The investing game is rarely plain sailing. While no doubt investors would like the choices that make up their portfolio to always go up, the reality is more complicated. There are periods when even shares of the world’s most successful companies have been on a downward trajectory for one reason or another. Amazon is a good case in point.

While it’s no fun watching a stock you own drift to the bottom, any savvy investor knows that if the company’s fundamentals are sound to begin with, the pullback is often a gift in disguise. This is where the chance for strong returns really comes into play. “Buy the Dip” is not a cliché without reason.

Wall Street’s analysts have been noticing that plenty of stocks these days are oversold, and they are not shying away from pointing it out. Using the TipRanks’ platform, we’ve pulled up the details on two such equities. Both Strong Buys with substantial upside potential, according to the analyst community. Let’s dive in.

Twilio, Inc. (TWLO)

We’ll start with Twilio, a software company in the cloud sector, offering a full-service business communications platform designed to facilitate multiple telecom channels, including telephone and VoIP, instant messaging, and video chats, to name the big ones, in a single web-based browser outlet. The company’s service lets users keep all of their communications systems and outlets together, making them easier and more efficient to use and protect.

That Twilio shares were clearly preadapted to thrive during the corona pandemic is clear from the stock’s performance history. TWLO rose sharply, starting in May of 2020, and peaked in February of last year. After that, however, the stock turned volatile, and is now down 55% year-to-date. It’s a dramatic reversal of fortune for the company.

At the same time, Twilio has been posting steadily rising revenues since the end of 2019. In Q4 of last year, the last quarter reported, Twilio’s top line hit $842 million, up 54% year-over-year. For all of 2021, the company showed a 61% y/y revenue increase, to $2.84 billion. But a bit of fog did worry some investors – the company’s EPS turned negative in early 2021 and the Twilio posted a per-share loss of 20 cents in Q4. This compared unfavorably to the 4-cent profit reported in the year-ago quarter – although management said it expects the company to return to profitability in 1H23.

This coincided with a market macro trend that we just can’t avoid right now – high and rising inflation. This metric hit 8.4% annualized in March of this year, the worst since December 1981, and shows now sign of abating. In the last six to eight months, inflation has pushed investors away from growth-oriented tech stocks like Twilio. And one top analyst believes that, in this case, that push has been far too strong.

Cowen analyst Derrick Wood, rated 5-stars at TipRanks, writes of Twilio: “We think the stock remains deeply oversold. We see catalysts for multiple expansion including 1) organic growth acceleration in 2H on easier comps, rising traction with newer products & political traffic benefits; and 2) gross margin pressures abating and starting to strengthen. These two factors have been the biggest overhangs on the stock and we see a path for both to reverse as we navigate through the year, creating a compelling time to buy in our view.”

Unsurprisingly, Wood rates Twilio shares an Outperform (i.e. Buy) along with a $300 price target. Possible gains of 154% could be heading investors’ way should the target be met over the next 12 months. (To watch Wood’s track record, click here)

Even a quick glace at the consensus view on this one shows that Wall Street is in broad agreement with the bullish stance – Twilio has 25 reviews on record, with a 24 to 1 breakdown in favor of Buy over Hold backing up the Strong Buy consensus view. The stock is selling for $118.03 and its $297.58 average price target suggests it has room for 152% share appreciation in the coming year. (See TWLO stock forecast on TipRanks)

Western Alliance (WAL)

Now we’ll turn to Western Alliance, a bank holding company who main subsidiary, Western Alliance Bank, focuses its operations on business clients. The company’s operations are mainly located in the Western US, where its serves its customer both online and through a modest network of brick-and-mortar banking offices. The company is based in Phoenix, Arizona.

Western’s stock has been falling in recent months, dropping 36% from the peak it reached in January of this year. In large part, this drop is reflecting a general worry about the US economy going forward. Recent government data showed that 1Q22 GDP contracted by 1.4%, in sharp turnaround from the near-7% growth in Q4 of 2021. The banking sector was among those hard hit.

At the same time, Western Alliance reported some solid data in its 1Q22 financial release. The bank saw its balance sheet grow to more than $60 billion in total assets, growth that included an additional $2 billion in loans and $4.5 billion in deposits. The two key banking metrics were up year-over-year by 43% and 35%, respectively. The bank’s net income in Q1 hit $240.1 million, for an EPS of $2.22. This EPS result, while down slightly from Q4, was still up an impressive 51% y/y.

This lends itself to Piper Sandler analyst Brad Milsaps’ conclusion that the pullback represents an attractive entry point. He says bluntly: “We simply think the stock remains oversold at less than 8x our 2022E and 7x our 2023E, especially since we expect WAL to continue generating above peer growth and profitability in both 2022 and 2023.”

“In our view, achieving $9.80 in EPS would be ideal, but the stock at $78 still looks way oversold even at something less than $9.80 as we think there is positive risk/reward with a decent margin for error,” Milsaps added.

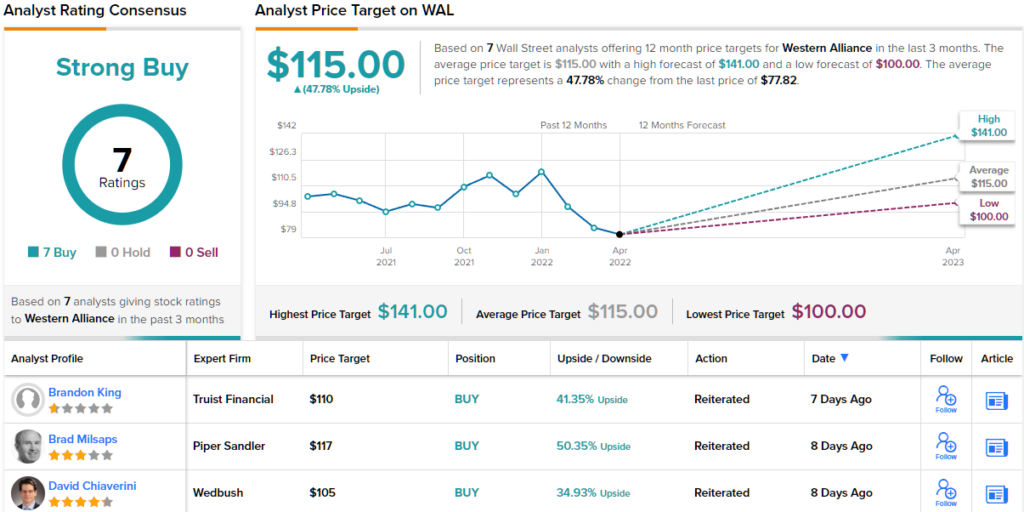

Looking forward, Milsaps rates the stock as Overweight (or, Buy), with a $117 price target to indicate a 50% upside for the next 12 months. (To watch Milsaps’ track record, click here)

Western Alliance may be a smaller regional bank, but it has still picked up interest from 7 Wall Street analysts, whose reviews are uniformly positive and give the stock a unanimous Strong Buy consensus rating. The average price target of $115 suggests ~48% upside from the current trading level of $77.82. (See WAL stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.