Investor sentiment is turning positive, as this month’s significant market gains roll on. The pace of inflation continues to decelerate, easing a major headwind, and the S&P 500 is up almost 17% year-to-date.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Watching the market situation for Goldman Sachs, chief US equity strategist David Kostin notes that the sound third quarter earnings have provided additional support for the index’s recent gains, writing, “S&P 500 3Q earnings results were stronger than expected and represented the first quarter of year/year EPS growth since 3Q 2022. EPS grew by +4% year/year and +10% excluding Energy. Sequential margin expansion represented the bright spot during earnings season, while sales results beat expectations by a smaller magnitude. Corporates reported a continued broad-based slowdown in cash spending.”

But it’s no secret that this year’s market gains have been driven by the tech sector. The tech-heavy NASDAQ has a 34% year-to-date gain. However, those gains have not been evenly distributed. Seven mega-cap tech giants, dubbed the ‘Magnificent Seven,’ have led the way.

However, even among the ‘Magnificent Seven,’ the potential for gains is not evenly spread. According to 5-star analysts at Goldman Sachs, Amazon (NASDAQ:AMZN) and Nvidia (NASDAQ:NVDA) are primed for much larger gains than their peers going forward, and their stories are based on reduced worry in an uncertain time. Here are the latest details on these two tech leaders from the TipRanks databanks, along with comments from the Goldman analysts.

Don’t miss

- Oppenheimer Expects the S&P 500’s Advance to Continue Into 2024 — Here’s Why These 2 Stocks Might Be Worth Buying

- Insiders Load Up on These 2 ‘Strong Buy’ Stocks — Here’s Why You Should Pay Attention

- Morgan Stanley Says China’s Education Industry Looks Appealing Right Now — Here Are 2 Stocks to Bet on It

Amazon

We’ll start with Amazon, a company that started out in the ‘90s as an online bookseller, survived the dot-com bubble-bust, and has since become the world’s largest online retailer. The company built its success on a complete reimagining of the e-commerce promise – giving customers access to an unmatched variety of products and offering home delivery as early as the next day. With a market cap just under $1.5 trillion, Amazon is the world’s fourth-largest publicly traded company.

Growing from its extraordinary scale, Amazon has expanded from online retail into numerous other niches. The company has its hands in everything, from cloud computing to online television streaming, and is making use of AI to improve its service offerings on many of these products. AI has already been integrated into the AWS cloud, and is also used in Amazon’s new software code development tool, its new chatbot, and its image building platform. While these services are revenue generators, the company can afford to pursue them due to the size and scope of its retail successes.

That success brought Amazon solid beats in its recent 3Q23 financial release. The company’s top line came to $143.1 billion, up nearly 13% year-over-year and beating the forecast by over $1.5 billion. Amazon’s year-over-year sales gains included 11% in the North American retail segment, 16% in international retail, and 12% for AWS. At the bottom line, Amazon reported an EPS of 94 cents per diluted share, compared to 28 cents in the prior-year quarter. The 3Q23 EPS came in 35 cents better than had been anticipated.

As a result, Amazon shares are up 66% so far this year, strongly outperforming the broader market.

For Goldman Sachs’ 5-star analyst, Eric Sheridan, this adds up to a long-term growth story. He writes of the stock, “Looking over a multi-year timeframe, we reiterate our view that Amazon will compound a mix of solid revenue trajectory with expanding margins as they deliver yield/returns on multiple year investment cycles. After trading in a range (& underperforming the broader market) for most of the past 2-3 years, we see AMZN as well positioned for future outperformance as eCommerce margins continue a trajectory of scaling over headwinds created in recent years, as its advertising business continues to achieve scale and as AWS can still benefit from a long-tailed structural growth opportunity in the shifting needs of enterprise customers (while producing a balance of growth and margins).”

Looking ahead, Sheridan sees Amazon as a sound investment by any measure: “In summary, we continue to see Amazon positioned as a leader in all aspects of secular growth within our Internet coverage (eCommerce, digital advertising, media consumption, aggregated subscription offerings & cloud computing).”

The analyst goes on to rate Amazon shares as a Buy, and he sets a $190 price target to point toward a one-year gain of 29%. (To watch Sheridan’s track record, click here)

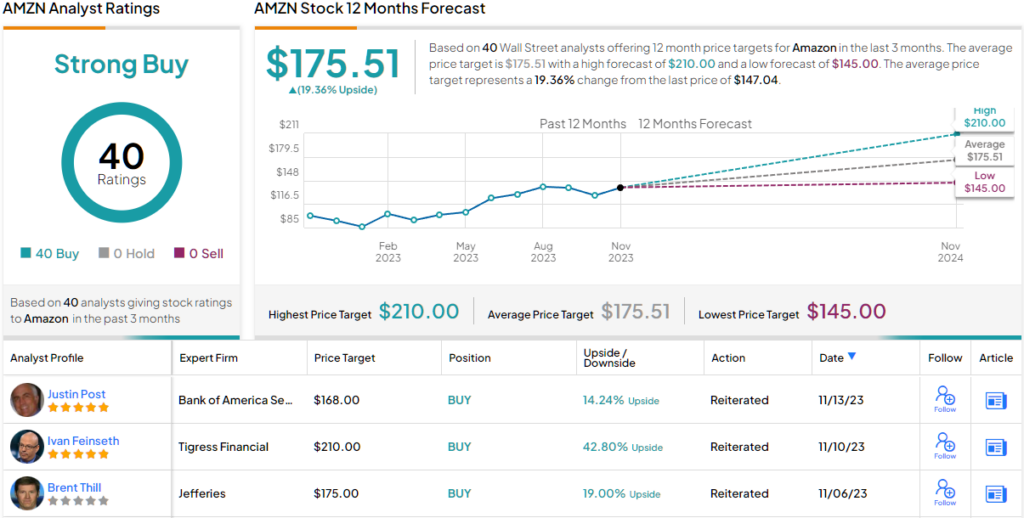

The tech giants have no problem gathering plenty of analyst reviews – and Amazon has 40, all positive, for a unanimous Strong Buy consensus rating. Amazon shares are trading for $146.81, and their $175.51 average price target implies an upside of 19% in the coming year. (See Amazon stock forecast)

Nvidia Corporation

The next tech giant we’ll look at is Nvidia, a leader in the essential semiconductor chip industry. Nvidia is another of the market’s multi-trillion-dollar companies, with a market cap of $1.2 trillion and huge – and growing – demand for its high-end, AI-capable GPU chips. Nvidia originally developed these chips for the online gaming niche, but the high processing capacity of the company’s GPUs made them eminently suitable for professional graphic design use as well as later for data center and AI applications.

Nvidia got a major boost one year ago when its customer OpenAI launched the generative AI chatbot, ChatGPT. That powered a sudden boom in the AI industry, with a consequent burst of demand for Nvidia’s products. Nvidia received some additional welcome support earlier this year when OpenAI announced that it will need up to 10,000 new GPUs by next summer, just to maintain ChatGPT’s performance levels.

While AI gets the headlines, Nvidia’s largest business comes from its data center segment. In the last reported quarter, fiscal 2Q24, Nvidia brought in more than $10 billion in data center revenue, the bulk of the company’s $13.5 billion quarterly top line. That total was more than $2.4 billion above the forecast, while Nvidia’s earnings, at $2.70 per share in non-GAAP measures, came in 61 cents ahead.

Nvidia will release its fiscal 3Q24 numbers next week, and the Street is expecting to see $15.99 billion in revenue with a non-GAAP EPS of $3.37.

Powerful demand is the key here, for Goldman analyst Toshiya Hari. The 5-star stock pro writes of Nvidia’s shares, “Look for NVDA to maintain its status as the accelerated computing industry standard for the foreseeable future given its competitive moat and the urgency with which customers are developing and deploying increasingly complex AI models. And a strong and broadening demand profile in the Data Center, plus an improving supply backdrop should support sustained revenue growth through CY2024.”

Quantifying his stance, Hari gives NVDA shares a Buy rating. He has set his price target at $605, which implies a 23% upside for the next 12 months. (To watch Hari’s track record, click here)

All in all, Nvidia has picked up 38 recent analyst reviews, and these have a lopsided split of 37 to 1 in favor of the Buys over Holds. The shares are currently selling for $491.41, and their $647.32 average price target suggests an increase of ~32% on the one-year horizon. (See Nvidia stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.