As we approach mid-year, it’s time to take stock of the oil markets. Prices are up, near $119 per barrel of crude oil right now, and indications are that they’ll keep going up. Industry experts are predicting a rise to $150 per barrel, but in quiet tones and small print they’re indicating chances for $175 or even $180 by year’s end, with high prices continuing into next year.

If they’re right, then markets generally are in for a shock. Oil – and energy, generally – are upstream of everything else; what happens to oil and its refined fuels will trickle down through almost the entire economy. As the price of crude goes up, as demand increases, and as refining capacity remains static, the conditions are set for record-high prices in petroleum and its refined fuels.

For retail investors, an environment like this brings home the need for expert advice, from a market expert who has made a career of studying the oil and energy industry. Analyst John Freeman, from Raymond James, is the man to turn to – and he’s not only an oil expert, he’s also one of the best analysts on Wall Street. Freeman holds the #3 overall ranking from TipRanks, out of more than 7,880 analysts. He’s build his reputation on his thorough examinations of energy and oil stocks, and has racked up a 67% success rate and a 41% average return from his recommendations.

We can use the database at TipRanks to look up the details on some of Freeman’s recent oil industry stock picks. These are stocks with Buy ratings, and offering investors double-digit upside potentials. Let’s get into those details, and find out what Wall Street’s #3 analyst has to say about them.

Marathon Oil Corporation (MRO)

The first oil stock we’re looking at is Marathon Oil Corporation, the exploration and production spin-off from Marathon Petroleum. Marathon Oil has been operating independently for the past 11 years, and focuses its operations in several of the country’s best-known oil-producing regions, including the Eagle Ford shale in Texas, the Permian Basin in New Mexico, the STACK and SCOOP plays in Oklahoma, and the Bakken fields in North Dakota. The Houston-based company’s hydrocarbon portfolio is comprised 50-50 in petroleum and natural gas assets.

Since seeing its activities bottom out in 2Q20, at the worst of the COVID crisis, Marathon Oil has experienced 7 quarters in a row of sequential revenue gains. The company has found support in both increased demand and increased prices. In 1Q22, the most recent reported, Marathon Oil showed $1.75 billion in total revenues, and an adjusted net income per diluted share of $1.02. Year-over-year, the revenue number was up 48%, and EPS was up an astounding 363%. Earnings came in ahead of the 96-cent EPS expected.

Marathon Oil earned these results with solid production numbers. Total Q1 production came to 281,000 barrels of oil equivalent per day (boed) net, of which some 158,000 was barrels of oil per day. US unit production costs in the first quarter, per parrel of oil equivalent, came to $5.59. Marathon Oil’s best-producing operational area was North Dakota’s Bakken, which generated 118,000 boed.

Of interest to investors, Marathon Oil has an active policy of returning profits to shareholders through dividends and buybacks. The program is weighted toward the buybacks; the 8-cent per common share dividend represents a modest yield of just 1.1%. The buybacks, however, have totaled more than $1.6 billion since last fall, and are currently driving a 16% shareholder cash return.

This the key point in Freeman’s take on MRO stock, as he writes: “MRO once again exceeded our expectations when it came to share buybacks during the quarter, repurchasing nearly $600m of shares (~15% above what we modeled). MRO has promised to repay 40% of cash from operations using the base dividend and buybacks, but exceeded that mark considerably paying out 50%, now averaging ~60% of CFO returned to shareholders in the last two quarters or ~80% of FCF.”

“Given their continued outperformance, we are expecting MRO to continue paying 50% or more of CFO during 2022. We are now anticipating cash returns of ~$2.7B for a yield of ~15% at the current strip. Keep in mind, even at these elevated cash return levels, we are still modeling a fairly substantial cash build in 2022 leaving the door open for further upside,” the top analyst added.

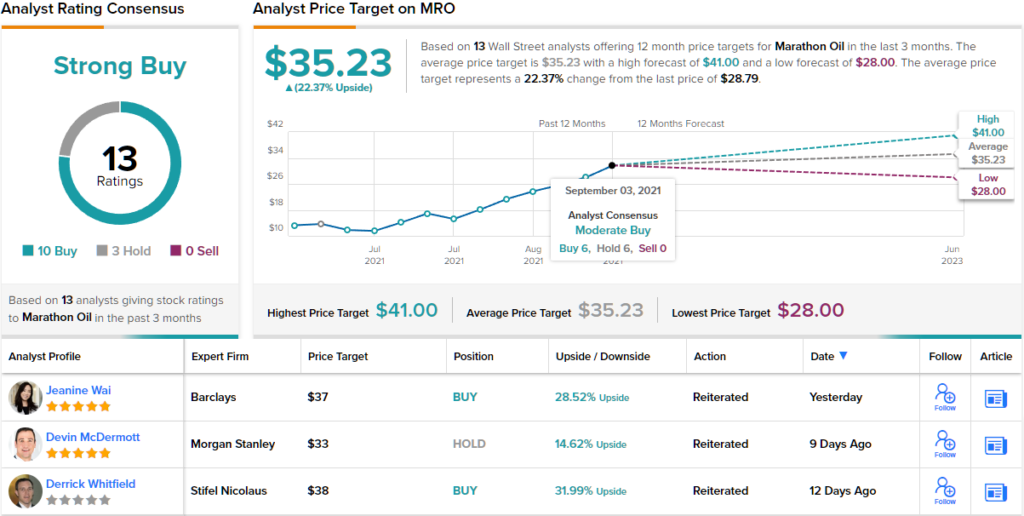

Considering the strong upside for return-minded investors, and the company’s potential for continued gains, Freeman rates MRO shares as a Strong Buy, and his $40 price target indicates room for ~39% share appreciation in the year ahead. (To watch Freeman’s track record, click here)

Overall, this high-performing oil company as attracted a lot of interest on the Street, where no fewer than 13 analysts have filed recent reviews. These break down to 10 Buys and 3 Holds, for a consensus rating of Strong Buy. MRO shares are up 76% this year, and their $35.23 average price target implies additional upside of ~22%. (See MRO stock forecast on TipRanks)

Pioneer Natural Resources (PXD)

Next up is Pioneer Natural Resources, another hydrocarbon company working to exploit the Texas oil fields. Pioneer’s production areas are centered on the Texas side of the Permian Basin, where production generated average daily sales of 637,756 barrels of oil equivalent per day in 1Q22. This generated $6.17 billion in top line revenue for Q1 – and marked the seventh straight quarter of revenue increases.

In addition to high revenues, Pioneer has seen a strong cash flow, with the Q1 free cash flow hitting $2.3 billion. The company returned some 88% of that cash directly to investors during the quarter, in part through $250 million worth of share repurchases, but mainly through a high dividend. Counting base-plus-variable, PXD paid out $7.38 per common share in dividends for the quarter, for a yield of 11%.

All of this has investors interested in Pioneer’s stock, and the shares have been strongly outperforming the markets. Where the S&P 500 has fallen 22% so far this year – putting it into bear market territory – PXD is up 52%. As with Marathon Oil above, Pioneer is finding support from both customer demand rebounding as COVID recedes and from the current high price regime in the oil markets.

Turning again to Raymond James’ Freeman, we find that he is highly impressed with Pioneer’s free cash flow, and its dividend policy. In Freeman’s words, “Pioneer remains a free cash flow machine with what should be easily the highest dividend yield in the S&P 500 this year… In addition to dividends, PXD continued to utilize share buybacks after spending another $250M on repurchases during 1Q. We anticipate buybacks will continue at a similar pace resulting in an extra $1B returned to shareholders in 2022. PXD’s incredible balance sheet, shareholder return program, and unhedged philosophy has them pegged as one of our favorites in the space.”

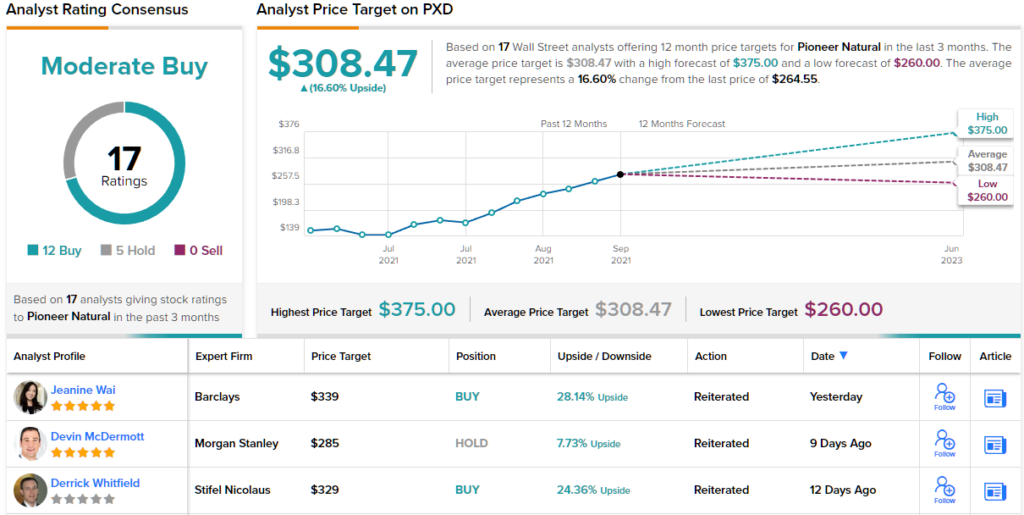

Freeman isn’t shy about where these comments lead, and rates PXD shares as a Strong Buy. His price target is $375, suggesting a 42% upside over the next 12 months. Based on the current dividend yield and the expected price appreciation, the stock has ~53% potential total return profile.

Looking at the consensus breakdown, with 12 Buys and 5 Holds, the analysts rate this stock a Moderate Buy. Given the average price target stands at $308.47, shares are anticipated to appreciate ~17% in the year ahead. (See PXD stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.