Keeping up the returns would be a neat trick in today’s market, as the main indexes are all steeply down for the year so far – with losses of 15% on the S&P 500 and 24% on the NASDAQ. For investors, then, the best strategy may just be to follow a winner.

Billionaire investing legend George Soros is most definitely a winner. He’s built a portfolio worth billions, and had possibly the greatest bull run in hedge fund history, averaging 30% annualized returns for 30 years. Starting in 1992, when he shorted the Pound Sterling and made $1 billion in 24 hours, to his most recent 13F filings, Soros has a record of success that few investors can match.

Today, Soros remains the chair of Soros Fund Management and is thought to be worth over $8 billion, a figure which would have been far greater but for the billionaire’s extensive philanthropic work.

So, when Soros takes out new positions for his stock portfolio, it is only natural for investors to sit up and take notice. With this in mind, we decided to take a look at three stocks his fund has recently loaded up on. Soros is not the only one showing confidence in these names; according to the TipRanks database, Wall Street’s analysts rate all three as Strong Buys and see plenty of upside on the horizon too.

Stem, Inc. (STEM)

First up is Stem, a tech company that specializes in using artificial intelligence (AI) to create ‘smart’ storage systems for clean energy. In other words, that company is designing thinking batteries that are optimized for use with renewable energy production schemes. Energy storage is a major bottleneck when it comes to renewables; as we all know, you cannot power the grid with wind or solar if the breezes die down or night falls. Smart batteries will let producers squeeze higher efficiencies from optimal generation times.

The company’s main product is the Athena software platform, that uses a combination of AI and machine learning to optimize the switches between grid power, on-site generated power, and battery power. The customer base includes public utilities, major corporations, and various project developers and installers. Stem estimates that its total addressable market will increase 25x by the year 2050, to reach $1.2 trillion.

So Stem is getting in at the beginning of what may be a boom. And the company’s revenue growth would suggest that the ‘boom potential’ is real. The top line grew 166% from 1Q21 to 1Q22, rising from $15.4 million to $41.1 million in one year, and coming in 29% above the high end of the previously published guidance. The company’s quarterly bookings almost tripled, from $51 million one year ago to $151 million in 1Q22. And, despite running quarterly net losses, Stem finished the first quarter this year with a usable balance of $352 million in cash and liquid assets.

All of this caught the attention of George Soros, who’s bought up 300,000 shares of Stem in Q1. These shares are worth $2.25 million at current prices.

Guggenheim analyst Joseph Osha, rated 5-stars at TipRanks, is also bullish here. He notes that the company’s Q1 results beat his expectations, and then adds, “STEM still faces a multi-year period during which much of the company’s revenue is likely to consist of low-margin storage hardware sales, but our confidence is growing that the company should be able to earn good returns by managing and dispatching storage assets. At this point, the company’s full-year targets appear reasonable, in our view, and in fact the annualized recurring revenue target of $60–80 million by yearend looks conservative to us.”

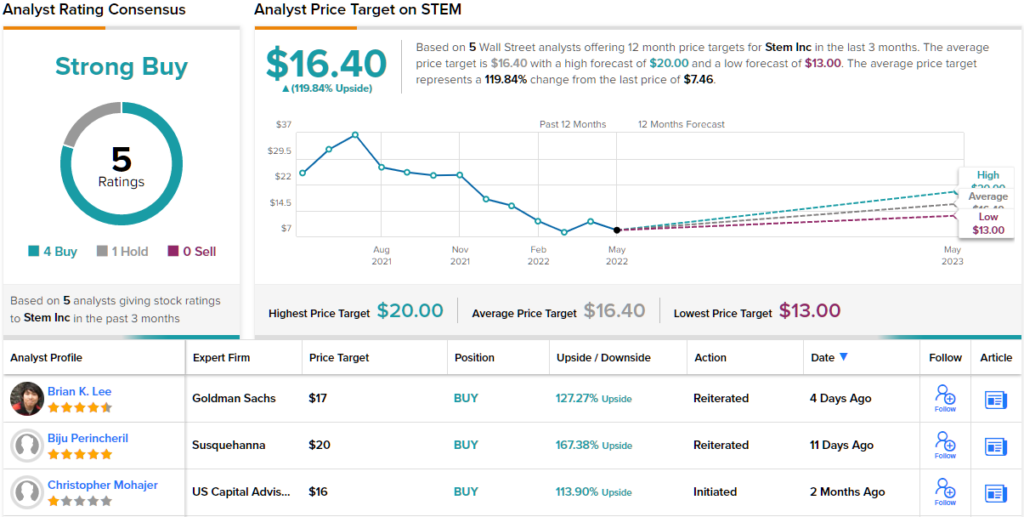

These comments back up Osha’s Buy rating on STEM stock, while his $16 price target indicates room for ~115% upside in the next 12 months. (To watch Osha’s track record, click here)

For the most part, Wall Street’s analysts agree that this is a stock to buy. Stem shares have 5 recent analyst reviews, including 4 Buys over 1 Hold, for a Strong Buy consensus rating. The stock is selling for $7.49 and its $16.40 average price target suggests its has ~120% upside ahead of it. (See STEM stock forecast on TipRanks)

Webster Financial (WBS)

The next Soros pick is Webster Financial. This is a holding company, the parent of Webster Bank. This Connecticut-based banking firm has approximately $65 billion in assets and offers a range of services, including consumer and commercial banking, personal and business loans, and wealth management. Webster has a commitment to growth, and in February of this year it completed its merger with Sterling Bancorp. With that transaction complete, Webster now has $44 billion in loans, $53 billion in deposits, and a network of 202 branches in the Northeast.

Webster’s first quarter of 2022 showed a net interest income of $394 million, up 76% year-over-year. The company’s interest-generating assets showed substantial growth over the past year, increasing from $19.2 billion to $50.3 billion, a gain of 61%. Webster increased its loans and leases outstanding by 67%, from$14.4 billion to $35.9 billion, and saw its average deposits increase from $17.6 billion to $45.9 billion, or 62%.

These gains in income and income generation supported Webster’s continued payment of its dividend, which was declared in April at 40 cents per common share. With an annualized rate of $1.60 per share, the dividend currently yields 3.45%.

Turning to Soros’ activity here, the billionaire purchased 42,100 shares of WBS stock in Q1, which are now worth a total of $2.02 million.

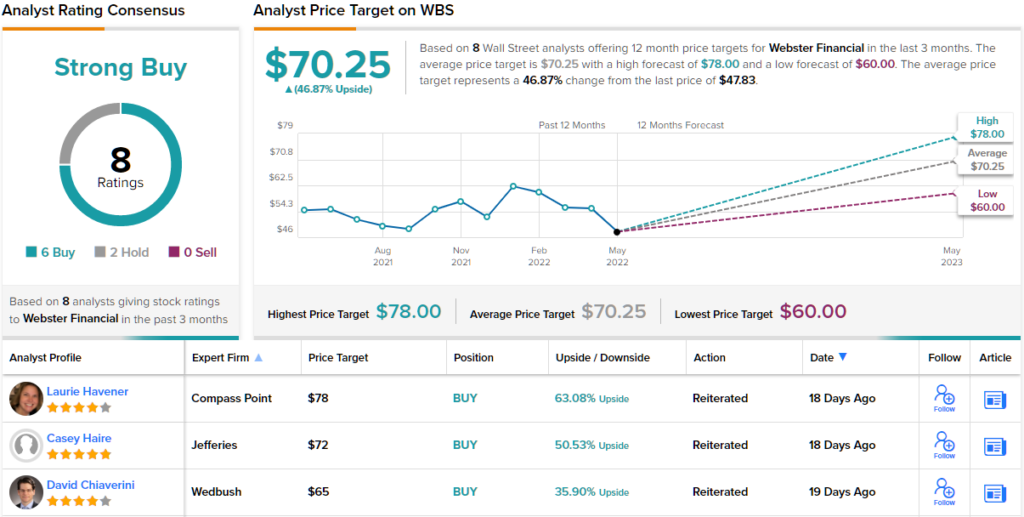

Soros isn’t the only one giving this stock some love. 5-star analyst William Wallace, of Raymond James, puts a Strong Buy rating here, and a $73 target price that suggests ~52% upside in the year ahead. (To watch Wallace’s track record, click here)

Backing his bullish stance, Wallace writes: “All in, our thesis remains unchanged, where we believe cost and growth targets from the Sterling deal are attainable, and the financial merits of the deal continue to be mispriced, leaving room for upside. That said, as progress is shown towards deal targets, which look increasingly reasonable, we believe shares should recover their discount and ultimately trade at a premium relative to its mid-cap peer group valuation comparison.”

Overall, of the 8 recent analyst reviews published for WBS, 6 are Buys and 2 are Holds, backing a Strong Buy rating. The stock has an average price target of $70.25, implying ~47% upside from the share price of $47.81. (See WBS stock forecast on TipRanks)

Synovus Financial Corporation (SNV)

Let’s wrap up with Synovus, another denizen of the financial world. This financial services company, based in Columbus, Georgia, commands some $56 billion in assets and has 272 branches across the Southeast, in Tennessee, South Carolina, Georgia, Alabama, and Florida. This is a high-growth region, known as one of the country’s economic drivers. Florida is the country’s third-largest state, and Tennessee, with no state income tax, hits above its weight in attracting business growth. This is Synovus’ playing field.

In 1Q22, Synovus reported a year-over-year drop in earnings. Diluted EPS fell from $1.19 in the year-ago quarter to $1.11 in the current report. At the same time, the bank increased its loan business in the quarter. Total loans grew from $38.8 billion one year ago to $40.1 billion as of March 31. Total deposits grew a modest 3%, from $47.3 billion to $48.6 billion.

Synovus still felt confident to boost its dividend payment for the first time since the start of 2020. In its March declaration, the company increased the common share dividend from 33 cents to 34 cents. At an annualized payment of $1.36, this gives a yield of 3.5%.

Soros liked what he saw here, and in the last quarter he bought 40,800 shares. At current prices, these are now worth $1.65 million.

The controversial billionaire wasn’t the only bull on Synovus. In coverage for Wells Fargo, analyst Jared Shaw writes, “The effects of streamlining the franchise, reducing overall credit risk, expansion into faster growing FL markets, and a head start on digital offerings were materializing throughout 2021, with increased momentum providing a boost year to date. We believe SNV reached an inflection point in 2021, and think the asset sensitivity combined with an upgraded management growth outlook for ’24 will drive shares higher.”

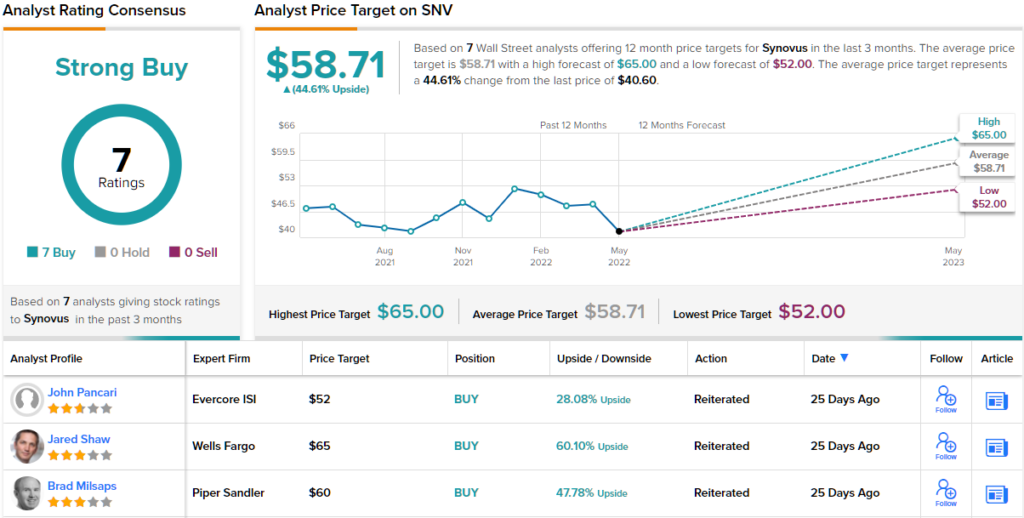

To this end, Shaw gives SNV stock an Overweight (i.e. Buy) rating, and his price target, of $65, indicates potential for 60% appreciation in the next 12 months. (To watch Shaw’s track record, click here)

All in all, this stock gets a unanimous Strong Buy from the Street’s consensus, based on 7 recent analyst reviews. The stock is selling for $40.6 and its $58.71 average price target suggests ~45% upside from that level. (See SNV stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.