Once the closing bell rings on Tuesday’s trading action, Netflix (NFLX) will take its turn to report 2Q22 earnings.

The latest financial statement comes at a time of change for the streaming giant as it has decided to add an ad-supported tier for the first time in its history – a measure intended to fix growth issues. Investors will also be hoping there will be no repeat of Q1’s abject performance, which represented the first time Netflix lost subs in a decade.

Netflix, however, has warned the second quarter is unlikely to bring much cheer and said it expects to lose another 2 million subs in Q2.

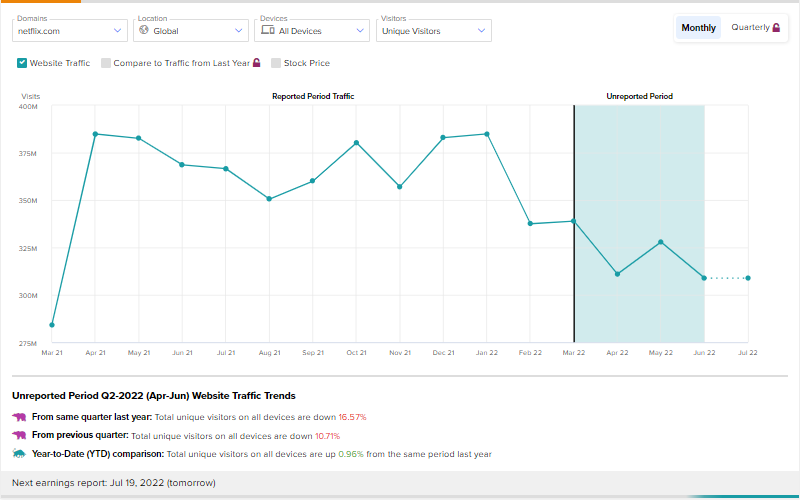

Notably, Netflix’s website visits are not encouraging right now. According to the TipRanks Website Traffic tool, total unique visitors on all devices were down ~17% year-over-year in Q2.

However, heading into the print, Wedbush’s Michael Pachter is optimistic the company can beat its targets.

“We think that Netflix is positioned to exceed its guidance for Q2, particularly because of the staggered release date for Stranger Things 4, which has very strong viewership,” the analyst explained. “While it is possible that the company will once again issue downbeat guidance for Q3, we think that the staggered release dates limited churn at quarter end and once again, Netflix is likely positioned to grow.”

Addressing the company’s plans, Pachter does do not anticipate significant changes to happen overnight; rather, the analyst thinks Netflix will “gradually” raise its fees and introduce its ad-supported tier.

That said, the analyst believes the sooner the company demonstrates its dedication to lowering churn by staggering the release of its new content over several weeks, investors will see an increase in net new subscribers and “investor confidence in the Netflix business model will be restored.”

As for the numbers, Pachter expects Netflix will lose 1.50 million subs – better than the loss of 2.00 million in the guide. The analyst expects Q2 revenue of $8,137 million vs. the Street at $8,046 million and guidance of $8,053 million. For the bottom-line, Pachter is calling for EPS of $3.05 compared to the consensus estimate of $2.95 and guidance of $3.00.

While Pachter does not think Netflix’s share price will “approach 2021 levels for many years,” the analyst believes that over the next 12 months his $280 price target is “achievable.” The figure anticipates shares will climb 48% higher over the period. Pachter’s rating stays an Outperform (i.e., Buy). (To watch Pachter’s track record, click here)

Overall, the Street’s take offers an interesting paradox; the stock currently boasts a Hold consensus rating, based on 24 Holds, 10 Buys, and 6 Sells. However, at $253.52, the average target suggests shares will rise ~28% in the year ahead. (See Netflix stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.