Even though cloud computing has been around for over 20 years – the innovator in the space was Saleforce.com (CRM) – the market continues to grow at a rapid pace. The fact is that this technology offers much more flexibility, integration and access to data. There are also many large companies that are looking to migrate their legacy systems to the cloud to achieve digital transformation.

Of course, the COVID-19 pandemic has been another catalyst. Companies have had to scramble to use systems to allow for remote work environments.

So, in light of all this, it should be no surprise that cloud stocks have been a great trade. For the past five years, the First Trust Cloud Computing ETF (SKYY) has soared from $29 to $97.

That said, there are some cloud companies that have been left out of the party on Wall Street. Take a look at Box (BOX).

Founded in 2005, the company is one of the pioneers of cloud-based storage systems. Co-founder and CEO Aaron Levie actually became a celebrity in the tech world. He also had little trouble raising substantial amounts of venture capital from top firms like Andreessen Horowitz, DST Global and Coatue.

In 2015, he would take the company public at $14 a share and the price would jump to $23. However, the good times would not last for long. Wall Street would get antsy about the substantial net losses and the intense competition, which included players like Microsoft (MSFT), Dropbox (DBX), and Alphabet (GOOGL). On top of this, there were the struggles to gin up the growth.

The result? Box has been a poor investment. Since the IPO, shares are actually down 4%.

But any bearishness may be an overreaction. For the most part, Box does look like an interesting opportunity right now.

Why Box Now?

Over the years, Box has taken tough measures to reduce the cost structure. Because of this, the company has been profitable (at least on a non-GAAP basis) and generates positive operating cash flows ($57.5 million in the latest quarter).

But the nagging issue is the top-line as it has remained sluggish. During the fiscal fourth quarter, it only increased 8% to $199 million.

However, there are some catalysts that should drive a turnaround, with the company aggressively innovating its platform.

One of the offerings is Box Shuttle. This focuses on a major market opportunity – that is, to help organizations with the heavy costs and complexities of transitioning to the cloud. Box Shuttle is an easy-to-use system that works with a variety of on-premises legacy systems like OpenText, Documentum and SharePoint.

In addition, Box has added a variety of applications to help provide for cybersecurity, governance and workflow automation. Then there have been software versions for different verticals like life sciences, media/entertainment, professional services, banking, retail and tech.

But perhaps the most interesting new product is Box Sign, which provides native e-signature capabilities. A key part of the technology came through the acquisition of SignRequest.

Box Sign is really a perfect fit for the Box platform. Levie stated on the earnings call, “There are an incredible number of use cases that Box Sign will address for our customers. For example, legal teams will be able to create and finalize contracts within Box, from drafting and co-editing to signing and retaining the agreement with Box Governance. HR teams will be able to initiate and complete offer letters using Box Relay together with Box Sign. Sales teams can initiate digital customer contracts for signature right from Salesforce and compliance teams will be able to retain and protect executed agreements while securing sensitive content with Box Shield.”

As seen with DocuSign (DOCU), the e-signature business is definitely lucrative and continues to grow. Since the company’s IPO in 2018, shares have risen from $40 to around $220.

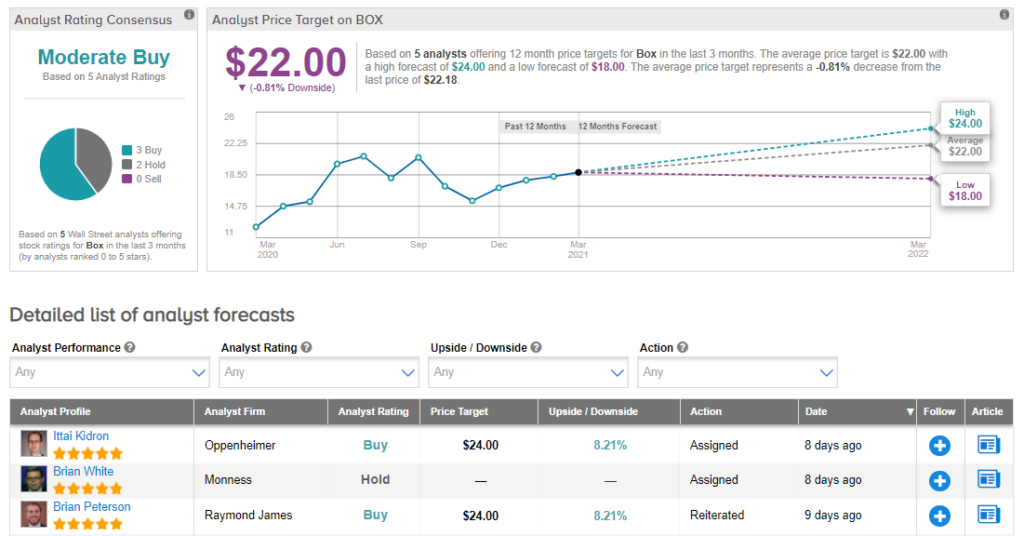

Analysts Weigh In

Turning to the analyst community, 3 Buys and 2 Holds have been assigned in the last three months. So, Box has a Moderate Buy consensus rating. Additionally, the $22 average analyst price target implies 1% downside potential. (See Box stock analysis on TipRanks)

Conclusion

Gaining traction will take some time for Box, but the company appears to be heading in the right direction – and the product pipeline looks encouraging.

Besides, the valuation is attractive, especially when compared to the outsized multiples in the cloud industry. Note that the company is trading at about 4.3 times sales. Thus, as the business starts to pick up some momentum, there should be nice gains for investors.

Disclosure: Tom Taulli owns shares in Box.

Disclaimer: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities.