The current year is winding down, and investors are starting to prepare for 2022. They’ll shed the non-performers from their portfolios, double down on the winners, and scan the markets to find stocks that are ready to pop. It’s the usual merry-go-round game of the market, just with a New Years’ theme.

In this sort of environment, it’s no wonder to find investors drawn to the top-rated stocks. These are the Street’s Strong Buy-rated equities, the stocks that have picked up a deeply positive consensus view from the market’s top performing analysts. And when analysts of this caliber, with records of success, speak, pointing to stocks with strong upside potential, investors listen.

So let’s take a look at two such stocks, with Strong Buy ratings, upside in the range of 50%, and positive reviews from top analysts. A dip into the TipRanks data can clarify the picture. Here are the details.

Caesars Entertainment (CZR)

First up is Caesars Entertainment, a venerable name in the casino industry. The modern incarnation of the company was formed in 2020, from a merger-by-purchase, when Eldorado Resorts bought Caesars and then took on the name. The current company boasts 53 casino, resort, and hotel properties, mostly in the US but with one location each in Canada and Dubai. Nearly one-third of Caesars’ properties, 16 total, are located in the State of Nevada.

It’s hard to find an industry that drips cash as copiously as casino gaming, and even during the pandemic ‘panic year’ of 2020 Caesars’ managed to bring in $3.5 billion in top-line revenue. This year, with the economy mostly reopened, and consumers both flush with cash and on the prowl for entertainment and leisure, Caesars has already seen $6.89 billion in revenue – just for the first three quarters.

That’s the good news. Earnings, however, are not keeping up, and the company saw a $1.08 loss in Q3, a far cry from the 8-cent positive EPS analysts had expected. It’s important to note that Caesars has seen only one quarter of positive earnings in the last two years, in 2Q21.

The company has been working hard to turn earnings around, following a strategic plan to increase income. In one facet of this, Caesars in April of this year bought the sports betting company William Hill, in a transaction valued at $3.7 billion. The acquisition was rebranded as Caesars Sportsbook, and Caesars recouped much of the purchase price when it sold the European side of the business for $3 billion to 888 Holdings.

In his review of this industry giant, B. Riley’s 5-star analyst David Bain writes: “We believe Caesar’s iconic brand and loyalty synergies from its peer-high room count/scale and rewards membership are scarce attributes. Despite portfolio outperformance and advantages versus peers, our $143 per share land-based valuation utilizes target multiples in line with peers and historical averages—conservative, in our view.”

Bain goes on to add, in regard to the company’s outlook and expansion plans, “We believe CEO Tom Reeg’s deal track record indicates there is ‘more to come,’ potentially (ultimately) unleashing a better digital valuation than peers with better than investor expected market share gains.”

In line with his outlook, Bain rates CZR shares a Buy, and his $191 one-year price target implies an upside of 104%. (To watch Bain’s track record, click here)

Overall, this stock has 11 analyst reviews on record, and from the breakdown it’s clear that Wall Street agrees with Bain; there are 10 Buys against just a single Hold. CZR shares are priced at $93.48 and their $139.70 average price target suggests room for ~50% growth the current share price. (See CZR stock analysis on TipRanks)

Paragon 28 (FNA)

The second stock we’ll look at is about as different from Caesars as it is possible for a stock to get. Paragon 28 is a medical device company, specializing in orthopedic foot and ankle treatments. The company name even references the number of bones found in the foot. Paragon 28’s product line includes a range of surgical aids and orthopedic prosthetics and implants, all aimed at improving patient outcomes and maintaining function in the feet.

Founded in 2010, Paragon 28 is nevertheless new to the public markets. The company held its initial public offering in October of this year, with the FNA ticker making its Wall Street debut on October 15. The offering saw more than 7.8 million shares go up for sale, with an initial price of $16 each. Overall, the company raised $125 million in gross proceeds from the sale.

Of interest to investors, Paragon 28 released its 3Q21 earnings report in November. The company showed $35.9 million in top line revenue, a solid figure that represents a gain of 18% from last year’s Q3, and a gain of 45% from pre-pandemic levels in 3Q19. Looking ahead to Q4, the company expects 8%-11% year-over-year growth, ahead of Street expectations of ~2%.

Canaccord’s 5-star analyst Kyle Rose is bullish on this company, writing: “Paragon 28 came in with a solid first print as a public company, beating guidance and the Street despite a difficult 3Q/21 backdrop given the continued strain of CV19 variants on procedure deferrals and staffing shortages. The company saw continued momentum within the business globally and, despite a somewhat conservative guide for the 4Q with COVID lingering, we expect the groundwork for growth acceleration in 2022+ has been put in place.”

“With a broad portfolio of solutions for foot and ankle disorders, a compelling pipeline of iterative new product launches, and a strong/expanding commercial team, we believe Paragon 28 is reaching its growth stride and positioned to take share in the fastest-growing segment of the orthopedic market,” the analyst summed up.

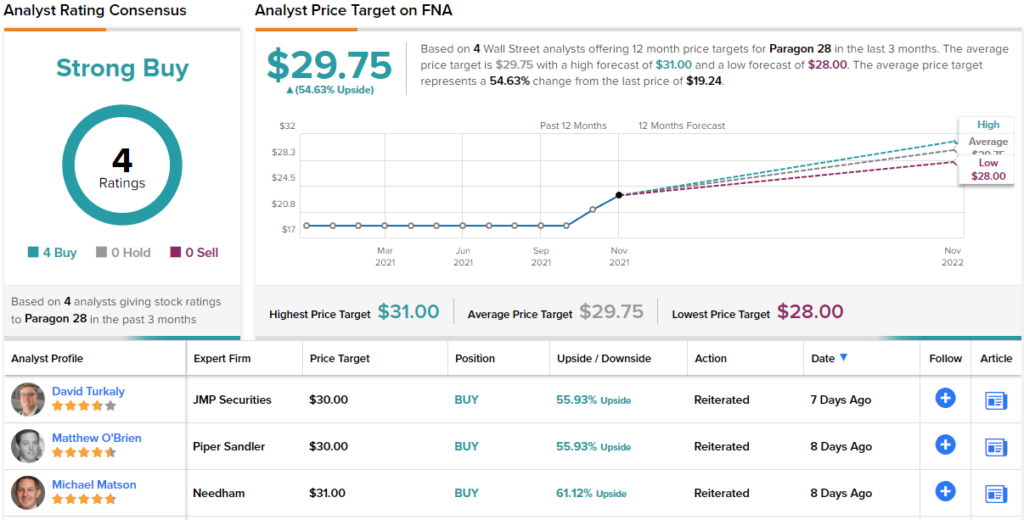

Rose’s upbeat outlook leads him to put a Buy rating on the stock, and his price target, of $27, implies an upside of ~46% for the year ahead. (To watch Rose’s track record, click here)

The Street is in agreement with the bullish position here and all 4 of the recent reviews on Paragon 28 are positive, supporting the Strong Buy consensus rating. Shares are trading for $19.24 and have an average price target of $29.75, suggesting an upside of ~55% in the next 12 months. (See FNA stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.