The rally we’ve experienced in the stock markets has become something of a sensation. The rebound has been substantial, with the S&P 500 rising almost 34% from its March 23 trough.

Even in the current buying mood, however, there are plenty of investors who want a cautious strategy. They believe that the future is uncertain, that given the combination of coronavirus, social unrest, and a Presidential election year, there is no way to truly predict market behavior. They are not necessarily wrong, but even the most cautious investors can develop a bullish strategy.

With plenty of evidence for both the bulls and the bears, the smart play now is to buy into rising dividend stocks, shoring up the portfolio for whatever lies ahead. The advantage of such a fundamentally defensive strategy is obvious: stocks that are rising now will bring the immediate gains of share appreciation, while strong dividends will provide a steady income stream regardless of market conditions.

Using TipRanks database, we’ve found three dividend stocks that are yielding at least 8%, and are backed by enough analysts to earn a “Strong Buy” consensus rating.

Magellan Midstream Partners (MMP)

The first stock we’ll look at here is Magellan Midstream. This Oklahoma-based company is major player in the oil and gas industry, with a market cap over $10 billion and an asset map that touches on most states east of the Rocky Mountains. Magellan transports both refined products and crude oil through a network of pipelines and terminals, including Gulf Coast marine terminals connecting to the export trade.

The importance of midstream to the energy industry helped insulate Magellan from the economic downturn in Q1, and while earnings slipped sequentially, they still came in 24% above expectations. The $1.28 reported marked the fifth quarter in a row that MMP beat the earnings forecast. At the same time, the outlook for Q2 is less rosy, at just 73 cents per share.

Last month, Magellan priced a $500 million issue of senior notes, due in ten years. These notes will help pay down higher interest debt that comes due next year, and improves the company’s liquidity position, important points in uncertain economic times. The new debt carries interest of 3.25%, a significant reduction in the company’s debt service payments.

In addition to improving liquidity, MMP management also recently declared the $1.0275 per share quarterly dividend. This payment is the same as the previous quarter’s, which makes sense as the company has a pattern of raising the dividend every other quarter. At $4.11 annualized, the dividend yield is 8.58%.

Wells Fargo analyst Praneeth Satish sees MMP as a reliable choice for dividend investors, writing, “The company intends to maintain the current quarterly distribution for the rest of the year… In the interim, MMP remains well positioned given its strong balance sheet and liquidity position, and ratable cash flow stream, in our view.”

Satish rates the stock a Buy, and his $54 price target implies an upside potential of 14% for the year. (To watch Satish’s track record, click here)

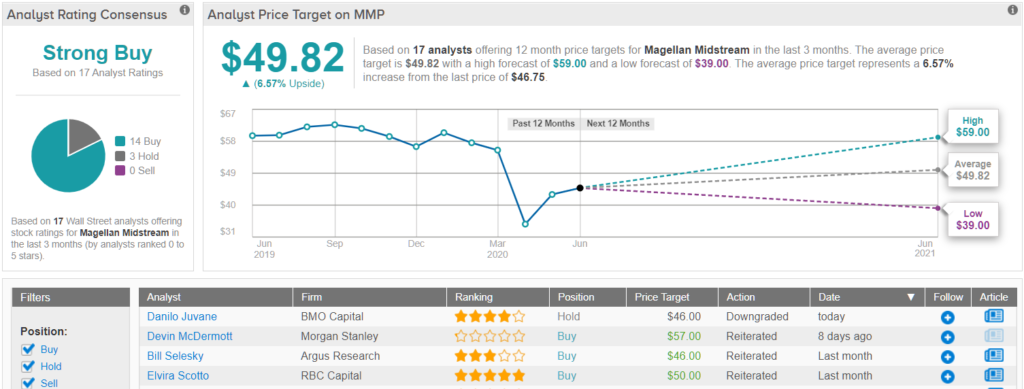

Magellan’s Strong Buy analyst consensus rating is based on no fewer than 14 Buys set in recent weeks, along with 3 Holds. Some caution is evident in the average price target, which at $49.82 represents a 6.5% premium from the $46.77 trading price. (See Magellan stock analysis on TipRanks)

New Mountain Finance (NMFC)

Next up, New Mountain Finance, is a business development corporation. The company controls a portfolio of credit funds and public and private equity worth over $20 billion. Earnings on the company’s portfolio actually increased in Q1, rising from 32 to 34 cents per share. The Q1 number beat expectations by over 6%.

In a nod to the current corona crisis, management lowered the quarterly dividend from 34 cents to 30 cents, but even the lower dividend still gives an annualized yield above 11.92%.

Investors can also note that company officers – the insiders, if you will – have been on a buying spree lately. Their sentiment on NMFC is strongly positive, and insiders have purchased over $7 million worth of company stock in the past three months.

Oppenheimer analyst Chris Kotowski assigned a Buy rating on this stock, citing the company’s resiliency. His $11 price target suggests a 6.5% upside for the next 12 months. (To watch Kotowski’s track record, click here)

In his comments, the 5-star analyst wrote, “Given the quality and liquidity of NMFC’s portfolio as well as support from its manager (which supplied a $50M line of credit and deferred fees), we think they should be able to get this situation in hand in a quarter or two.”

NMFC shares have recently powered right through their average price target, another indicator of investor confidence. The stock sells for $10.33, nearly 1% above the average price target of $10.25. Expect Wall Street’s investors to revisit their expectations here in the near future. In the meantime, 4 of 4 reviews on this stock are to Buy, giving NMFC a Strong Buy analyst consensus rating. (See NMFC stock analysis on TipRanks)

Summit Hotel Properties (INN)

We’ll finish this list with Summit Hotel. A stock in the hospitality sector, in the midst of the coronavirus public health crisis? Yes, really. Summit, an REIT, owns 73 hotels in the US, and boasts over 10,000 rooms. The company’s properties are skewed toward upscale customers, who are less likely to be affected by a cash crunch, even in the current economy. And, Summit entered the current crisis with over $395 million in available credit.

Even with those advantages, Summit’s shares are down 31% after the bears and bulls have had their way in the past three months. But the main result recent volatility has been to inflate the dividend yield. At 72 cents annualized, the company’s dividend gives a yield of 8.9%, 4.5x higher than the S&P average yield.

Deutsche Bank analyst Chris Woronka is duly impressed by the company’s position. He writes of Summit, “[We] expect to see meaningful market share gains as INN leans into the power of the brand platforms and potentially benefits from demand that has been displaced from hotels’ whose highly leveraged owners have had to suspend operations. INN has 27-28 months of liquidity… We view INN as a solid risk-adjusted way to gain exposure to lodging in the nascent stages of recovery.”

In line with this bullish view, Woronka rates INN a Buy. (To watch Woronka’s track record, click here.)

Wall Street is unanimous at INN shares, as 6 analysts have all given recent Buy ratings to the stock. INN’s recent gains have pushed it through the average target as well. The current trading price of $8.36 shows that the $7.67 average price target is simply obsolete. (See Summit stock analysis on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.