Fintech stocks were one of the canaries in the coal mine in 2021, as euphoria quickly turned to fear. It was the fear of higher interest rates that knocked fintech darlings off the podium. The rest of the overpriced tech scene was quick to follow, with accelerating losses this year. In this article, we’ll compare two beaten-down fintech stocks, Block (NYSE: SQ) and PayPal (NASDAQ: PYPL), to see which is the better Buy. Based on upside potential from analyst targets, SQ comes out on top, but let’s dig deeper.

It’s easy to look back at the top fintech stocks as obvious bubbles. Price-to-earnings (P/E) and price-to-sales (P/S) multiples were stretched as euphoric investors became increasingly willing to pay more for innovation and exciting growth stories. Ark Invest’s Cathie Wood was one of the most exciting money managers, with a focus on the most innovative and disruptive forces in tech.

By focusing on huge total addressable markets and forward-thinking technologies, one can justify paying a bit of a premium. Such a premium quickly swelled as investors looked to the tech sector as a critical industry to navigating out of pandemic-era lockdowns. While the pandemic may have accelerated various technological trends, including fintech, it soon became clear that the post-2020 tech boom overextended to the upside, setting the stage for a harrowing crash in many of the “story-driven” stocks.

As the Federal Reserve continues to raise interest rates, it’s become harder to value fintech based on its hazy growth stories. Just over a year ago, it seemed like the fintech leaders would put the traditional banks on notice.

The old banks have been wildly profitable for hundreds of years, and fintech was seen as the disruptive force to put them on their knees. Fast-forward to today, and it’s now apparent that fintech investor ambitions were slightly exaggerated. Strong balance sheets matter more than ever now that credit is harder to come by. With deep pockets and innovative capabilities of their own, the banks now have the edge over the fallen fintech companies.

Over the long run, the fintechs will likely be able to cut further into the turf of the big banks. However, don’t expect the big banks to go down without a fight. The banks aren’t going anywhere. If anything, today’s hot fintechs may evolve to become just another bank as they look to expand their financial service offerings.

Now that expectations have been reset, it may be wise to give the beaten-down fintechs a second look. Block and PayPal stock collapsed 78% and 76%, respectively, from peak to trough. Each firm had unrealistically high expectations just over a year ago. Today, expectations may be unrealistically low.

Block (SQ)

Block, formerly Square, underwent a name change as the firm looked to move above and beyond payments. Undoubtedly, CEO Jack Dorsey is one of the most exciting men to bet on. He’s one of the tech founders that you could argue is a visionary.

Right now, Dorsey has his sights set on bitcoin (BTC-USD) and cryptocurrencies. With “crypto winter” quickly approaching, Dorsey’s blockchain ambitions seem less worthy of paying up for. In any case, Dorsey is focused on the truly long term. Block’s secretive blockchain and crypto projects will likely outlast the coming “crypto winter,” potentially fueling the next boom in the asset class.

Though I’m no fan of cryptocurrencies, I think there’s no denying the potential behind blockchain technology. It could hold the keys to how a vast majority of consumers transact 10 years down the road. It’s fine to be excited about the potential behind emerging technologies.

However, investors must be careful how they bet on certain technological trends. Just because blockchain and crypto technology could change the world does not mean any one of today’s cryptocurrencies will make you rich during the timespan. As such, you must be careful how you choose to bet on forward-thinking trends.

In prior pieces, I praised Block as one of my favorite ways to bet on blockchain technology. While Block may be many years away from proving itself as more of a blockchain-centric tech firm than a payments platform, I do think the caliber of management is more than worth betting on, especially with valuations at multi-year lows.

Even if Dorsey is too early to the blockchain party, Block has a solid ecosystem of payment offerings that can help the firm pay the bills for its incredibly forward-thinking endeavors.

Square Payments and Cash App remain Block’s two present-day growth drivers. Each platform has an impressive user network that Block will easily be able to upsell to as new features and services come to be. Cash App is more than just a payment app to transfer cash to your friends. It’s become a place to buy and sell bitcoin. In due time, Cash App may evolve to become the force that helps Block pressure the big banks.

Ultimately, I view Block as a fintech that could evolve to become more of a neobank in time. As Block continues investing in blockchain projects, there’s also a chance the firm creates the future infrastructure necessary for cryptocurrencies to become more than just a volatile asset to speculate on.

What is SQ Stock’s Price Target?

Wall Street remains a fan of Block, with a “Strong Buy” rating, 26 Buys, five Holds, and one Sell. The average Block price forecast of $112.69 implies about 62% upside potential.

PayPal (PYPL)

PayPal is another fintech firm that’s suffered quite a vicious valuation reset. The digital payment pioneer is looking to expand its presence in digital commerce. With a recession up ahead, payments could be in for a bit of a spill. Regardless, PayPal is a firm that’s more than capable of adapting to the times, even as the digital payments scene gets more crowded.

Following PayPal’s horrid crash, it seems like many investors are discounting the firm’s strong network effects. Though PayPal users will cut back on spending over the next 12-18 months, such users will probably be sticking around. When the tides turn and spending booms again, PayPal will be in a spot to see its payment volumes surge again.

Looking ahead, I’d look for PayPal to be more acquisitive. Whether that means acquiring a social-media firm to lay out the foundation for a social-commerce expansion or taking advantage of smaller tuck-in deals on the latest dip in the fintech scene, PayPal has a lot of ways to flex its “network effect” muscle.

In a prior piece, I praised PayPal’s prior acquisition of Honey as a tool that helped PayPal differentiate itself. The Honey service added value for users by helping them easily find digital coupons to save money on digital purchases. By giving a large user base the tools to save money, PayPal can continue growing the digital payments space.

It won’t be easy to stay competitive, but I would look for PayPal to pursue M&A to further build upon its moat while tech multiples are low.

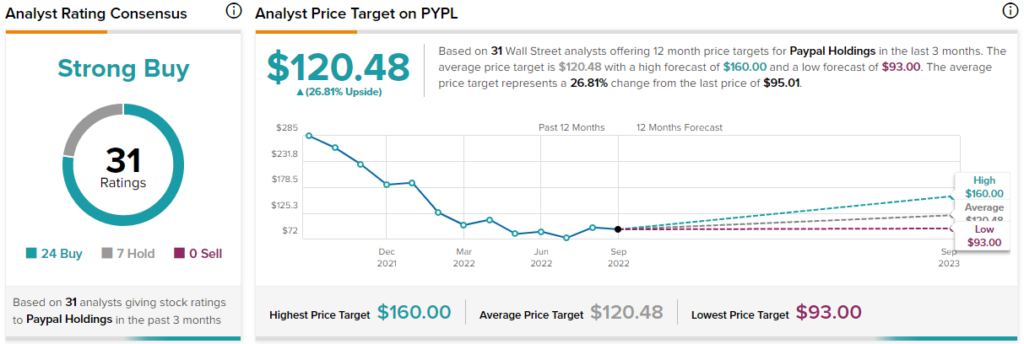

What is PayPal Stock’s Price Target?

Wall Street loves PayPal stock, with a “Strong Buy” rating, 24 Buys, and seven Holds. The average PayPal stock price prediction of $120.48 implies about 26.8% upside potential.

Conclusion: PYPL and SQ Both Look Oversold

Fintech is a tough place to be in right now, as consumers look to cut spending while investors become less willing to pay up for forward-thinking growth stories. Regardless, each fintech giant seems oversold, with Wall Street analysts continuing to stand by each name with “Strong Buy” ratings.