Wall Street has over 7,600 analysts who give market watchers the low-down on equities from over 9,500 companies, in every imaginable business sector. It’s a database with a wealth of information on current conditions in the market – but the sheer volume of data can intimidate the retail investor.

From that investor’s perspective, this makes rating the analysts as important as rating the stocks. Investors seeking the most trustworthy analysts can turn to the TipRanks list of Wall Street’s top analysts, the 25 best professional stock reviewers working in the markets today. The list rates them on several factors, including the accuracy of their rating calls, the average returns those calls bring, and their total number of reviews.

The results show just who’s at the top of the pyramid among the Street’s analyst corps. Investors can seek out those analysts, to find what stocks they are recommending – and then follow that lead.

So let’s try that. Right now, Oppenheimer analyst Brian Schwartz holds the #4 spot overall. His 409 ratings in the past year have brought in solid results: an 80% success rate, and 33.7% average return. We’ve used the TipRanks platform to look up the details on two of his recent picks. Here is what we found, along with Schwartz’s own commentary.

Qualtrics International (XM)

We’ll start with Qualtrics, a global leader in experience management. XM, experience management, is an industry of growing importance in the digital world; it aims at nothing less than the measurement and analysis of a company’s interactions with, well, anyone. XM can focus on employees, on customers, on service providers – and time that the company interacts with a segment of the public. Qualtrics offers a top-line XM platform via cloud-based software through subscription. The company boasts over 13,000 major brands in its own customer base, including such names as IBM, Toyota, Coca-Cola, Dell, and VW. Qualtrics’ XM platform has over 2 million users across more than 100 countries.

Qualtrics has offices across the developed world – in the US, in Europe, in Central and South America, in Australia, and in Tokyo and Singapore. The company brought in $723 million in revenue in 2020. That figure was up 29%, despite the corona pandemic crisis.

Back in April of this year, Qualtrics’ shares got a boost when the company reported Q1 results that beat the analyst expectation in both revenues and earnings. In the Q2 report, released on July 20, the company beat the revenue estimates again; while shares slipped the next day, the stock is now trading above its July 20 level.

Getting to specifics, the company reported $249.3 million in total revenue, for a 38% yoy gain – and beat the forecast of $241.6 million by over 3%. In a key metric for the coming months, the company announced that it ended 2Q21 with over $754.8 million in ‘current remaining performance obligations’ – a fancy way of describing the backlog. These performance obligations are work that the company will be doing – and the total, which is up 61% yoy, exceeds the full year-year 2020 total revenue.

Looking ahead, Qualtrics’ management provided Q3 revenue guidance in the range of $257 million to $259 million. Analysts had expected forward guidance approximating $246.6 million.

These are the facts that led Brian Schwartz to reiterate his Outperform (i.e., Buy) rating on Qualtrics. In his comments, Schwartz wrote, “Qualtrics had an excellent second quarter. 2Q’s beat-and-raise was driven by broadbased strength, and results display accelerating growth trends across the business metrics. Market demand for experience management solutions is increasing with the category evolution, is a top priority in the current IT buyer mindset, and management is succeeding in exerting Qualtrics’ leadership position to accelerate the growth and capitalize on the opportunity.”

In a point of interest for investors, the analyst added, “Guidance looks conservative given the step-up in Qualtrics’ fundamentals.”

These comments come along with a $55 price target, suggesting room for an upside potential of 45% in the next 12 months. (To watch Schwartz’s track record, click here)

Schwartz is bullish, but he is hardly an outlier on Qualtrics. The stock has 14 recent reviews, and those break down to 10 Buys and 4 Holds, giving XM a Moderate Buy consensus rating. The shares are selling for $38.39, up more than 4% in the day’s trading. The average price target of $48 implies a 26% one-year upside. (See XM stock analysis on TipRanks)

Sprinklr (CXM)

Let’s stick with experience management, and look at Sprinklr. This company, founded in 2009, is another of the tech field’s billion-dollar unicorns, having been valued at $2.7 billion in September of last year. The company offers a SaaS experience management platform, which unifies a series of channels – live chat, email, voice communications – through an AI engine to create a seamless user experience.

Sprinklr held its IPO in June of this year, and the event has generated some conflicting news reports. The company initially priced the offers in the $18 to $20 per share range, with 19 million shares potentially up for sale. The actual IPO, when trading opened on June 23, saw the company make 16.625 million shares available to the public, at a price of $16 each. The shares closed that first day at $17.60. Sprinklr’s gross proceeds from the IPO were $266 million. The company has a current market cap of $4.7 billion.

Prior to the IPO, Sprinklr released financial data for its fiscal year ending January 31, reporting $387 million in total revenue, compared to $324 million for the previous year. The company ran a net loss during the year, of $41 million. This was slightly deeper than the $39 million net loss reported in 2019.

Also in the weeks before the IPO, Sprinklr announced an expanded partnership with Merkle, the European performance marketing agency. The partnership will see the companies expand their reach by offering support to Netherlands-based clients. This was just the most recent of Sprinklr’s partnership expansions in Europe; in April, the company announced a similar agreement with the Portuguese electric utility EDP.

Evaluating Sprinklr after the IPO, Oppenheimer’s Schwartz says as his bottom line, “We believe Sprinklr will deliver above SaaS industry growth over a multi-year horizon as the company exerts an enterprise market leadership position in experience management, an increasingly important software layer that enables companies to gather real-time intelligence for improving engagement, service, and ROI…. we think the pedigree, technology vision, and industry experience of its CEO and leadership could push the company to the top echelon of platforms in experience management.”

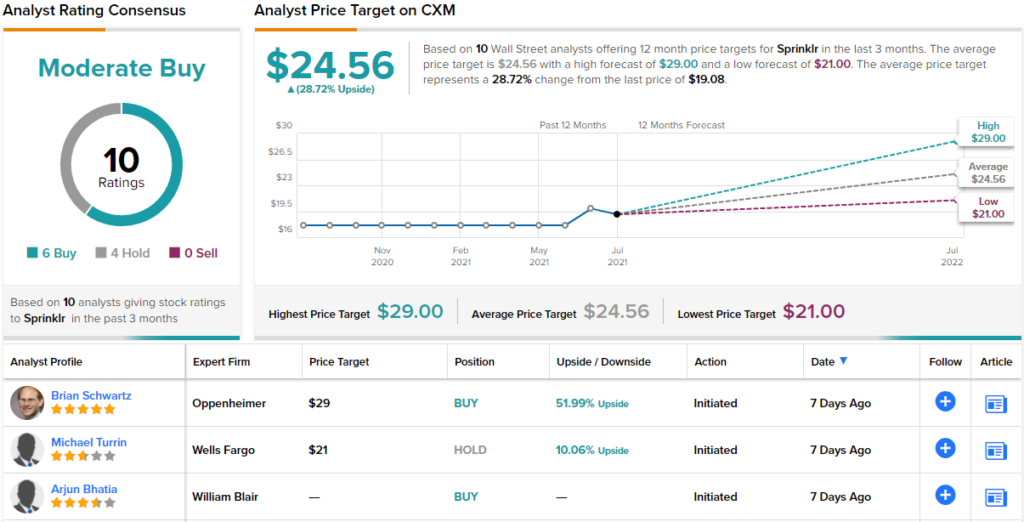

Schwartz is bullish on this new stock, and initiates his coverage as Outperform (Buy), with a $29 price target indicating his confidence in a 48% one-year upside potential. (To watch Schwartz’s track record, click here.)

So far, 10 analysts have weighed in on CXM shares since the IPO – and they are somewhat divided. The breakdown is 6 to 4 Buy over Hold, and the stock has a Moderate Buy consensus rating. The average price target of $24.56 suggests ~29% upside from the current share price of $24.56. (See CXM stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.