The global energy shortage has forced many nations to revert to coal usage to fill the gaps in the supply line. The European Union provides an example of coal reversion, with the likes of Germany, Austria, and the Netherlands tapping into reserve energy coal plants to fuel their economies.

More nations are being squeezed by the short supply of oil and gas, meaning that most coal producers could see their sales grow exponentially in the coming years. Moreover, the price of coal has risen by 190% in the past year, providing primary producers with much operating leverage.

In this piece, I used TipRanks’ Comparison Tool to look at three solid coal-mining companies that I am bullish on.

Arch Resources (ARCH)

Arch Resources operates seven active mines in North America, producing thermal and metallurgical coal. The company’s mines are long-duration assets that provide the firm with pricing power, which can be seen in its gross profit margin of 35%.

The firm’s vertically-integrated metallurgical offerings provide it with a powerful market position. Arch’s Leer mine consistently ranks as one of the lowest production cost assets in the United States, and it could soon expand the mine’s operating capacity by mining the Leer South property.

Arch Resources exhibits attractive balance sheet metrics with a current ratio of 1.78x. In addition, Arch sports promising return metrics with a return-on-common-equity ratio of 102%.

Furthermore, Arch stock is undervalued on a normalized basis. Compared to the broader sector, Arch’s price-to-earnings ratio is trading at a 59.6% discount, and its price-to-sales ratio is trading at a 45% discount. Thus, it seems as though the market underscores the stock’s financial capacity.

Although Arch Resources doesn’t provide a mouth-watering dividend profile (its dividend is 0.5%), it can be argued that a dividend increase is in the offing.

To elaborate, the company’s cash dividend payout ratio is 94.4% lower than its five-year average, signaling that Arch’s shareholder compensation could increase soon.

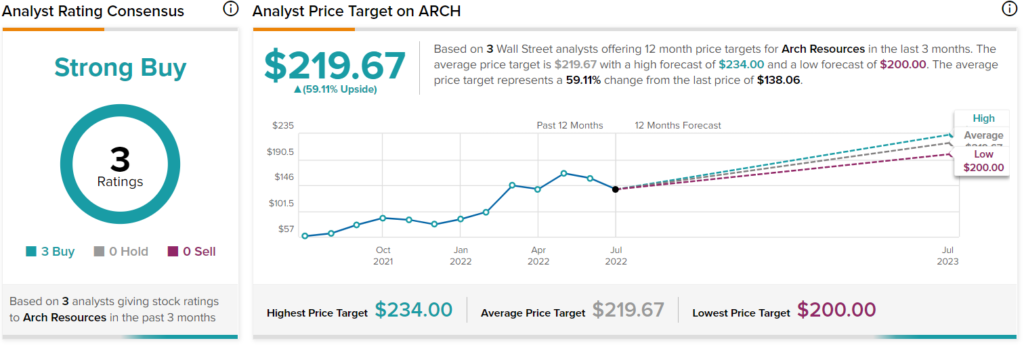

Turning to Wall Street, Arch Resources earns a Strong Buy consensus rating based on three Buys assigned in the past three months. The average ARCH stock price target of $219.67 implies 59.1% upside potential.

Peabody Energy Corporation (BTU)

Peabody Energy is a global coal mining company that operates across various continents. The firm’s operations include seaborne thermal mining, Seaborne metallurgical mining, and powder river basin mining.

The company’s second-quarter financial statements revealed a year-over-year revenue increase of 6.2% and earnings per share of $1.60. Much of the company’s pandemic lockdown-induced glitches were resolved in the quarter, namely its operational restrictions and labor shortages in Australia.

It increased its CapEx in its PRB and midwest mining operations to increase much-needed capacity, and it advanced project activity to re-enter the south workings of North Goonyella and access 70 million tons of reserves.

Furthermore, Peabody’s balance sheet has strengthened considerably in the past quarter by paying off $600 million in debt and raising $320 million through a convertible note offering while retiring higher-cost debt.

Peabody stock provides sound style metrics. The coal miner’s return on common equity (21.95%) and gross profit margin (20.5%) suggest that the company’s investors are getting full value for money from a firm that operates efficiently.

Lastly, Peabody appears undervalued. The stock’s price-to-earnings ratio is at a mere 7x, conveying strength in Peabody’s earnings-per-share ratio. In addition, Peabody stock is trading at a 78.7% discount to its five-year price-to-sales ratio, which implies that the market hasn’t yet calibrated the firm’s top-line potential.

Turning to Wall Street, Peabody Energy earns a Strong Buy consensus rating based on three Buys and one Hold rating assigned in the past three months. The average BTU stock price target of $32.00 implies 54.3% upside potential.

Alpha Metallurgical Resources (AMR)

Alpha Metallurgical produces thermal coal through its 19 active mines in the United States. The firm also owns eight load-out and preparation facilities, providing it with a vertically-integrated business model.

The company posted a monstrous earnings beat in its fourth quarter, as its EPS of $13.45 strolled past analysts’ estimates by $2.01. In addition, Alpha Metallurgical produced $828.22 million in revenue during the quarter, a 155.7% increase year-over-year.

Furthermore, a big attraction for investors is the stock’s dividend prospects. Alpha’s payout ratio of just 1% could increase significantly in the coming years, as its free cash flow yield to dividend yield currently stands at 63.3%.

Moreover, the company’s interest coverage ratio (13.2x) and net income margin (24.5%) add much substance to the debate that the firm’s dividend distribution policy could be more favorable in the coming years.

AMR stock stacks up well against its peers from a relative valuation vantage point. For instance, its price-to-earnings ratio trades at a 76% discount to the sector average, and its price-to-cash-flow ratio is 49% under the sector average. Finally, its price-to-sales ratio is 35% cheaper than its sector.

Turning to Wall Street, Alpha Metallurgical Resources earns a Moderate Buy consensus rating based on one Buy rating assigned in the past three months. The average AMR stock price target of $182.00 implies 59% upside potential.

Concluding Thoughts – Coal Prices Could Hold Up Relatively Well

Commodity prices could retreat soon as consumer spending wanes. However, coal could be an exception, as it’s being utilized to fill energy shortages. The stocks mentioned in this article provide solid total return prospects and can be considered “best-in-class” picks.