Even though COVID still makes headlines, with Delta and other variants, the world is starting to emerge from the economic disruptions of the pandemic. Vaccination programs are expanding, and – with the notable exception of Australia – governments are growing leery of imposing strict lockdowns again. The result is a return to economic growth, and a resumption of global trade.

Protect Your Portfolio Against Market Uncertainty

- Discover companies with rock-solid fundamentals in TipRanks' Smart Value Newsletter.

- Receive undervalued stocks, resilient to market uncertainty, delivered straight to your inbox.

While supply chains still have not returned to normal, some industries are showing impressive gains. Drybulk, the seaborne trade in raw materials carried in bulk lots on freight vessels, is one of these.

Looking at the near- to mid-term prospects for global trade, H.C. Wainwright analyst analyst Magnus Fyhr writes: “…we remain constructive on the outlook for the drybulk market as we believe moderating demand growth coupled with limited fleet growth should result in further tightening of the supply/demand balance and support strong vessel earnings over the next year. While seaborne trade volumes are well above pre-pandemic levels and growth in China is slowing down, commodity demand for the rest of the world is catching up and should support further growth in seaborne trade volumes.”

Fyhr goes on to point out several drybulk equities that he sees continuing to gain in the current trade environment. We are talking returns of at least 40% over the next 12 months. It also doesn’t hurt that each stock is admired by the rest of the analyst community, enough so to earn a “Strong Buy” consensus rating.

StarBulk Carriers (SBLK)

We’ll start with Star Bulk Carriers, a specialist in the drybulk ocean trade. This Greek-based company has an ‘on the water’ fleet of 128 carriers, averaging 9.3 years old and including both the largest Newcastlemax and Capesize carriers for the long hauls as well as the smaller Ultramax and Supramax vessels that hope from port to port along coasts. Shares in Star have gained 188% this year.

The quality of Star’s fleet and capabilities is clear from the company’s financial performance. In early August, Star reported a net profit of $124.2 million for 2Q21, or $1.22 per share. This result represented tremendous gain turnaround from the 46-cent net loss reported in the year-ago quarter, and was up 238% from Q1. At the top line, the $311 million reported revenue was more than double the year-ago figure, and the best quarterly revenue in over two years. The company finished the quarter with $238 million cash on hand.

Star’s sound finances backed the company’s 70-cent per common share dividend. The payment, which was slashed down to just 5 cents during the pandemic crisis, has been raised twice so far this year. The current payment annualizes to $2.80 per common share and gives a solid yield of 4.2%.

Star shares have raced ahead 188% this year, but would you believe it could go up another 45%? H.C. Wainwright’s Fyhr does. The analyst rates SBLK a Buy along with a $35 price target. (To watch Fyhr’s track record, click here)

“With most of the fleet operating in the spot market, we believe SBLK is well positioned to capture current strength in the spot market. With an average fleet cash break-even level of $9,800/day, including debt amortization, we believe SBLK is poised to generate significant cash flows in 2021 and 2022. While spot rates are at a ten-year high, we still believe that we are in the early stages of a multi-year cycle as steady demand growth coupled with lower fleet growth should result in improved utilization and firmer charter rates over the next few years,” Fyhr opined.

The analyst summed up, “We believe SBLK shares are attractively valued trading at 4.5x our 2021E EV/EBITDA and a 9% premium to our current NAV estimate of $21.63/share compared to the drybulk yield peer group…”

A full house of Buys – 5, in fact – provides the shipping company with a Strong Buy consensus rating from the Street. The average price target comes in at $31.75 and indicates ~31% upside from current levels. (See SBLK stock analysis on TipRanks)

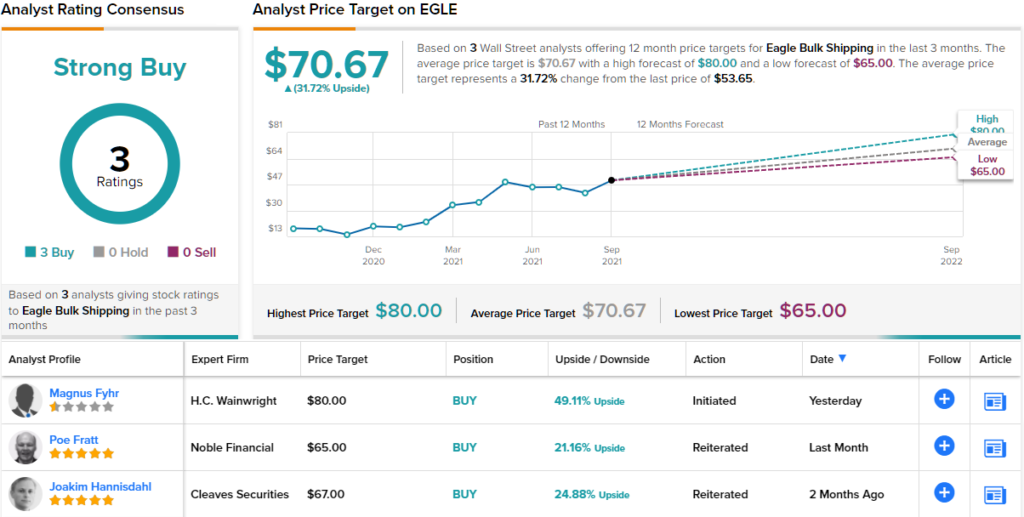

Eagle Bulk Shipping (EGLE)

Next up, Eagle Bulk Shipping, is another major player in the drybulk sector. The company focuses on the shorter-haul trade, with a fleet of Ultramax and Supramax vessels in the 50K to 65K ton deadweight range. Eagle’s fleet comprises 53 vessels totaling 3.2 million tons – and at 8.8 years average, it’s a younger fleet than Star’s above. Eagle’s ships carry a wide range of cargos, including cement and coal, fertilizer and grains, and iron and other ores.

In the second quarter of this year, Eagle posted revenues of $129.9 million, up more than 126% from the year-ago quarter. EPS was down 10 cents sequentially, from 84 cents in Q1 to 74 cents in 2Q21. Higher charter rates this year compared to last year helped to drive the increase in revenues. Eagle reported $83.8 million in cash as of the end of June, as well as an additional $56 million in undrawn credit, to balance $176 million in outstanding debt.

Wainwright’s Fyhr initiated coverage of Eagle with a Buy rating and an $80 price target that indicates potential for 49% growth over the coming year.

Backing this stance, the analyst points to sound fundamentals in the drybulk carrying sector: “With slower fleet growth and robust Chinese demand for iron ore and coal, we expect the drybulk market to continue to improve, albeit at a slower pace than in 2021. While demand growth is expected to exceed supply growth in 2022, we believe much of the demand growth hinges on that drybulk demand recovers in the rest of the world to offset slowing demand in China.”

The analyst added, “We believe EGLE shares offer an attractive play on the drybulk market with a clear focus on the Supramax/Ultramax market segment… We believe EGLE shares are attractively valued trading at 3.1x 2021 EV/EBITDA and 14% discount to our NAV estimate of $59.34/share, which compares favorably to the drybulk peer group…”

Overall, there are only 3 analyst reviews on file for this company, and all agree that the stock is a Buy proposition. EGLE shares are priced at $53.65 with an average target of $70.67 suggesting an upside of ~32% in the next 12 months. (See EGLE stock analysis on TipRanks)

Genco Shipping, Inc. (GNK)

We’ll wrap up with Genco, another operator of high-end, modern bulk carriers. Like Star above, Genco operates a fleet of mixed capacity, from Supramax vessels of 55K deadweight tonnage to the largest oceangoing Capesize carriers.

Genco has seen recent strong gains in revenues and earnings, as well as a sharp increase in share price. GNK is up nearly 190% this year, and the company beat the revenue and earnings estimates in its 2Q21 financial report. That quarterly report showed $121 million at the top line with a net income of $32 million, or 75 cents per share. The EPS was the highest since 2010. Genco finished the second quarter with $161.2 million in cash on the balance sheet.

These sound results are supported by increasing charter rates in the shipping industry, and improved efficiencies in fuel usage. On the latter note, Genco in June entered into a multi-company framework agreement to test the viability of ammonia as an alternative fuel for maritime uses. The feasibility study is part of larger efforts to decarbonize the global bulk carrier fleet.

Since alt fuels are still in the early study stage, Genco is also taking steps to modernize its fleet. The company in May entered an agreement to acquire two new Ultramax vessels in 2022. These new vessels will be constructed in China and delivered to Genco in January of next year. Both new vessels will incorporate fuel efficiency technology to improve operating costs.

For Q2, Genco increased its dividend from 5 cents per common share to 10 cents. This was the second consecutive quarterly dividend increase, and marks a commitment by the company to grow the dividend back to pre-pandemic levels. At the current level, the dividend yield is modest, just under 1%.

Once again, we check in with H.C. Wainwright’s Fyhr. The analyst sees Genco holding a solid position in its industry, writing of the company: “We believe GNK shares offer an attractive play on the drybulk market as the Capesize fleet is highly leveraged to Brazilian iron ore exports while the Supramax fleet provides stable cash flows to cover debt service and overhead.… In addition, GNK has installed scrubbers on 17 of its larger Capesize vessels, which we believe could provide additional fuel cost savings. While spot rates are at an eleven-year high, we still believe that this cycle has additional legs as steady demand growth coupled with lower fleet growth should result in improved utilization and elevated charter rates over the next few years.”

In line with these comments, Fyhr starts his overage of the stock with a Buy rating and a $30 price target. If correct, the analyst’s objective could deliver one-year returns of 41%.

All in all, Genco has attracted 6 recent analyst reviews, and these break down 5 to 1 in favor of Buy over Hold, for a Strong Buy consensus. The average price target of $27.33 implies an upside of ~29% for the next 12 months, from the current trading price of $21.22. (See GNK stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.