The year 2022 is barely one month old, and the stock market is starting it off with sharp downturn. In a way, this shouldn’t be too surprising. Inflation started taking off in the second half of last year, and reached an annualized rate of 7% in December. The Federal Reserve, normally tasked with watchdogging inflation, had already been talking about raising interest rates; this anti-inflationary move was a possibility that moved to a probability. Now it’s certainty, and sooner rather than later.

This week, the Fed’s Open Markets Committee made it known that it will likely begin instituting rate hikes this year, perhaps as early as March. The move will be the first such increase in over three years, and will also mark the official end of the central bank’s market-supporting ‘easy money’ policy.

A rising interest rate regime is typically associated with a lower return rate in stocks, but that’s an average. Some stocks will thrive in the new environment, and the Street’s analysts are sorting through the traded equities, looking for those that are primed for gains.

Using TipRanks’ database, we pinpointed three such stocks that are poised to benefit from rate increases. These are Strong Buy tickers, according to the analyst community, and all three offer considerable upside potential. Let’s take a closer look.

Silvergate Capital (SI)

The first stock we’re looking at is Silvergate Capital, a commercial bank based in California. The bank specializes in financial services for the digital currency industry, serving digital currency exchanges, institutional investors, and fintech software companies. Silvergate has been in business since 1988, shifted to the digital currency business in 2013, and has grown with its target sector. The bank has been profitable for 20 years, and currently boasts over 1,300 clients.

Silvergate reported several sound metrics from 4Q21. The bank’s total assets exceeded $16 billion, compared to $5.5 billion at the end of 2020. Total net income was down sequentially, falling from $23.5 million in Q3 to $21.4 million Q4 – but the Q4 result was up an impressive 135% year-over-year. The company’s average deposits from digital currency customers grew 18% sequentially, to $13.3 billion.

Net income available to shareholders was reported at 66 cents per share. Like the revenue, this was down from Q3, when it came in at 88 cents per share, but up from 4Q20. The yoy gain was 40%. In total dollars, quarterly net income for shareholders was $18.4 million.

Commenting on the impact of Fed policy on Silvergate, Wedbush 5-star analyst David Chiaverini says, “Rate hikes should benefit SI the most… SI is the most asset sensitive bank in our coverage as a 100 bp increase in rates should benefit NII by 52% as of 3Q21.”

Overall, the top-ranked analyst takes a bullish stance on Silvergate, noting: “We remain positive on SI given the strong underlying fundamental performance of the core business and we continue to see a significant amount crypto hedge fund capital formation and capital inflows into the space… [SI] has a favorable growth outlook, its strong network effects discourage new entrants, there’s significant potential stemming from the rapidly expanding digital currency market, and the incremental benefit from its stable coin initiative.”

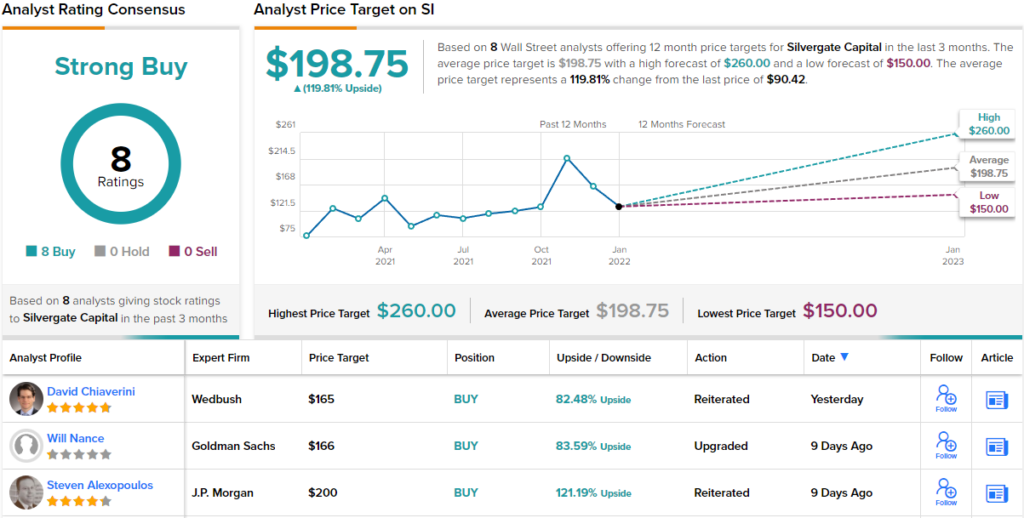

To this end, Chiaverini rates Silvergate shares an Outperform (i.e. Buy), while his $165 price target implies a 12-month gain of ~82%. (To watch Chiaverini’s track record, click here)

Overall, Silvergate has been getting some love from Wall Street, where the analysts give it a unanimous Strong Buy consensus rating, based on 8 positive reviews. The stock is selling for $90.56 and its $198.75 average price target indicates potential for ~120% upside this year. (See Silvergate stock forecast on TipRanks)

Signature Bank (SBNY)

Next up is Signature Bank, one of the country’s 25 largest banks. It has operations in the New York City metropolitan area, in California, and North Carolina; customers can go to any of the 36 private client offices or access banking services online. The bank has more than $96 billion in total assets, including over $53 billion in loans, and has more than $100 billion in total customer deposits. Signature serves a group of high-net-worth clients, including privately owned business, their owners, and their senior managers.

High-end banking is a lucrative business, and Signature has seen its earnings grow – with one blip – for the past two years. The blip came between 4Q20 and 1Q21, when EPS sipped sequentially by 1%; other than that, the company’s EPS has consistently shown sequential EPS gains since the second quarter of 2020. In the most recent quarterly report, for 4Q21, earnings came in at $4.34 per share based on $272 million in net income. Both numbers were company records.

The high quarterly income came along with strong increases in total deposits and loans in Q4. Deposits grew by $10.57 billion, to reach $106.1 billion, while loans made grew by $6.28 billion, another company record. Loans have increased by 32%, or more than $16 billion, since the end of 2020.

The bank’s large loan business puts Signature in a sound position to increase income should rates go up, a point elaborated by Wedbush’s 5-star analyst David Chiaverini.

“The company remains very well-positioned to take full advantage of an impending rising rate environment, with each 100 bp increase in rates expected to generate a 12-13% increase in net interest income. 2022 asset growth guidance calls for $3 to $7 billion in growth for 1Q22 (lower end likely), with $4 to $7 billion in growth per quarter thereafter,” Chiaverini noted.

According to analyst, SBNY is a growth story with a long growth runway. He writes: “The company has multiple growth drivers including its digital asset initiative, West Coast expansion, fund banking division, and new lending initiatives including mortgage warehouse, SBA and an unnamed vertical to be announced soon.”

Chiaverini’s comments support his Outperform (i.e. Buy) rating on SBNY shares. He sets a $415 price target, indicating confidence in a 42% upside for the next 12 months. (To watch Chiaverini’s track record, click here)

Befitting a stock that’s primed for gains in the near future, SBNY has a unanimous Strong Buy consensus rating, based on 15 recent analyst reviews. The stock is selling for $291.88, and its $434.40 average price target implies a one-year upside of ~49%. (See SBNY stock forecast on TipRanks)

F.N.B. Corporation (FNB)

The last stock to benefit from rising rates is F.N.B. Corporation, the holding company for First National Bank. The bank boasts over $39 billion in total assets, along with $31 billion in total customer deposits. First National has operations in 7 states, from the Great Lakes to South Carolina, plus DC, and a network exceeding 330 physical banking offices and 850 ATM machines. The company offers a full range of consumer and commercial banking services.

FNB this month reported its 4Q21 results, showing year-over-year gains in revenues and earnings despite slight declines in both metrics from Q3. The top line came in at $323 million, up 13% yoy, while earnings showed 7% yoy growth to 30 cents. For the full year 2021, total revenues reached $1.2 billion, a company record, and full year earnings grew from 85 cents per share in 2020 to $1.23 in 2021.

During Q4, the company’s total commercial loans increased by 5.3% to $817.2 million, and its consumer loans grew 6.4% to $514.7 million. While the company’s total interest earnings assets increased by an annualized rate of 9.6% in the quarter, to $831.6 million, Q4 net interest income (NII) slipped 3.9% to $223.3 million. This is, in part, due to the current low-rate regime, which brings us to the prospect of a Fed rate hike.

Russell Gunther, from D.A. Davidson, sees Fed action on rates as a strong positive for FNB, as the bank subsidiary has a large business in loans and other interest earning assets. He writes: “NII guide of $965M-$1,005M (non-FTE) includes Fed rate hikes in June and September with 3% additional upside should the Fed move in March… We forecast steady NIM expansion beginning in 1Q22E as we layer in 3 rate hikes in ‘22E (2Q-4Q) and a fourth in 2Q23 for this asset sensitive name.”

Expounding on FNB’s valuation, the analyst stated, “FNB looks cheap relative to its inline return profile vs. Mid-cap peers, and vs. asset sensitive names in particular.”

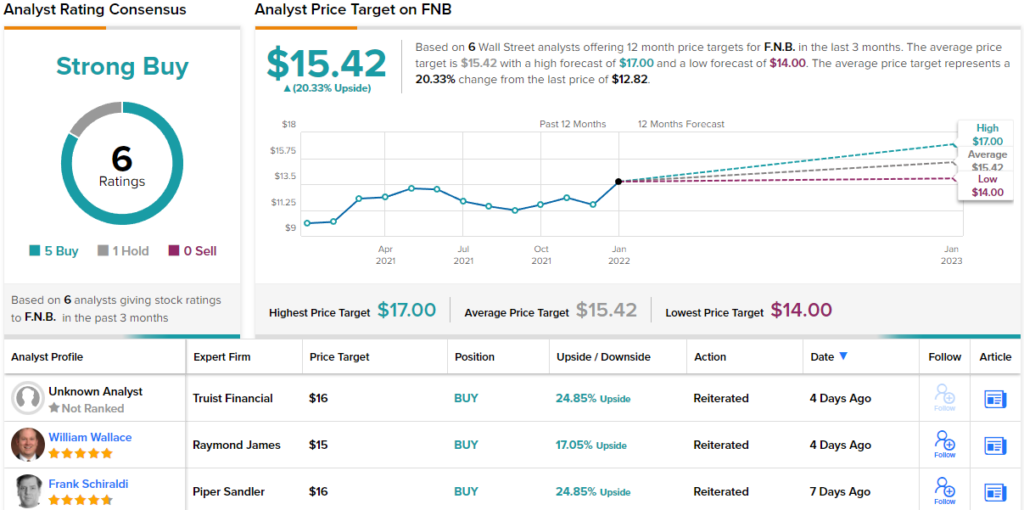

All of this prompted Gunther to rate FNB shares a Buy along with a $12 price target. This target conveys his confidence in FNB’s ability to climb ~33% higher in the next year. (To watch Gunther’s track record, click here)

Overall, a 4 to 1 advantage of Buy ratings over Holds gives FNB its Strong Buy consensus view. The shares are trading for $12.87 and their $15.42 average price target suggests ~20% upside in 2022. (See FNB stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.