Canada is both a vast geographical expanse and a state of mind worth guarding; it is also a behemoth in the world energy industry. Energy, generally, accounts for 900,000 jobs in the Canadian economy, and makes up more than 10% of the country’s total GDP. Canada is the world’s fourth largest producer of natural gas, and third largest producer of crude oil. Hydrocarbons are big business in the snowy north.

Toronto-based banking giant RBC, the Royal Bank of Canada, is immersed in the Canadian financial sector, with a vested interest in the country’s success. The bank has just released its latest report detailing its Global Energy Best Ideas. These are the go-to energy choices for RBC’s cadre of analysts; they don’t confine themselves to the Canadian landscape, but they don’t ignore it either.

We’ve looked up two of RBC’s choices in the TipRanks database to find out what makes them so compelling – the dividends stood out. These stocks offer investors returns ranging from 5% to nearly 8%. Adding to the good news, each boasts over 30% upside potential.

TC Energy Corporation (TRP)

First on our list, TC Energy operates a network of hydrocarbon facilities across North America. The company’s natural gas and crude oil pipeline networks extend from British Columbia, across Canada and the ‘Lower 48,’ and down to the Gulf Coast of Louisiana and Mexico. In addition, the company’s Energy division generates 6,600 megawatts of electricity for the North American grid.

Inhabiting an economically essential niche helped insulate TRP from the disruptions of the first quarter. While the coronavirus-inspired shutdowns hurt most companies at both the top and bottom line, TC Energy reported an increase in earnings attributable to common shares, to a total of $1.15 billion. Net cash for the quarter, from operations, came to $1.7 billion. Success in the pipeline business contributed to the forecast-beating quarterly results, especially continued progress on the US-Canadian Keystone XL project.

The company used its high earnings to fund a 56.5-cent per share dividend in the quarter. Annualizing to $2.26, the payment gives the stock a dividend yield of 5.3%, providing a steady income stream for return-minded investors.

Representing RBC, 5-star analyst Robert Kwan describes TC Energy as having “numerous avenues for growth.” He elaborates, “The company’s assets provide a competitive advantage in winning new projects to lever off the existing ‘steel in the ground’ (i.e., in- corridor expansions). Typically, these are projects of smaller size that often ‘fly under the radar’ but also generate above-average returns given that they expand or extend existing infrastructure.”

Kwan’s price target here, of $81 Canadian ($59.61 in US currency), implies an upside potential of 38% for the coming year. (To watch Kwan’s track record, click here)

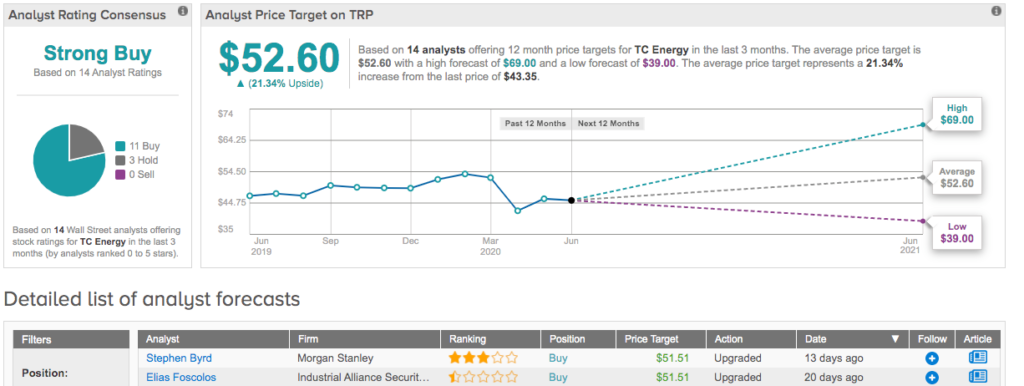

With 14 analyst ratings on record, including 11 Buys and 3 Holds, the analyst consensus rating on TRP is a Strong Buy. The stock is trading for US$43.35, and the average price target, at US$52.60, suggests it has room for 21% upside growth. (See TC Energy stock analysis on TipRanks)

Williams Companies, Inc. (WMB)

Heading south to Tulsa, Oklahoma, the next stock on our list is Williams Companies. Like TC Energy, Williams primarily processes and transports natural gas, but its business model also includes crude oil and energy generation capacity. WMB controls gas pipelines connecting production fields in the central Rockies with the Pacific Northwest, and fields in Appalachia and Texas with the Northeast and the Gulf Coast. Approximately one-third of all US commercial and residential natural gas is handled by Williams.

The Q1 report showed some mixed results for WMB. Quarterly revenues were down 6.8% year-over-year, from $2.05 billion to $1.91 billion, but EPS beat the forecast. Earnings, at 26 cents per share, came in one penny over the estimates. Overall, the earnings report was seen as a net positive, as it was generally in-line with expectations.

That management felt confident, despite the coronavirus pandemic, was evident in the dividend. The company raised the quarterly payment in Q1, continuing its pattern of starting the year with a dividend increase, and has maintained the payment for the Q2 dividend, already announced for the end of June. At 40 cents, the dividend gives an annualized payment of $1.60 and a yield of 8.8%. For comparison, the services sector, where Williams Companies resides, has an average dividend yield of only 1.37%.

TJ Schultz, another 5-star analyst from RBC, is impressed with WMB’s balance sheet and increasing cash flow. He writes of the stock, “Despite moderating NE gathered volume growth, we still expect WMB to deliver stable cash flow in 2020 and 2021. With this, we think WMB will remain safely within IG metrics, as it should post positive FCF this year (after capex and dividends).”

As a result, Schultz rates the stock a Buy, and his $25 price target implies a 37% upside potential in the next 12 months. (To watch Schultz’s track record, click here)

The Strong Buy analyst consensus rating on WMB is based on 9 Buys and 2 Holds, showing that Wall Street for the most part agrees with Schultz’s assessment. The average price target, $21.73, indicates a 19% upside potential from the current share price of $18.23. (See Williams Companies stock analysis on TipRanks)