above our/consensus estimates of a low-single-digits q/q decline and EPS of $1.97/$1.95. We see Analog and Embedded coming in flat-to-slightly down q/q, while Automotive and Industrial endmarkets continue to be strong. In addition, we see TI’s online presence a benefit to the company. We see the continued emphasis on Industrial & Automotive, more balanced analog/embedded growth vectors, and strong excess cash return setting up TI nicely as 2021 commences.”

These comments back up Mosesmann’s Buy rating, and his $230 price target implies ~15% one-year upside potential. (See TXN stock analysis on TipRanks)

To find good ideas for chip stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.