Buy low and sell high, we’ve all heard it before. For stock investors, it means finding an optimal combination of low point of entry and return potential. The trick is finding low-cost stocks that are fundamentally sound; share price always drops low for a reason, so you need to find stocks that are low for reasons that won’t press it down further.

Among the stocks that are getting the thumbs up are three that show a strongly attractive profile for retail investors: an initial price below $10 per share, a Strong Buy rating from the Street, and over 100% upside potential.

We’ve used the TipRanks database to pull up these stocks and find out what else makes them so compelling. Let’s take a closer look.

Aspen Group (ASPU)

The first company on our list is an education holding company, using tech to develop the infrastructure and expertise on its two major subsidiaries, Aspen University and United States University. The company has set a goal to make college affordable. Both subsidiary schools are fully accredited post-secondary institutions offering a variety of undergrad and postgrad programs.

Like many online services, Aspen Group saw revenues increase through the corona crisis period. This past May, Aspen reported that fiscal Q4 enrollment was up 23%, with over 2,100 new students. Along with the enrollment growth, Aspen reported $32.2 million in new bookings, for a 21% yoy gain. For the end of fiscal year 2021, Aspen reported having $8.5 million in cash on hand along with $5 million in undrawn credit, for a total of $13.5 million in total liquidity.

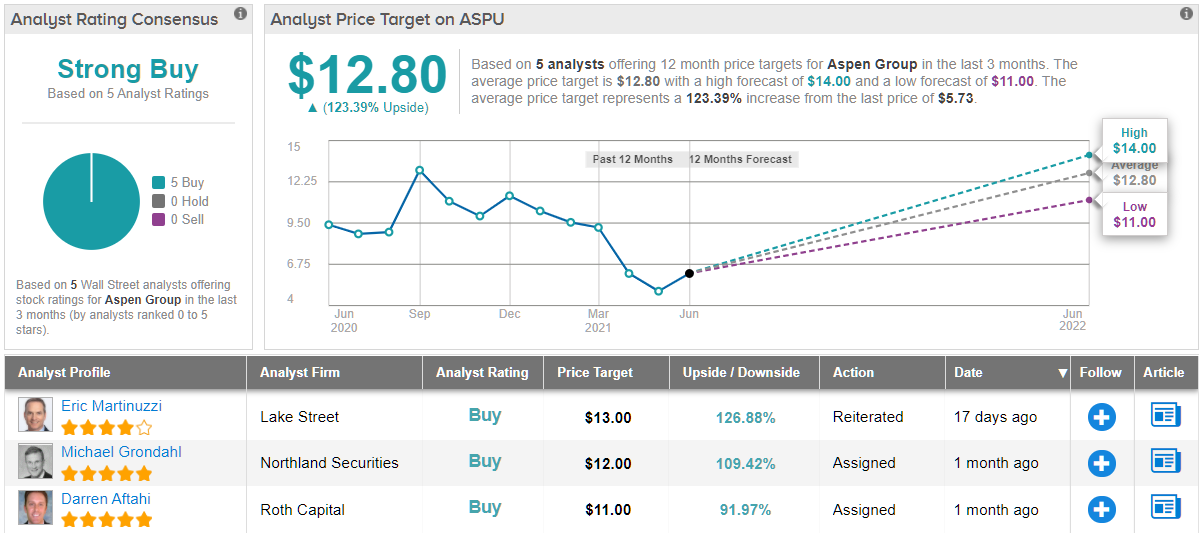

Aspen stock, however, is down ~50% year-to-date. This opens up an attractive entry point, according to Craig Hallum analyst Jeremy Hamblin.

“We believe the stock’s weakness over the past couple of months is largely tied to near-term trading technicals and concerns around the impact from the forthcoming Russell rebalance. We believe this has created an excellent risk/reward opportunity as the fundamentals of the story remain firmly intact. We continue to see a long runway of growth at ASPU with revenue growth in the 25% – 30% range over the next several years putting the company on pace to reach $100M+ in revenues in CY22,” Hamblin opined.

To this end, Hamblin rates ASPU a Buy along with a $14 price target. Investors could be sitting on gains of 144%, should Hamblin’s forecast play out over the coming months. (To watch Hamblin’s track record, click here)

Sometimes, Wall Street’s analysts all agree, and that’s the case here. ASPU has 5 recent reviews and all are to Buy, giving the stock a Strong Buy consensus rating. Shares are trading for $5.73 with an average target of $12.80 implying ~123% one-year upside. (See ASPU stock analysis on TipRanks)

Alto Ingredients (ALTO)

Changing gears, we’ll move over to the bio-renewable industry, where Alto Ingredients is a producer of specialty alcohols and other essential ingredients used in beverages, industrial fuels, cosmetics, and pharmaceuticals. The company’s products include, in addition to alcohols, feed products like yeast, corn glutens and oils, and distillers grains; also, low carbon renewable ethanol fuels. Alto has production facilities in California, Oregon, Idaho, and Illinois. In January of this year, the company took on the name Alto Ingredients, changing it from Pacific Ethanol.

In a recent move that streamlined production facilities and provided capital for debt reduction, Alto in May closed out the sale of its Madera, California ethanol fuel production facility. The sale, to Seaboard Energy, totaled $28.3 million, of which $19.5 million as a cash payment to Alto and $8.8 was as assumption of liabilities by Seaboard. After the deal, Alto used the cash to prepay principal and interest on a senior note issue. The company now has just $0.7 million remaining in outstanding notes.

Alto showed some mixed results in its Q1 financial results. Revenues, from net sales, came in at $218.7 million, which were down 29% from the $311.4 million reported in the year-ago quarter – but up 29% from 4Q20. Earnings showed strength. At 6 cents per share, the EPS was a definite turnaround from the 30-cent loss reported in Q4 and the 47-cent loss reported in 1Q20.

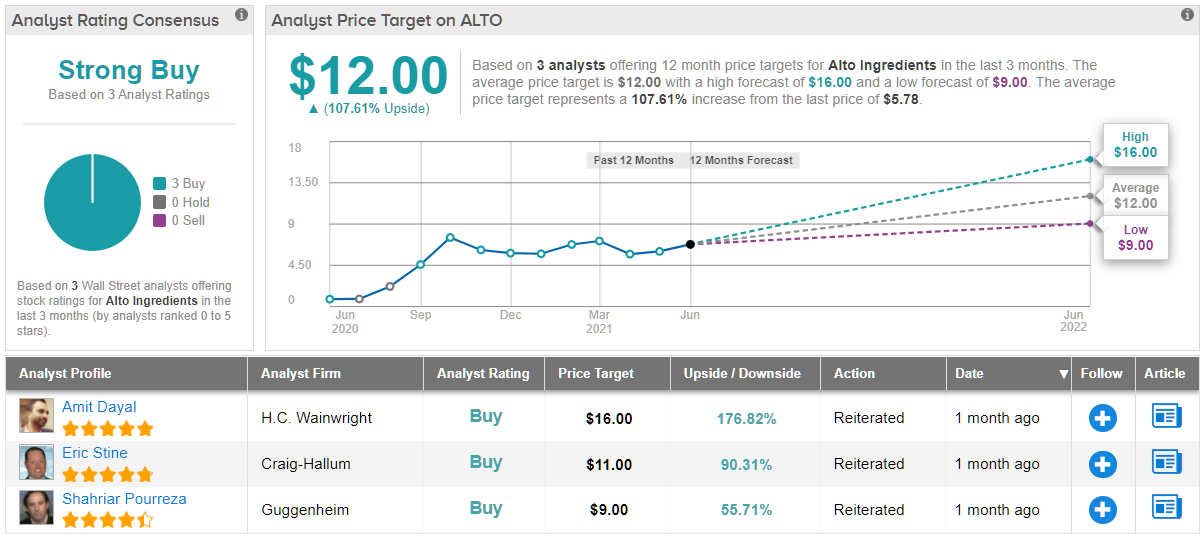

All of this caught the attention of 5-star analyst Amit Dayal from H.C. Wainwright, who rates ALTO a Buy alongside a $16 price target. This target suggests the stock will be changing hands for a ~177% premium a year from now. (To watch Dayal’s track record, click here)

“We believe investors should conservatively assume that moving closer to full utilization of specialty alcohol capacity may take a couple of years. We believe the company could be net-debt free by the end of 2021, supported by operating cash flow improvements and ongoing asset sales… We believe these improvements could generate $5M in EBITDA improvements annually. Ingredients related M&A and expansion into carbon sequestration continue to remain potential mid-to-long-term upside drivers in the story. Investors should note that we adjust our market prices for the company’s offerings and feedstock costs on a quarterly basis to match prevailing trends. This should cause our revenue and earnings expectations to vary sequentially. However, we reiterate that the historical volatility in the company’s financial performance should now be meaningfully lowered, supported by the stability in the ingredients segment,” Dayal wrote.

All in all, ALTO’s Strong Buy consensus rating is unanimous, based on 3 recent positive reviews. The stock has an average price target of $12, suggesting ~108% one-year upside from the current price of $5.77. (See ALTO stock analysis on TipRanks)

TRACON Pharmaceutical (TCON)

Last but not least is TRACON Pharma, a clinical stage biopharma company focusing on new targeted medicines for cancer treatment. The company is working on development and commercialization of its drug candidates. TRACON has an active pipeline, with envafolimab, the leading candidate, currently undergoing 7 active clinical trials, of various stages, in multiple countries.

Envafolimab is a single-domain PD-L1 antibody, administered by subcutaneous injection. The drug is being evaluated as a treatment for a range of solid tumor cancers. The key clinical study in the US is the ENVASARC Phase 2 pivotal trial, which will test the drug against Undifferentiated Pleomorphic Sarcoma (UPS)/Myxofibrosarcoma (MFS). The study is currently dosing patients, and earlier this month the Independent Data Monitoring Committee recommended that the trial proceed as planned. The committee examined safety data on more than 20 patients enrolled so far, in two separate test cohorts.

In other recent development program updates, the company this month reported progress on its Phase 1 study of uliledlimab and atezolizumab. Reporting on data from 20 test patients with advanced or metastatic solid tumors, the company showed evidence that the drugs were safe and well-tolerated at a range of doses, and demonstrated some clinical activity in a significant number of patients. The results were presented at the virtual annual meeting of the American Society of Clinical Oncology.

5-star analyst Soumit Roy, of JonesTrading, notes the developments in the envafolimab trial, and goes on to say, “We believe TRACON is developing a first in class subQ PD-L1 inhibitor that is well positioned for accelerated approval in UPS/MFS subtypes of soft tissue sarcoma…. We could also see envafolimab expand into additional soft tissue sarcoma types like ASPS, angiosarcoma and dedifferentiated liposarcoma (DDLS), indicating further upside to our PT…. we could see an additional approx. $450MN in peak sales in 2031 with positive data and approval. With the potential market expansion into additional indications and key data catalysts in 2021, we are reiterating BUY rating…”

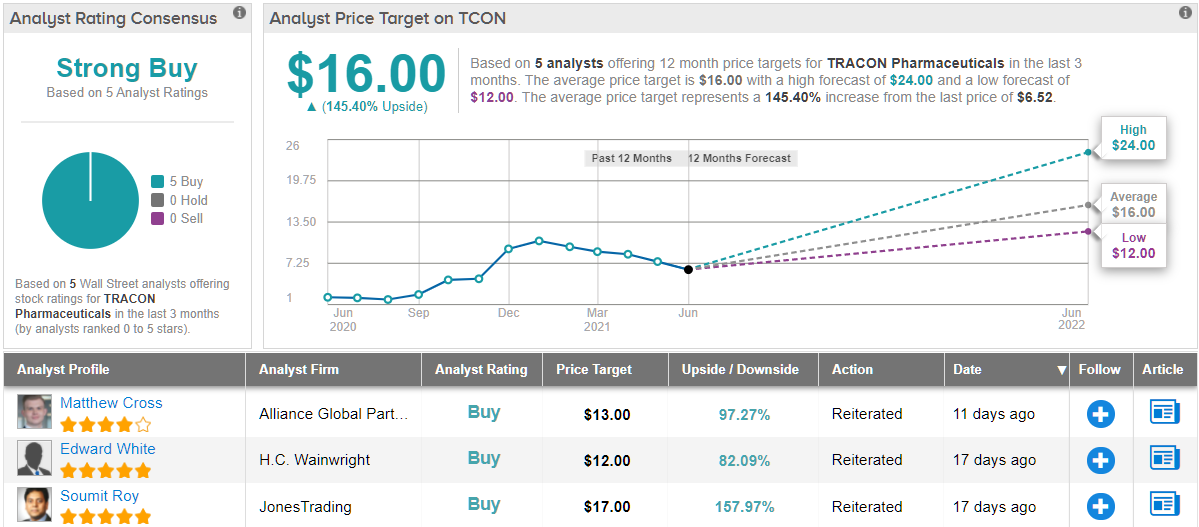

Along with this Buy rating, Roy give TCON a $17 price target, indicating his confidence in a solid 161% upside potential. (To watch Roy’s track record, click here)

Once again, we’re looking at a stock with a unanimous Strong Buy rating – derived from 5 positive analyst reviews. TCON shares are priced at $6.52 and have an average price target of $16; this suggests the stock has room for ~145% growth in the year ahead. (See TCON stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.