Investors know that the key to profits is in the return – and that means, a willingness to shoulder risk. Risk is relative, of course, and tends to run hand-in-hand with the return potential. Find a stock with a giant return potential, and chances are, you’ve also found one with a higher risk profile.

The highest returns usually come along with the lowest share prices. After all, when a stock is priced for just pennies, even a small gain in share price translates into a huge return. Which means that penny stocks – these days, usually seen as those equities priced under $5 – combine a perfect storm of market attractions: low share price, high return potential, and higher than usual risk.

Given the nature of these investments, Wall Street analysts recommend doing some due diligence before pulling the trigger, noting that not all penny stocks are bound for greatness.

With this in mind, we set out our own search for compelling investments that are set to boom. Using TipRanks’ database, we pulled two penny stocks that have amassed enough analyst support to earn a “Strong Buy” consensus rating. Adding to the good news, each pick boasts over 200% upside potential.

Lineage Cell Therapeutics (LCTX)

First up is Lineage Cell Therapeutics, a clinical-stage biotech firm working on new cell therapies for the treatment of serious medical conditions with high unmet needs. Specifically, the company uses a proprietary platform to develop ‘specialized, terminally-differentiated human cells’ from a variety of progenitors; the end cells can be used to treat disease conditions by replacing or supporting affected cells and tissues. The company aims to treat, or even reverse, degenerative diseases or traumatic injuries.

Lineage has based its program on an infinitely reproducible cell line, and works to develop cell therapies for retinal conditions and photoreceptors, spinal cord damage, auditory neurons, and immune conditions. The company has 5 research programs, two at preclinical stages and three in human clinical trials. The lead candidates are OpRegen, under development in partnership with Roche affiliate Genentech, and the spine injury treatment OPC1.

OpRegen is currently undergoing Phase 2 trials, and 24 patients have been treated. The drug candidate is designed for administration as a single dose, for the treatment of eye disorders, including advanced dry age-related macular degeneration (dry AMD) with geographic atrophy (GA). These are both severe conditions, with large addressable markets. Lineage received a $50 million upfront payment from Genentech earlier this year, and stands to receive up to $670 million in royalties through the partnership.

The second leading candidate, which has been used to treat 30 patients, is OPC1, a new potential treatment for spinal cord injuries. OPC1 is designed to treat the loss of function associated with spinal cord injury, and is currently undergoing a Phase 1/2a multicenter clinical trial.

Covering Lineage for Baird, analyst Jack Allen sees plenty of profit potential here for investors. As he explains, “With an estimated ~2.5M GA patient in the developed markets and no approved treatments for this disease we believe that Roche’s annual sales of this asset could easily top $4B. This could translate to over $500M in annual royalties to Lineage, a dynamic that should drive significant upside from the current ~$250M market capitalization in the long term.”

The analyst added, “We are very encouraged by the initial data from the OpRegen program and note that the observed functional benefit with this treatment is a key differentiator…We are encouraged by Lineage’s ability to create fully differentiated, pure, allogeneic cell therapies and note that the current programs may only represent the tip of the iceberg as to what is possible with these types of regenerative medicines.”

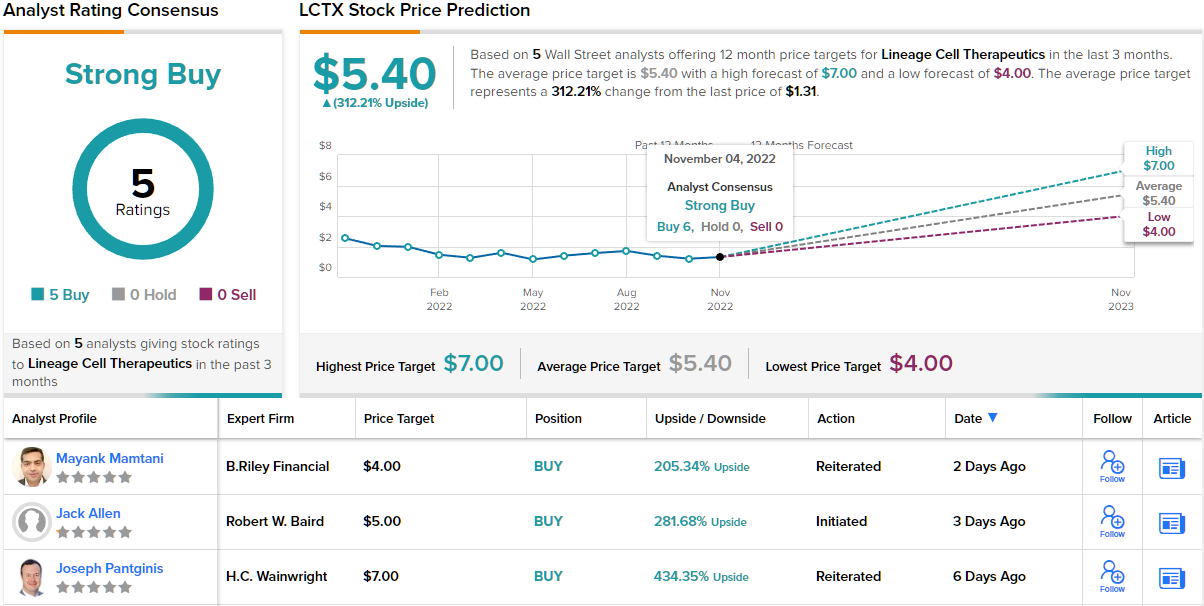

Based on the potential of OpRegen, and Lineage’s $1.30 share price, Allen thinks that now is the time to get in on the action. The analyst rates the stock an Outperform (i.e. Buy), and his price target, set at $5, suggests the stock will gain an impressive 281% in the next 12 months. (To watch Allen’s track record, click here)

Some stocks just manage to press all the buttons with the analysts, and Lineage has managed that – and picked up 5 positive reviews from the stock pros. These add up to a Strong Buy consensus rating, and the $5.40 average price target implies a bullish 312% upside on the one-year time horizon. (See LCTX stock forecast on TipRanks)

Graphite Bio (GRPH)

The second penny stock we’ll look at is Graphite Bio, a clinical stage biotech company focused on next-generation gene-editing technology to use in the development of curative therapies for a wide range of severe and/or life-threatening diseases, especially genetic diseases. The company uses its UltraDRTM gene editing platform to design precise corrections for any genetic mutation, which can then be precisely inserted into the disease-causing gene, replacing the flawed genes with functional copies.

Graphite Bio’s pipeline includes four tracks, two of which are still in discover stages. The third, GPH102, is a potential treatment for the blood condition beta-thalassemia, and is at the IND enabling stage. The real excitement in this stock comes from the fourth drug candidate, Nulabeglogene autogedtemcel, or nula-cel, which is undergoing human clinical trials as a treatment for the genetic-based sickle cell blood disorder.

Sickle cell disease, or SCD, is the most widespread monogenic disease worldwide, and affects over 100,000 people in the US alone. Nula-cel aims to correct the underlying mutation that causes the disease, by directly inserted functional genes and restoring the expression of healthy hemoglobin proteins. Nula-cel is currently in a Phase 1/2 clinical trial, CEDAR, an open label trial designed to evaluate safety, gene correction, and hemoglobin expression, prior to larger trials. Proof-of-concept data is expected for release in the middle of next year.

Cantor analyst Olivia Brayer is impressed by this small-cap firm’s prospects going forward, noting: “The team has made continued progress with its ongoing phase 1 clinical program for its lead clinical asset nula-cel. We’re still another 6+ months away from getting a look under the hood, with first phase 1 data still on track for mid-2023, but this is a name we’d flag as one worth another look as investors position for 2023 into what could be a major run-up into the readout.”

“Safety will be the biggest focus, but we think Graphite could show some early signs of direct elimination of the sickle globin, which may demonstrate some early clinical differentiation and could be a major inflection point for the stock’s valuation next year,” the analyst added.

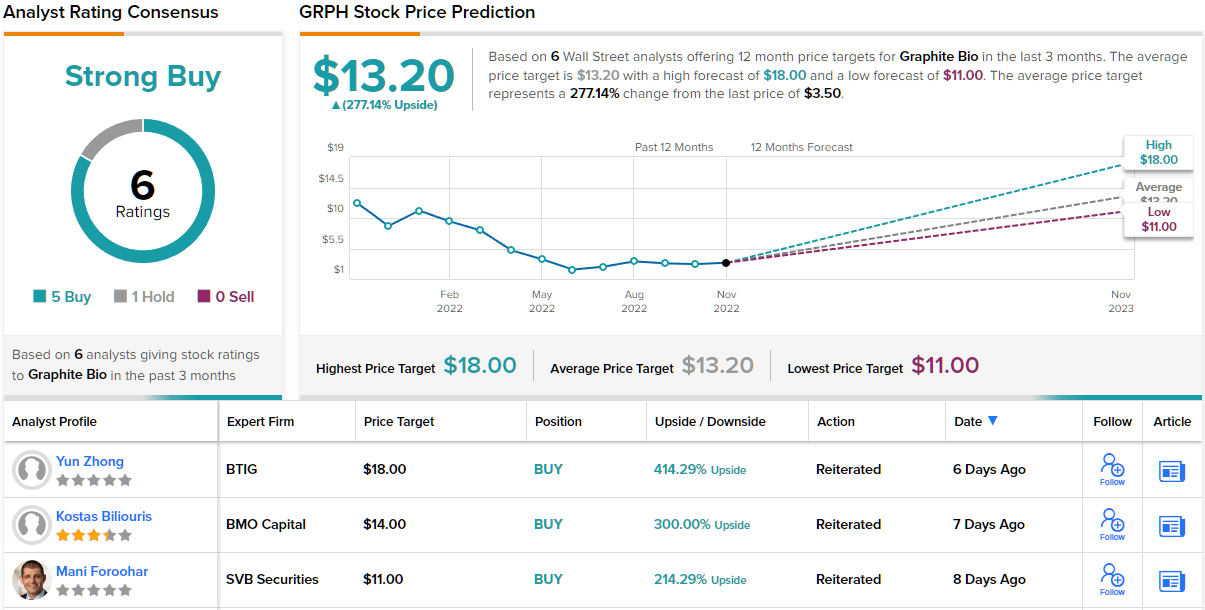

Quantifying her bullish stance, Brayer rates GRPH shares an Overweight (i.e. Buy), and her price target of $12 indicates her confidence in a strong 12-month gain of 242%. (To watch Brayer’s track record, click here)

Overall, of the 6 analysts who’ve filed recent reviews on this stock, 5 have come down as Buys and 1 as a Hold (i.e. Neutral) – for a Strong Buy consensus rating. The shares have a current trading price of $3.50 and their $13.20 average price target implies a jump of 277% going out to one year. (See GRPH stock forecast on TipRanks)

To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.