Investing is a two-way Street. That is, for every buyer there must be a seller too. The market’s overall performance is defined by whoever wrestles control of the narrative.

Until recently, it was clear the sellers had been the dominant force in 2022, but change is in the air and the markets have been ticking higher. Oppenheimer technical analyst Ari Wald thinks that a certain subset of stocks is ready to use this development to its advantage.

“While we’re using small-cap growth to measure market risk and upside, we think large-cap growth offers an attractive balance between near-term rotation potential within intact long-term strength,” Wald wrote. “As a proxy for this theme, the NASDAQ-100’s (QQQ) failed breakdown below May 2021 support vs. the S&P 500 is indicative of selling exhaustion (also called a “bear trap”) and argues for additional outperformance over the coming weeks, based on our work.”

Against this backdrop, Wald’s colleagues at Oppenheimer have pinpointed 3 large-cap stocks which they believe are set to push ahead over the coming months. They are a varied lot, operating in different segments, with one trait in common; the Oppenheimer analysts see all 3 adding at least 50% of gains in the year ahead.

With a little help from the TipRanks database, we can also gauge Street sentiment toward these big players. Let’s get into the details.

T Mobile US (TMUS)

We’ll kick off with a telecoms giant. T-Mobile is the US’s second-largest wireless carrier, seeing out 2021 with 108.7 million subscribers. For these customers the company offers voice, messaging, and data services, as well as wireless devices – from smartphones to tablets to wearables, amongst others. Naturally, we’re talking about a huge company, with 75,000 employees and a market cap over $155 billion.

Since 2013, TMUS has captured a huge chunk of the wireless carrier industry’s growth. Its massively improved network and inventive marketing for underserved corners in both urban and rural areas resulted in real-world share gains. That said, there have been worries about rising competition, and following the 2020 merger with Sprint, concerns about profitability. However, the company assuaged investors’ fears following the latest earnings report – for 4Q21.

Although revenue of $20.79 billion came in shy of Street expectations by $260 million, EPS of $0.34 came in ahead of the consensus estimate by $0.18. Total postpaid net customer additions reached 1.75 million and for the full-year came in at 5.5 million. The company’s guidance had these coming in between 5.1 million to 5.3 million.

Even better, investors were pleased with the outlook. The company guided for postpaid customer net additions of 5.5 million in 2022, slightly ahead of Wall Street’s 5.2 million forecast. T-Mobile is known for heeding caution with its guidance, and for 8 consecutive years has beaten its subscriber-growth outlook.

Oppenheimer analyst Timothy Horan thinks the “momentum from 2021 will position TMUS for a strong year of growth in 2022.”

“High speed internet service will be a key sector with promising growth potential,” the 5-star analyst said. Around 40% of TMUS high speed internet customers are completely new to TMUS, unlocking a unique opportunity to cross-sell mobile services… TMUS is in the early innings of growing services revenues from underindexed markets, key to unlocking up to $60B of stock buybacks long-term. With more of its 2.5GHz deployed, its 5G network quality is improving at an impressive clip, highlighted by lower churn and superior performance relative to peers.”

Conveying his confidence, Horan rates TMUS an Outperform (i.e. Buy) while his $190 price target makes room for upside of 53%. (To watch Horan’s track record, click here)

It’s not often that the analysts all agree on a stock, so when it does happen, take note. TMUS’ Strong Buy consensus rating is based on a unanimous 15 Buys. The stock’s $167.07 average price target suggests ~34% from the current share price of $124.29. (See T-Mobile stock forecast on TipRanks)

PayPal (PYPL)

Our next large-cap needs no introduction either. PayPal is the online payments leader, with a huge worldwide footprint. Via a wide selection of payment solutions, its platform enables businesses to accept payments from online merchants and mobile devices/apps. Its services also include peer-to-peer (P2P) payment app Venmo, PayPal Credit, payments platform Braintree, commerce tools provider Zettle, and crypto offerings, amongst others. The company has 360 million active customers in 200+ markets across the globe and it boasts a market cap of $132.53 billion.

That said, not long ago, that market cap was some way larger, and you could say PayPal has suffered from its own success. The company was one of the pandemic era’s big success stories, as more consumers turned online and embraced ecommerce. The market’s change of direction, amidst heightened fears of inflation and rising interest rates have hammered the valuations of many previous high-flyers.

The company has also offered some mixed earnings, as evidenced in the recent 4Q21 results and outlook. The quarterly display was decent; revenue increased by 13.1% year-over-year to reach $6.92 billion whilst coming in ahead of the $6.87 billion the Street had expected, and at $1.11, adj. EPS just missed the consensus estimate by $0.01.

However, the real disappointment lay in the outlook. For Q1, PayPal anticipates adj. EPS of $0.87, falling short of Wall Street’s $1.16 forecast. For the full year, the company expects revenue growth between 15% to 17%. The Analysts were looking for revenue growth of 17.9%.

Following the report’s release, the shares cratered, further depressing an already beaten-down stock. However, Oppenheimer analyst Dominick Gabriele senses it is time to pounce.

“Reduced expectations create the opportunity we were waiting for,” the analyst wrote. “After our post-3Q21 cautious stance we see significant upside on the kitchen-sinked outlook/soured sentiment and we’re going bottom fishing (grab your G. Loomis)… The company’s two-sided digital payments platform is a valuable and difficult-to-replicate asset exhibiting strong network effects. We think PYPL is particularly well positioned to benefit as retail activity continues to migrate from brick-and-mortar stores toward online and mobile venues.”

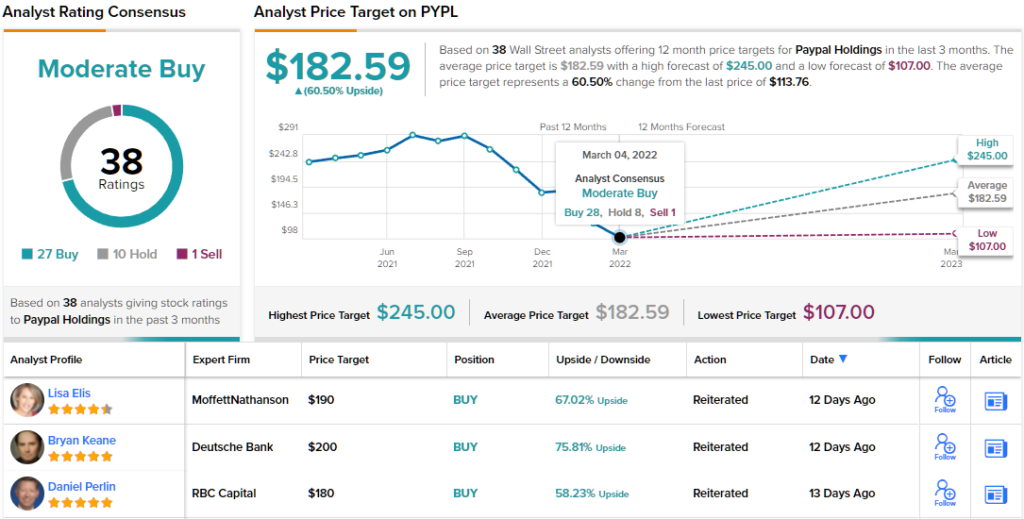

To this end, Gabriele rates PYPL an Outperform (i.e. Buy) along with a $190 price target, suggesting shares could climb 67% higher over the one-year timeframe. (To watch Gabriele’s track record, click here)

The Street’s average price target is only slightly lower; at $182.59, the figure represents potential upside of 60%. Rating wise, the picture is more nuanced; based on 27 Buys, 10 Holds and 1 Sell, the stock has a Moderate Buy consensus rating. (See PayPal stock forecast on TipRanks)

Atlassian (TEAM)

The final promising large-cap we’ll look at is the smallest member on this list with a market cap of a “mere” $72 billion. The Sydney, Australia-based company operates in the SaaS space, being a provider of workflow and collaboration tools, and a proponent of teamwork, as implied by the ticker.

Amongst its products, Atlassian offers the Confluence platform, a team workspace both for personal and professional use, task and project organizer Trello, and code sharing and management service Bitbucket. But the flagship product is workflow management system Jira, which software teams use for managing work and projects.

Atlassian stock has suffered at the hands of market rotation, with the shares down by 31% over the past 6 months. While the shares might be subject to the market’s whims, during the period the company delivered an excellent quarterly financial statement – for F2Q22.

The company generated revenue of $688.53 million, amounting to a 37% year-over-year uptick and beating the consensus estimate of $641.3 million. EPS of -$0.31 also improved on the analysts’ forecast – by $0.03.

And where so many have stumbled recently, TEAM delivered the goods with its outlook. For FQ3, revenue is anticipated to be in the $690 million and $705 million range. Consensus had $664.56 million.

The company has been pivoting its business toward the cloud, a factor which informs part of Oppenheimer’s Ittai Kidron’s bullish slant.

“We see a long runway for growth supported by multiple levers (TAM expansion, cloud transition, product innovation, free/starter conversion, pricing, etc.) and believe Atlassian can maintain elevated growth through its cloud transition,” says the 5-star analyst. “Despite NT challenges (tough comps in F3Q22, EOL for perpetual licenses in F4Q22, GM pressure, OpEx investment, management transitions), there is no change to our positive thesis and bullish LT stance.”

Based on the above, Kidron puts an Outperform (i.e. Buy) rating on TEAM shares to go with a $430 price target. The implication for investors? Upside of 51%. (To watch Kidron’s track record, click here)

Looking at the consensus breakdown, based on 9 Buys and 5 Holds, this stock claims a Moderate Buy consensus rating. There are decent gains projected here; going by the $412.93 average target, the shares will appreciate by 45% over the coming months. (See TEAM stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.