TipRanks’ website traffic tool has clearly shown that website traffic and stock prices often exhibit correlations.

Although stock analysis should always be a multifactorial process, website traffic data provides a valid premise on which to base your initial judgment. Here are three stocks with surging website clicks that also hold strong prospects.

New York Times

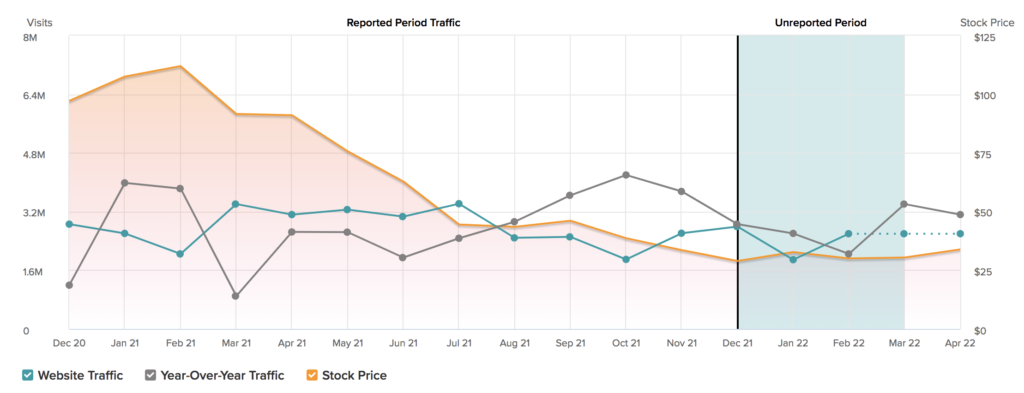

The New York Times (NYT) has provided news to Americans since 1851, but has seldom experienced the level of interest it currently has.

The company’s website clicks have surged by a staggering 97.43% year-to-date amid various high magnitude events such as the war in Ukraine and an abrupt stock market sell-off. I am bullish on the stock due to the rising consumer interest and its firm fundamentals.

The firm recently beat its fourth-quarter earnings estimates by 8 cents per share, and also exceeded its revenue target by $14.22 million. The key drivers behind the firm’s blockbuster quarter were 375 000 new digital subscriptions, and a 26.9% increase in advertising revenue.

The company is well poised for further growth as its CEO, Meredith Kopit Levien, claims that the media giant has a larger addressable market than in the past.

According to Kopit: “Our latest audience research suggests there are now at least 135 million adults worldwide who are paying or willing to pay for one or more subscriptions to English-language news, sports coverage, puzzles, recipes, or expert shopping advice.”

Furthermore, New York Times is undervalued relative to its five-year average price multiples. New York Times stock is trading at a 69.7% price to earnings discount with a PEG ratio of only 0.30, meaning that we’re looking at a stock with value in abundance.

Turning to Wall Street, New York Times stock earns a Moderate Buy consensus rating based on two Buys assigned in the past three months. The average New York Times price target of $55 implies 17.5% upside potential.

GXO Logistics

GXO Logistics (GXO) provides over 900 supply-chain facilities worldwide with a presence in matters such as warehousing, distribution, and order fulfillment, to name a few. I am bullish on the stock amid its surging traction in recent months; GXO’s website clicks have surged by an unbelievable 153,107.44% since the start of the year, leaving few doubting the company’s recent successes.

GXO’s operating activities are a force to be reckoned with. The company posted $2.3 billion in organic revenue during its fourth quarter, amounting to outstanding adjusted earnings per share growth of 70%.

Additionally, GXO has been one of the few supply-chain companies that have scaled its operations during a period of supply-chain bottlenecks, which is reflected in its impressive quarterly EBITDA of $167 million.

The stock is good value for money. It’s trading at a price-to-sales of exactly 1x and a price-to-book of 3.38x, meaning that there’s value in abundance for investors, especially when considering the stock is still in its growth phase.

Turning to Wall Street, GXO stock holds a Strong Buy consensus rating based on seven Buys and one Hold assigned in the past three months. The average GXO Logistics price target of $103.14 implies 50.6% upside potential.

AutoHome

AutoHome (ATHM) is an online autobody retail6% year-over-year increase in monthly website visits, suggesting a change in consumer sentiment after the company’s clicks were trending downwards for most of last year.

It’s not just because of Autohome’s website data that I’m bullish on the stock, but a variety of macroeconomic and internal matters makes this stock a big attraction.

There’s been systemic support behind AutoHome as the Chinese Communist Party pledged its support to the Chinese economy last month, after a prolonged period of contractionary rhetoric coming from Beijing.

According to the CCP’s central committee, it will expand its economy: “Regarding macroeconomic operation, we must implement the decisions and arrangements of the CPC Central Committee, effectively invigorate the economy in the first quarter, proactively respond to monetary policy, and maintain moderate growth in new loans.”

The aftereffect of this statement has bolstered consumer discretionary and industrial companies such as AutoHome as it will now be catering to a higher-spending economy.

From an internal vantage point, AutoHome has experienced robust growth by beating its fourth-quarter earnings estimates by three cents per share. Furthermore, AutoHome holds a mammoth $3.25 billion in cash on its balance sheet, which has been partially distributed in dividends at a forward yield of 0.49%.

An alternative for AutoHome bolstering its future dividend payments could be to re-invest the capital, thus expanding the entity’s intrinsic value. Regardless of the route the company follows, it’s a win-win for its investors.

AutoHome stock is trading at a bargain price. The stock’s price-to-earnings ratio is trading at a 77.5% discount relative to its five-year average, suggesting that the company’s earnings per share are yet to be priced in by the market.

Additionally, AutoHome’s price-to-sales ratio is trading at a discount worth 53.6%, conveying the fact that the company’s top-line revenue justifies a higher stock price.

Turning to Wall Street, AutoHome stock has a Hold consensus rating based on two Buys, three Holds, and two Sells assigned in the past three months. The average AutoHome price target of $32.16 implies 3.9% downside potential.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure