We’re more than 6 weeks into 2022, and the market uncertainty that characterized January has, if anything, deepened. The sharp drops have turned instead to higher volatility, giving a chart of February’s trading a sawtooth look.

The volatility comes as a series of headwinds continue to impact trading sentiment. Stealing the headlines is the Russia-Ukraine situation. Foreign policy pundits are openly speculating on the prospect of war, in the event that Russia invades its neighbor and the US objects. For now, that situation is fluid and unpredictable.

On the domestic front, inflation is high and rising, while the jobs market shows the contradictory indicators of low unemployment and record-high job openings. The Federal Reserve is gearing up to start increasing interest rates in March, but that raises its own questions: Will the rate hikes curb inflation? Will they push into recession?

It’s all enough to give an investor a headache – and an incentive to move strongly into dividend stocks. These are the classic defensive plays, giving investors a dual path toward returns, from both the share appreciation and the dividend payments.

But which ones to buy? Enter George Soros.

His name has become something a lightning rod for controversy in recent years – but the man behind the name is one of the investing world’s true legends. He started his hedge fund, the Quantum Fund, back in 1973, and for the next three decades his average annualized returns exceeded 30%. This made him one of the most successful hedge managers around – and one of the richest men in the world.

With this in mind, we’ve opened up the TipRanks database to get the scoop on two of Soros’s recent new positions. These are Buy-rated stocks – and perhaps more interestingly, both are strong dividend payers. We can turn to the Wall Street analysts to find out what else might have brought these stocks to Soros’ attention.

Kimbell Royalty Partners (KRP)

The first of Soros’ new positions is Kimbell Royalty Partners, a company that works in both energy and real estate. Kimbell is a major landowner in proven hydrocarbon basins across the US, and the company makes its money on royalties from mineral (read – oil and gas) extraction from its properties. Those properties are extensive – Kimbell holds title to more than 13 million acres in some of the highest-yield production basins in the lower 48 states, including the Appalachian gas fields, the Bakken shale oil region, and the Permian Basin of Texas. One key statistic tells just how well-focused Kimbell’s holdings are: approximately 96% of all the onshore rigs in the continental US are in counties where Kimbell has land holdings.

Kimbell has a history of moving to expand its footprint, and in December the company announced completion of a major property purchase. The seller and total acres were not disclosed, but Kimbell did produce, on average by the end of November 2021, some 700 barrels of oil equivalent daily. This is approximately 5% of the total output on Kimbell’s existing holdings.

The company will be reporting its 4Q21 results later this month, but has already declared and paid the Q4 dividend. The payment, of 37 cents per common share, was flat from 3Q21, and up significantly from the 19 cents per share paid out in the year-ago quarter. In fact, the current 37-cent dividend is the highest payment since the January 2020 declaration, and gives a strong yield of 9%. The company is using the dividend to pay approximately 75% of distributable cash back to shareholders.

It’s clear that Soros liked what he saw in KRP – his private family fund bought 150,000 shares in the company in Q4. At the current valuation, this is worth $2.239 million.

Soros isn’t the only one bullish on this stock. Raymond James’ 5-star analyst John Freeman sees Kimbell as one of the energy industry’s best-positioned land holders.

“Kimbell sports an industry-low average yearly decline rate (~12%), a 2022E distribution yield of ~12% and a diverse asset base with exposure to all major resource plays. Additionally, as Kimbell continues to decrease leverage, management intends to proportionally lower forward hedged volumes, giving the company increased exposure to our bullish commodity forecast, all while distributing tax-free distributions,” Freeman noted.

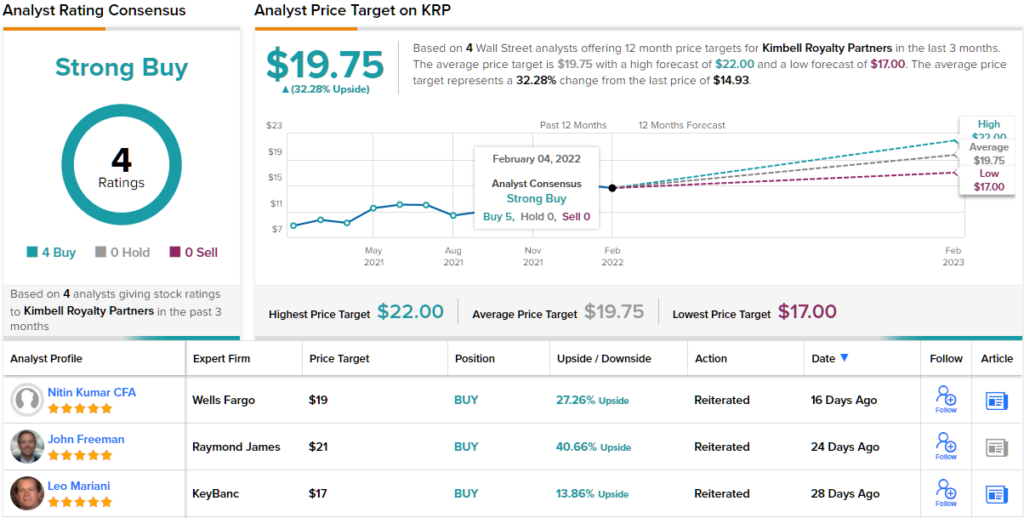

To this end, Freeman puts a Strong Buy rating on this stock, along with a $21 price target that suggests ~41% one-year upside potential. (To watch Freeman’s track record, click here)

The Wall Street view here is both in agreement with Freeman, and unanimous. All 4 of the recent share reviews are positive, for a Strong Buy consensus rating. With a $14.83 trading price and an average target of $19.75, Kimbell boasts an upside of ~32% for the next 12 months. (See KRP stock analysis on TipRanks)

BP PLC (BP)

The next stock on our list of Soros picks is BP, originally British Petroleum, one of the world’s ‘supermajor’ oil and gas companies. BP is a $107 billion behemoth, with operations in traditional crude oil and natural gas exploration and production, the petrochemical industry, and the solar and hydrogen renewable energy segments.

As a gross measure of success, BP saw $157 billion in total revenues last year. That number included the $50.6 billion in Q4, the highest quarterly total since 1Q20. A combination of rising oil prices and increased economic activity as the pandemic begins to fade improved the company’s top line.

The bottom line, also, has improved in recent quarters. The earnings per American Depositary Share reached $1.23 in Q4, for the fourth consecutive quarter of sequential gains – and a huge turnaround from the mere 3 cents reported in in the year-ago period.

The strong earnings have supported a steady dividend. While BP was forced to cut back on the payment during the worst of the pandemic crisis last year, the company still pays out 32 cents per share, which annualizes to $1.28 for a 4% yield. The yield is about double the average found among companies listed in the S&P 500.

As for Soros, he picked up 300,000 shares in this stock during Q4, a clear vote of confidence. Soro’s holding is currently worth $9.68 million.

Soros isn’t the only one giving this oil and gas stock some love. Wall Street analyst Stephen Richardson, writing from Evercore, describes the company as ‘a plan that is coming together.’ He writes: “The acceleration of both shareholder returns and the timeline on achieving a host of targets particularly across lower-carbon businesses was notable… This sets up an interesting near-term dynamic where cash returns to shareholders continue to step up while the transformation accelerates and ultimately comes forward in what is a long time-frame event.”

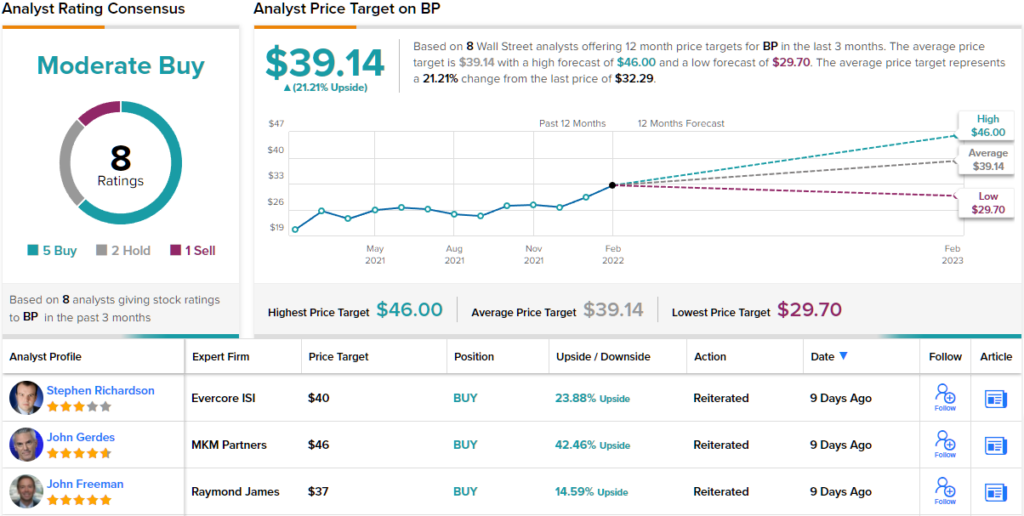

Acknowledging the strength of the company’s forward plans, Richardson rates BP shares an Outperform (i.e. Buy), and his $40 price target suggests an upside of 23% for the year ahead. (To watch Richardson’s track record, click here)

What does the rest of the Street think? As it turns out, 5 out of 8 analysts that have published a recent review see the stock as a Buy, making the consensus rating a Moderate Buy. Shares are selling for $32.29 and have an average price target of $39.14, suggesting a 21% upside by the end of this year. (See BP stock analysis on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.