Considering its status as what you might call a “recovery play,” Airbnb (ABNB) stock has not had a very successful 2021 so far. The shares are sitting 4% into the red, and much like a hard-working bod anticipating a holiday, are waiting for lift off.

That said, RBC Capital’s Brad Erickson thinks there are “multiple secular tailwinds” which should help push the company – and shares – forward.

“Airbnb is the clear leader in private/alternative accommodations while addressing an $800B+ market that we think expands to over $1.1T over time,” the 5-star analyst said. “In particular, we like ABNB’s dominant customer engagement, view it as more than just a re-opening trade with less appreciated secular tailwinds, our property manager checks suggest share gains are on the horizon and we think supply maturity is further away than investors realize.”

At the core of Erickson’s investment thesis is ABNB’s “dominant engagement with its user base” which allows for two very important features which set it apart from the competition.

For one, it significantly lowers Google traffic risk, which basically guarantees “industry-leading long-term margins.” Secondly, it sets the scene for TAM (total addressable market) expansion via the addition of “other travel modalities, long-term stays, co-working and/or student housing.” This can then be further boosted by “other value-added services” such as financial services, different kinds of loyalty partnerships and, importantly, advertising.

Erickson also thinks the company is almost certain to benefit from the pandemic-driven “incremental savings” of households across the globe. This extra “dry powder” will be used for booking trips. Furthermore, the move to remote working could provide an additional tailwind, and expand the TAM further, as employees won’t necessarily be tied permanently to just one location.

The analyst’s channel checks also indicate that May and June bookings are likely “tracking well ahead of expectations.” Lastly, Erickson anticipates the market share gains made by rival VRBO over the past few months, due to “favorable customer demographics and geographic exposure,” will eventually “normalize,” or even swing back in ABNB’s favor.

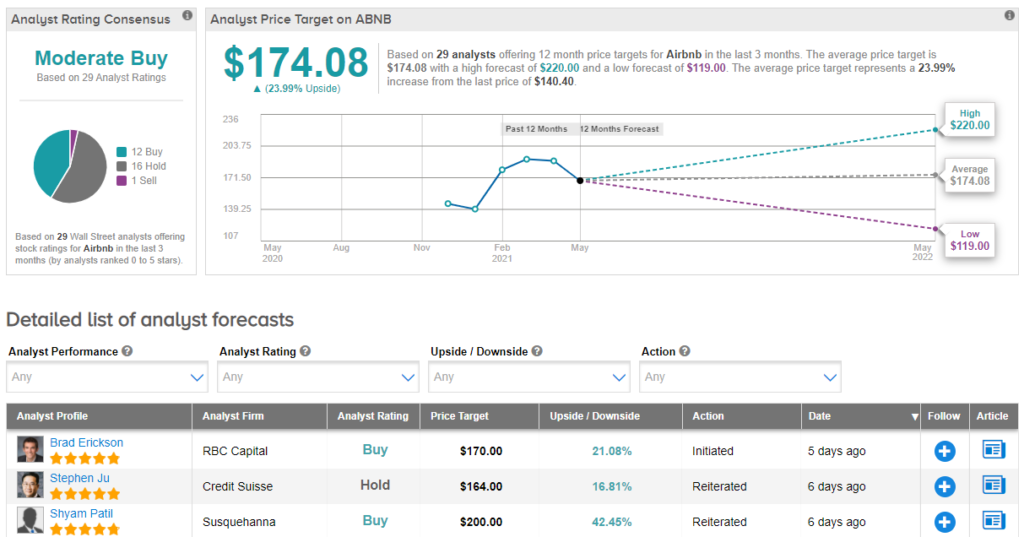

So, good news for Airbnb, but what does it all mean for investors? Erickson initiated coverage with an Outperform (i.e., Buy) rating and $170 price target, suggesting 12-month upside of 21%. (To watch Erickson’s track record, click here)

The rest of the Street has mixed opinions when considering ABNB’s prospects. Based on 12 Buys, 16 Holds and 1 Sell, the stock has a Moderate Buy consensus rating. Overall, the bulls are in control, as the average price target currently stands at $174.08, implying shares will appreciate by 24% in the year ahead. (See Airbnb stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.