Altria Group (NYSE: MO), the all-weather $81.7 billion consumer staples giant, appears well-positioned to keep flourishing in the current market environment. With its most recent dividend increase from last week marking 53 years of consecutive annual dividend hikes, investor confidence in the stock should remain very strong, moving forward.

Nonetheless, I am neutral on the stock.

Altria Stock’s Advantages in the Current Environment

As the ongoing macroeconomic unrest persists, equities continue to suffer significantly. In light of interest rate hikes, geopolitical turmoil, and a hard-to-predict future, investors have become increasingly keen on securities that offer lowered risk, softer volatility, and easier-to-foresee total return prospects as we advance in this treacherous environment.

The truth is that the economy has become increasingly interconnected over the past few decades. Additionally, with ETFs ruling the investing world, the way securities trade has become increasingly correlated.

However, I believe Altria stock is one of the very few well-known securities that totally differentiates itself in the current market environment. This is primarily due to two reasons.

Firstly, due to Altria’s revenues coming in predominantly from its cigarette business, the company’s cash flows are not being impacted during the current market setting. Cigarettes are among the most inelastic products, which implies that Altria can keep raising its prices during the ongoing highly inflationary environment while suffering no losses from declined sales volumes.

Secondly, Altria has quite a low ESG score. This is due to tobacco products being harmful. The effect of this factor, nevertheless, is that the stock is not included in a myriad of ETFs, mutual funds, and closed-end funds, as most such investment vehicles have at least some sort of ESG-related filters in place.

Institutions, in general, certainly avoid such stocks (i.e., tobacco, war, and vice-related stocks). Therefore, Altria’s trading patterns are mostly uncorrelated with the overall fluctuations over the general markets.

Robust Q2-2022 Results Despite Industry Concerns

Apart from the concerns linked to the ongoing market environment, investors have also been also mindful of tobacco stocks and their long-term sales prospects. Yet, Altria’s Q2 results once again demonstrated the resiliency attached to its business model.

Revenues net of excise taxes came in at $5.37 billion, just 4.3% lower year-over-year. However, we have to note that while the decline in revenues was partly due to lower net revenues in the smokeable products and oral tobacco segments, the larger factor was the sale of the company’s wine business last year. Besides the impact of the sale of the wine division, the core business remained mostly stable.

To reiterate the earlier point about cigarettes being an inelastic product, net revenues in Altria’s smokeable products segment fell by 2.9% year-over-year despite cigarette shipment volumes declining by 11.1%. This is because the company has fantastic leverage in terms of raising prices by an almost equally-high percentage.

What’s quite more important than revenues in the case of Altria, however, is its ability to deliver growing profits. We know revenues are going to be weak moving forward, so profits are the most meaningful element when assessing Altria.

Even though Altria’s top-line performance was soft, Altria was able to generate strong profits. Altria’s adjusted diluted EPS increased by 2.4% to $1.26, mainly powered by a lower share count, higher operating companies’ income (OCI), and lower interest expenses.

Amid Altria’s performance remaining on track with the underlying targets, management reiterated its full-year 2022 outlook, anticipating adjusted diluted EPS to be in the range of $4.79 to $4.93.

This suggests a growth rate of 4% to 7% compared to Fiscal 2021. Thus, Altria’s profitability potential stays in exceptional form. This is truly paramount for the company to preserve and grow its hefty capital returns, which appear to be the one favorable catalyst left in bulls’ weapon cache.

Capital Returns Trend Higher

As mentioned, the biggest catalyst that attracts investor interest in Altria’s investment case is its hefty capital returns. Management knows this. Thus, raising capital returns remains a top priority. Indeed, around a week ago, Altria announced a 4.4% increase in its quarterly dividend to a rate of $0.94.

This marked the company’s 53rd successive annual dividend boost, which makes for an incredible track record that illustrates the qualities of its business. By employing the midpoint of management’s guidance and the stock’s present annual dividend per share rate of $3.76, the stock’s payout ratio should stand at around 77.3%. This indicates a rather comfy coverage ratio when it comes to its massive 8.3% yield.

As noted, the growth in adjusted EPS was aided by a lower share count. Buybacks are a central component of Altria’s total capital returns to shareholders. Altria kept repurchasing shares in bulk, allocating over $2.11 billion in that area over the past twelve months.

In Q2 alone, Altria repurchased $507 million worth of stock, pointing to an accelerating pace of buybacks. It’s reasonable, considering the humble stock price levels. The steadily-falling share count should keep adding to earnings-per-share growth as we advance and even “save” the company from paying extra dividends on aggregate.

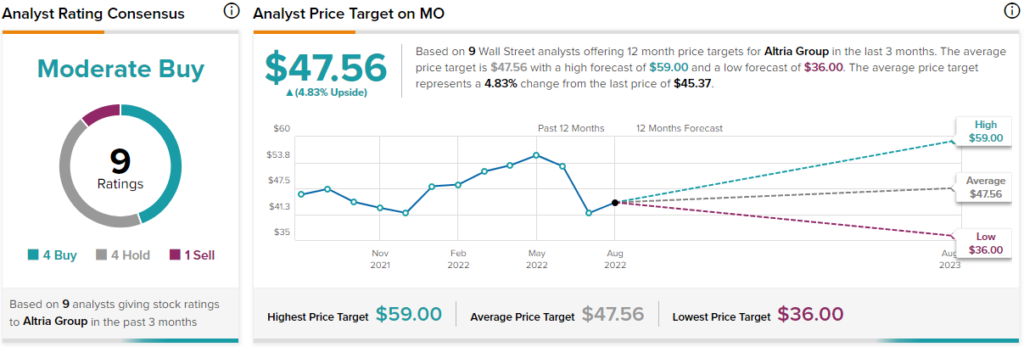

What is the Price Target for Altria?

Turning to Wall Street, Altria Group has a Moderate Buy consensus rating based on four Buys, four Holds, and one Sell assigned in the past three months. At $47.56, the average Altria Group price prediction suggests 4.8% upside potential.

Conclusion: Too Cheap & Fruitful to Ignore

Not all types of investors are interested in Altria, and that’s understandable. However, Altria’s profitability is still robust, management’s Fiscal 2022 is bright, and dividends/buybacks continue to rise. By combining Altria’s powerful yield and low valuation (9.3x P/E ratio at the midpoint of management’s guidance), the stock offers sizeable return potential and a wide margin of safety.