We all know how the stock market started out 2022 with a sudden reversal of last year’s bull run. By the end of February, it was clear that stocks had entered correction territory; the sell-off was broad-based, across all segments of the market.

But is the sell-off over? There are indications that may be the case. Since bottoming out on March 14, the market has staged a strong rebound, and year-to-date is no longer in correction territory. The S&P 500 is up 10% in that period, and the NASDAQ, which had fallen further, has bounced some 15%.

Swings of this nature and magnitude will leave investors with plenty of opportunities – in stocks that are oversold, yet poised to join the bounce.

With this in mind, we scoured the TipRanks database and picked out two names which have been heading south recently, specifically ones which have been flagged by those in the know as oversold. Not to mention substantial upside potential is on the table here. Let’s take a closer look.

Cellectis SA (CLLS)

The first beaten-down stock we’ll look at, Cellectis, is a Paris-based biopharmaceutical company working in the immunotherapy field, seeking new treatments for cancer. Cellectis focuses its efforts on the development of chimeric antigen receptor (CAR) T cells, a mode of attack on cancer that aims to use the patient’s own immune system to fight tumor growth. The company is developing its pipeline through its proprietary gene editing platform, TALEN, with the eventual goal of creating a line of ‘off the shelf’ anti-cancer therapies.

Cellectis is using its TALEN platform to create the UCART line of allogenic product candidates. These CAR T cell drugs are intended to meet multiple needs, giving them an important advantage over other therapies, which must be customer designed to each patient.

The company currently has three wholly controlled clinical programs in progress, each testing a drug candidate in the UCART line. UCART22, the first of these, is the subject of the BALLI-01 clinical trial. This study is evaluating the drug as a treatment for relapsed or refractory B-cell acute lymphoblastic leukemia. The company is currently enrolling patients for the trial, and has plans to begin dosing them in 2H22.

Also in active clinical trials are UCART123 and UCARTS1. These trials, titled AMELI-01 and MELANI-01, will evaluate the drug candidates as treatments for acute myeloid leukemia and multiple myeloma, respectively. Both trials are currently enrolling patients prior to dosing.

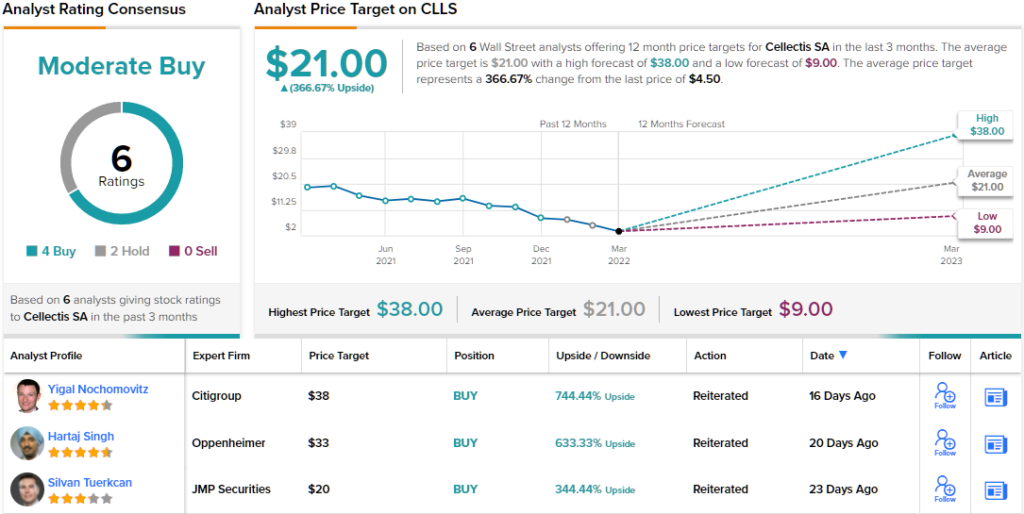

Cellectis reported finishing 2021 with $191 million in total cash assets on hand. Management estimated that these assets are able to support company operations through the end of 2023. Despite having a solid research pipeline, and sufficient assets to fund it, Cellectis shares are currently down 48% year-to-date.

Oppenheimer analyst Hartaj Singh doesn’t beat around the bush on this stock. He’s bullish, and writes bluntly: “CLLS’s share price has been volatile the past eight quarters; partly due to underperformance in biotech generally and a general lack of material clinical catalysts. We believe the stock is oversold and astute investors who want to own an allogeneic CAR-T leader, with a platform technology and multiple clinical projects should be buyers.”

Singh’s comments back up his Outperform (i.e. Buy) rating, and his $33 price target implies a robust upside potential of 633% for the next 12 months. (To watch Singh’s track record, click here)

While Singh is bullish, he is not alone in seeing the upside to this stock. Cellectis has picked up 6 recent analyst reviews, including 4 to Buy and 2 to Hold, giving it a Moderate Buy consensus rating. The shares are selling for $4.50 and their $21 average price target suggests a one-year upside of ~367%. (See CLLS stock forecast on TipRanks)

Laird Superfood (LSF)

Now let’s turn to the dietary supplement sector, with Laird Superfood. Founded by surfing champ Laird Hamilton in 2015, this company develops, produces, markets, and distributes a range of nutrient-dense plant-based food additives and snacks, designed to give consumers a natural boost of energy through the day. The company best-known products are its line of non-dairy coffee creamers. Laird’s target audience are consumers looking for a combination of energy and nutrition to add to their normal diet.

Since going public in September of 2020, Laird has consistently run a quarterly net loss. In the most recent quarterly report, for 4Q21, the net loss per diluted share came to 76 cents – this was the second-deepest quarterly EPS loss of the 6 that Laird has reported as a public entity. On the positive side, Q4 revenues, at $9.4 million, were up 29% year-over-year. For the fiscal year 2021, Laird reported total sales of $36.8 million, an increase of 43% y/y.

Looking forward, company management is guiding toward $41 million to $44 million in full-year revenue for 2022. At the midpoint, this represents a 15% increase from the 2021 results.

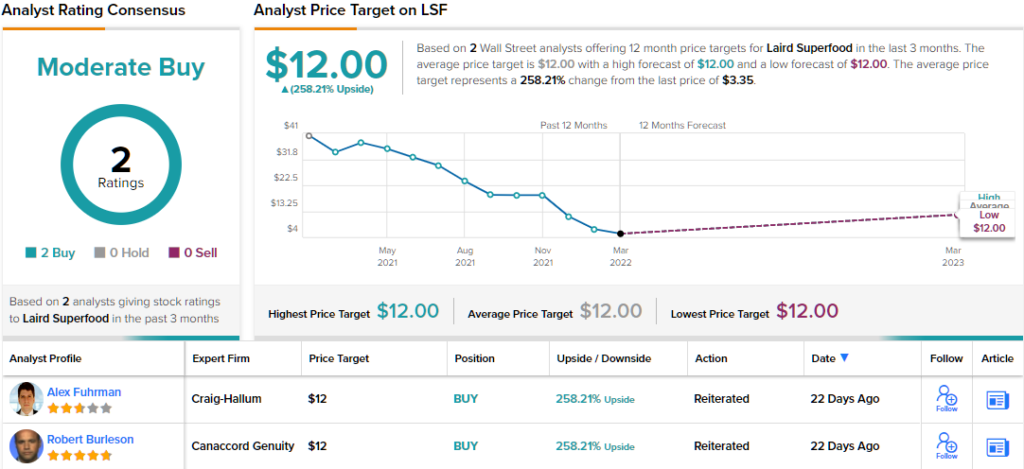

Laird shares are down sharply this year, losing 74%. Yet, one analyst thinks there’s significant upside ahead for the stock.

Craig-Hallum’s Alex Fuhrman takes an upbeat stance on the company, noting: “With more than half of its market cap in cash and revenue growing double-digits, we think the stock is oversold. Laird Superfood has a unique and differentiated portfolio of plant-based food and beverage products and a multi-channel distribution model that positions the brand for years of double-digit growth driven by grocery stores, e-commerce, coffee shops, and other retailers.”

Standing squarely in the bull camp, Fuhrman rates LSF a Buy, and his $12 price target implies a robust upside of 258% for the next 12 months. (To watch Fuhrman’s track record, click here)

Laird has slipped under most analysts’ radar; the stock’s Moderate Buy consensus is based on just two recent positive ratings. The shares are priced at $3.35 and their $12 average price target matches Fuhrman’s objective, in predicting a 258% upside. (See LSF stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.