For the past few years, the world’s largest chipmaker, Intel (INTC), has been buckling under pressure from elevated costs, intense competition, and supply shortages and constraints. The company also had hit a plateau with regard to technological innovation and, thus, lost its appeal on the way. Shares of the company have dropped considerably and are currently trading near its 52-week low of $33.6. Nonetheless, Needham analyst Quinn Bolton reiterated his bullish stance on the company recently, stating that it has a bright future.

Interestingly, the productivity lull was broken with the announcement of an investment program in partnership with global asset management firm Brookfield, on August 23. As part of the agreement, both partners will jointly invest $30 billion toward chip production. The investment will hasten the construction of two new wafer fab equipment production sites in Chandler, AZ.

Has Intel Found Its Way Back?

Bolton is upbeat about the financial flexibility that the partnership is expected to bring to Intel. The capital from the program will be below Intel’s cost of equity (CoE) of approximately 8.5% and above its cost of debt (CoD), which is around 4.5%, strengthening the balance sheet. For context, CoE is the returns expected by an investor on an equity investment, and CoD is the effective interest rate that a company pays on a loan. Bolton expects the cost of new capital to be around 6.5%.

Back in February’s Investor Day event, Intel had projected that the support from the U.S. government, private investment, and others would reduce its five-year expected capital expenditures by at least 10%, which might go up to 20-30%. The latest program deal and the government’s CHIPS and Science Act, signed earlier this month, make it all the more likely that the capital expenditure offsetting can hit the higher end of the projection, at least in CY2022. The funding itself will reduce upfront CapEx by about $15 billion.

Moreover, the program is also likely to help Intel achieve cash flow break-even sooner than it would under the traditional model. While boosting the bottom line of the company, this will also ensure the maintenance of cash/debt balance for other investments and continued dividend payments.

Bolton said, “Prior to the call, we believed Intel may have to give up half of its profits once the fabs reached full volume. This is NOT the case and we are more positive on the program as Intel keeps most of the upside.”

Needless to say, the analyst reiterated a Buy rating on the stock with a price target of $40.

Is Intel a Buy, Sell, or Hold?

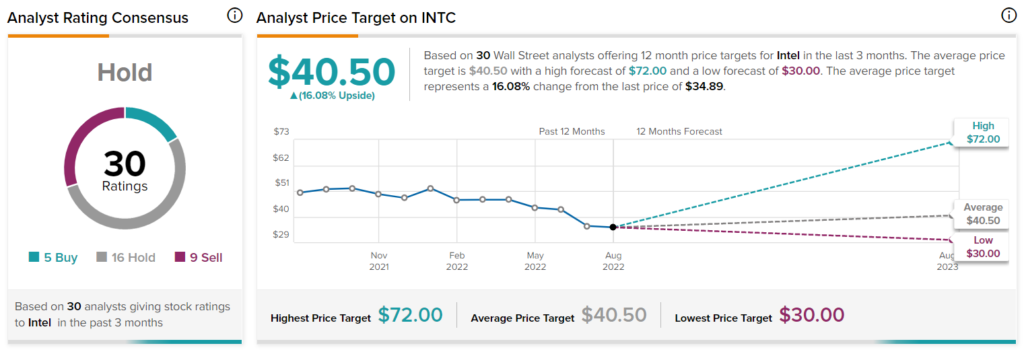

Wall Street is yet to arrive at the same conviction as Bolton and has a Hold consensus rating on Intel, which is based on five Buys, 16 Holds, and one Sell. INTC’s average price target is $40.50, indicating a 16.08% upside from current levels.

Parting Thoughts

The financial strength that the semiconductor investment program is expected to offer Intel holds most solutions to the concerns about the company’s future. Cash flows will start reflecting in the company’s profitability earlier than expected, which will boost its dividends as well as share gains.