For the retail investor, the only certainty of our current market environment is uncertainty. Volatility is up, and the main indexes are showing deepening losses. As if that wasn’t enough, at least one market bull is turning a bit more pessimistic.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

JPMorgan strategist Marko Kolanovic has been one of the more bullish voices on Wall Street in recent months, but current conditions have him pushing the timeline back. While he still believes that the S&P 500 can hit 4,800, or a 32% gain from current levels, he is putting that target into 2023 rather than this year’s end.

Kolanovic sees two main risks ahead, and both are artifacts of policy; central bank policy, which has potential to further damage currency and the stock market, and Russia’s war policy in Ukraine, which is threatening to destabilize the peace of Europe generally. Kolanovic describes the array of policy errors as ‘throwing rocks in glass houses.’

This sort of warning signals it is time for some defensive plays, and this will naturally bring us to dividend stocks. These are the stocks which will ensure a steady income no matter the day-to-day market swings and protect the portfolio against any incoming volatility.

Bearing this in mind, we used the TipRanks’ database to zero-in on two stocks that are showing high dividend yields – at least 5%. Each stock also holds a Strong Buy consensus rating; let’s see what makes them so attractive to Wall Street’s analysts.

WP Carey & Company (WPC)

We’ll start with WP Carey, a real estate investment trust (REIT). The company operates on the net lease model, under which tenants pay all expenses related to property management, including property taxes, insurance, and maintenance, but also frequently upgrades and new construction. The property owner leases out the land to a tenant who has more than the usual freedom to make improvements.

WP Carey operates in the US and Europe, and boasts a total of 1,390 net lease properties, in more than 25 countries, with a total of 170 million leasable square feet. These properties have a 99.1% occupancy rate, and 99.3% of the leases have rent escalations. Overall, from 386 tenant clients, WP Carey realizes annualized base rents in the neighborhood of $1.34 billion.

In the last reported quarter, 2Q22, WPC showed a 7.7% year-over-year gain in total revenues, from $319.7 million in the year-ago quarter to $344.4 million in the current report.

In a metric of interest to dividend investors, WP Carey’s AFFO, or adjusted funds from operations, rose a modest 3.1% y/y to reach $1.31 per diluted share. This increase matters – as the funds from ops is used to fund the company’s dividend, which was increased in the September declaration to $1.06 per common share. This gives an annualized rate of $4.24, for a yield of 6%. This yield is about triple the average found among S&P 500-listed companies.

All of this caught the attention of JMP Securities analyst Mitch Germain, who laid out a bullish take on the stock: “We continue to believe shares will outperform given favorable growth from CPI-linked leases, upside from storage holdings, and a well-diversified deployment strategy, particularly in the face of rising cap rates. The low-levered balance sheet has ample liquidity to fund an upsized deployment target ($1.75-$2.25B), while the story continues to be less complicated. These factors continue to favorably position the company to outperform, in our view.”

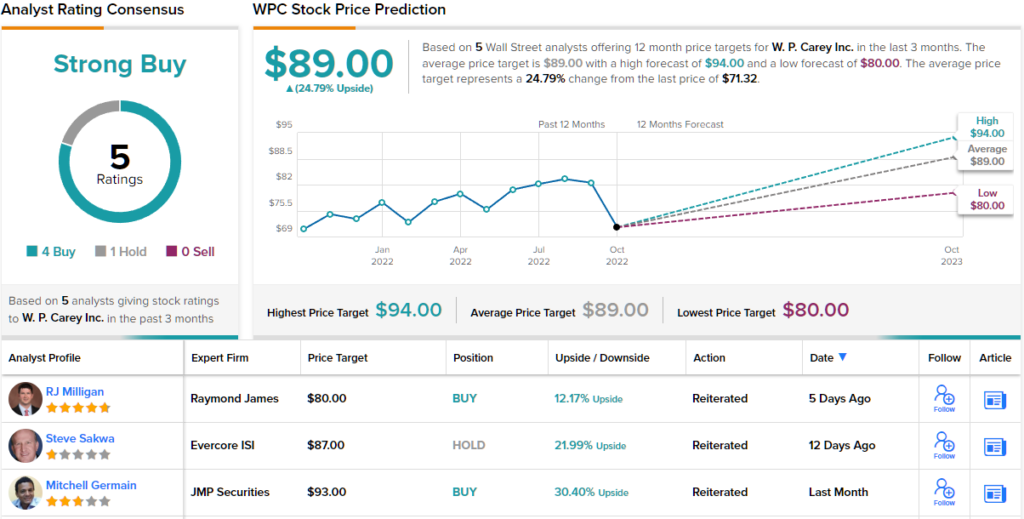

This reinforces the analyst’s view that WPC is a stock to “buy,” and worth a $93 target price. At current levels, this target suggests ~30% upside for the year ahead. (To watch Germain’s track record, click here)

Germain is bullish, but he’s far from the only bull on this stock. WPC has 5 recent analyst reviews, and these include 4 to Buy against just 1 Hold, for a Strong Buy consensus rating. The shares are priced at $71.32 and their average target of $89 suggests ~25% upside for the year ahead. (See WPC stock forecast on TipRanks)

HealthPeak Properties (PEAK)

Now we’ll turn to HealthPeak Properties, another REIT but this one focuses on developing and leasing real estate properties in the Life Science, Medical Office, and CCRC (continuing care retirement community) sectors. HealthPeak has been in business since 1985 and currently has some $20 billion worth of properties in its private-pay healthcare portfolio. The company has structured its portfolio to provide earnings stability and dividend growth no matter how the industry or markets perform.

HealthPeak will release its 3Q22 numbers early next month, but we can get a feel for the company’s performance by looking at the Q2 figures, the most recent reported. The company had a total rental revenue of $387 million, and revenue from resident fees and services of $125.3 million. Add on interest income of $5.5 million, and the company showed a total top line of approximately $517.9 million.

This revenue supported an adjusted FFO of $238 million, or 44 cents per common share. With those funds available, the company paid out it most recent dividend, in August, of 30 cents per share. With an annualized rate of $1.20, the dividend yields 5.3%.

This stock has attracted the attention of Wolfe Research analyst Andrew Rosivach, who is upbeat about HealthPeak’s potential for weathering an economic storm or market turndown. Rosivach writes of the company, “We believe the stock is the ant in the ‘ant and the grasshopper’ story with insulated growth from pre-leased life science developments, a steady MOB record, and healthy balance sheet… Our comment of PEAK being ‘boring’ is a high compliment-we believe the company-by design-has prepared itself for a downturn. We believe ‘ant and the grasshopper’ stocks which were prepared for a downturn will have increased market appeal…”

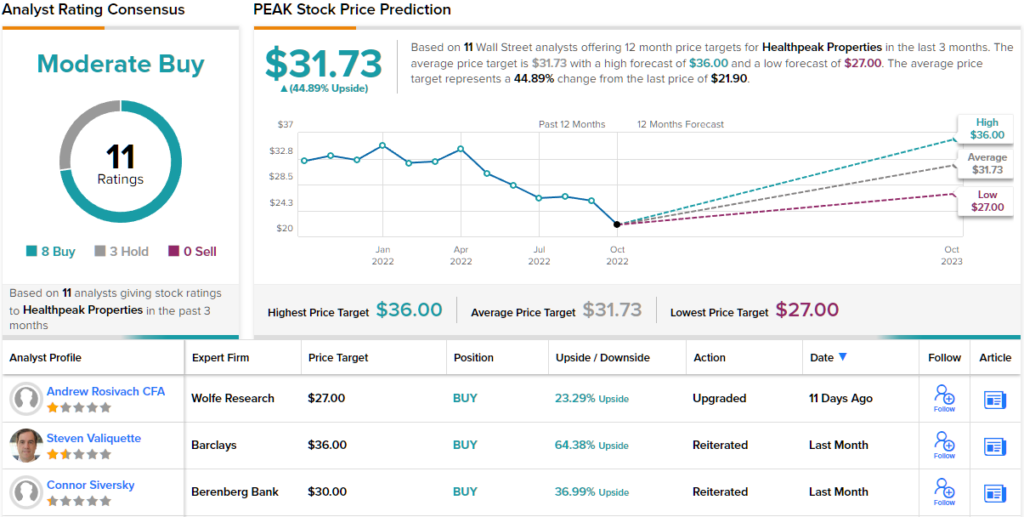

Quantifying his outlook, Rosivach gives PEAK shares a price target of $27, suggesting an upside of 23% for the stock in the coming months. This is accompanied by an Outperform (i.e. Buy) rating. (To watch Rosivach’s track record, click here)

Overall, it’s clear that the Street agrees with the bullish view on this one. Even though there are 3 Hold (i.e. ‘neutral’) ratings among the recent analyst reviews, these are outweighed by the 9 Buy ratings, which give PEAK its Strong Buy consensus. The stock is selling for $21.90 and its average target, at $31.67, implies a gain of ~45% in the next 12 months. (See PEAK stock forecast on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.