Data on cooling inflation has revived investors’ hopes about better days ahead. Nonetheless, macro uncertainty continues to make it difficult to pick the right stocks. Given this scenario, looking at some large-cap stocks trading at attractive levels could be helpful. Large-cap stocks have a market capitalization of more than $10 billion and are generally associated with well-established, stable companies. We used TipRanks’ Stock Comparison Tool to place Starbucks (NASDAQ:SBUX), MercadoLibre (NASDAQ:MELI), and CrowdStrike (NASDAQ:CRWD) against each other to pick the most attractive large-cap stock.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Starbucks (NASDAQ:SBUX)

Leading coffee chain Starbucks reported better-than-anticipated results for the second quarter of Fiscal 2023 (ended April 2, 2023), thanks to strong momentum in North America and recovery in the company’s business in China. However, investors were disappointed as the company maintained its previously issued full-year guidance and did not raise it.

Starbucks shares have advanced only about 2% year-to-date due to persistent macro challenges, China’s sluggish recovery following Q2 FY23 results, and conflict with the baristas’ union.

In late June, BTIG analyst Peter Saleh lowered his EPS estimates for Starbucks to reflect a slower-than-anticipated recovery in China over recent months. However, the analyst believes that a complete recovery in the company’s business in China could meaningfully boost earnings over the medium and long term.

Additionally, Saleh thinks that investors are likely not fully appreciating Starbucks’ shift to drive-thru locations in the U.S., which could drive operating margins above pre-COVID levels. The analyst pointed out that drive-thrus now account for 70% of Starbucks’ U.S. store base, up from 60% in Q4 FY20 and 40% in 2015. He highlighted that the drive-thru locations generally generate higher volumes and margins. Saleh maintained a Buy rating on SBUX with a price target of $125.

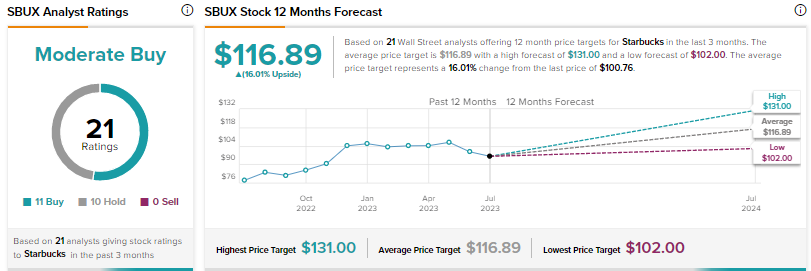

Is Starbucks Stock a Buy, Sell, or Hold?

Wall Street’s Moderate Buy consensus rating on Starbucks is based on 11 Buys and 10 Holds. The average price target of $116.89 implies 16% upside potential.

MercadoLibre (NASDAQ:MELI)

Shares of MercadoLibre, the leading e-commerce and fintech player in Latin America, have risen 43% so far in 2023, thanks to its solid performance in recent quarters despite a tough macro backdrop. In the first quarter, MercadoLibre’s Q1 revenue increased 35% to $3 billion. Further, EPS surged 205% to $3.97. The company gained from the collapse of Brazilian retailer Americanas SA.

Last week, Bank of America analyst Robert Ford downgraded MercadoLibre stock to Hold from Buy and lowered the price target to $1,350 from $1,680. Ford believes that the new cross-border tax rules, which exempt direct-to-consumer e-commerce purchases of up to $50 from a 60% import tariff and impose a 17% value-added tax, would encourage new entrants and adversely impact MercadoLibre.

In contrast, Hedgeye analyst Brian McGough added MELI to his long idea list in early July. The analyst believes that MELI could benefit from the bankruptcy of its Brazilian e-commerce competitor Americanas and win market share in a “strong secular growth category” like e-commerce.

McGough sees “a positive macro inflection in MELI’s core markets that are supportive of strength in consumer spending and consumer equities.”

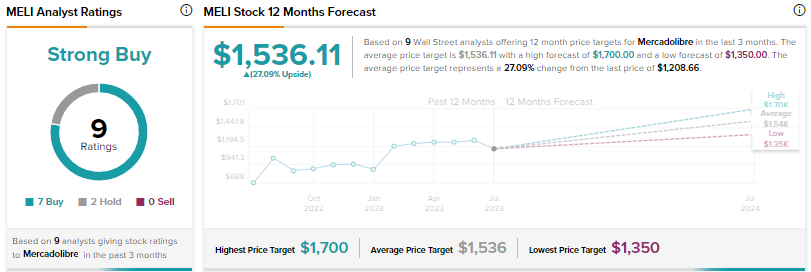

What is the Target Price for MELI?

Wall Street’s Strong Buy consensus rating on MercadoLibre is backed by seven Buys and two Holds. The average price target of $1,536.11 implies 27.1% upside.

CrowdStrike (NASDAQ:CRWD)

Cybersecurity provider CrowdStrike specializes in endpoint security. It reported upbeat fiscal first-quarter (ended April 30) results, with adjusted EPS surging 84% to $0.57, driven by 42% growth in revenue and higher gross margin.

CrowdStrike continues to witness increased adoption of its offerings. At the end of Q1 FY24, CrowdStrike’s module adoption rates were 62%, 40%, and 23% for five or more, six or more, and seven or more modules, respectively.

Despite an improved full-year outlook, there are concerns about the continued slowdown in the company’s revenue growth. The company expects its fiscal second-quarter revenue growth in the range of 34% to 36%. This guidance indicates a continued deceleration in the top-line growth, as enterprises are being cautious about their IT spending due to macro headwinds. That said, the spending on cybersecurity has been resilient compared to other IT areas due to the growing risk of cyber attacks.

Looking ahead, CrowdStrike sees tremendous opportunities created by generative artificial intelligence (AI) applications. In May, the company unveiled its Charlotte AI offering to deliver generative AI-powered cybersecurity.

Following an investor call with CrowdStrike President Mike Sentonas last week, Needham analyst Alex Henderson said that he expects Charlotte AI to increase the adoption of CrowdStrike’s modules and maximize customers’ return on investment (ROI).

Based on the discussions during the call, the analyst gathered that the initial feedback from top enterprise customers using the pilot Charlotte offering has been strong. The company is expected to officially roll out Charlotte AI in September at its Fal.Con conference. Henderson reiterated a Buy rating on CRWD with a price target of $170.

Is CRWD a Good Stock to Buy?

Based on 27 Buys and two Holds, CrowdStrike scores a Strong Buy consensus rating. The average price target of $177.18 implies nearly 16% upside potential. Shares have rallied 45% so far in 2023.

Conclusion

Wall Street sees higher upside potential in MercadoLibre than Starbucks and CrowdStrike. MercadoLibre is expected to benefit from further penetration of e-commerce and digital payments in Latin America. Despite the potential unfavorable impact of a new tax ruling in Brazil, the company’s dominant position in Latin America, strategic investments, and strong execution are expected to drive continued growth.