Making investments pay out for the long term is the true challenge in today’s market environment. The series of headwinds piling up – from persistently high inflation to rising interest rates to slowing demand to bureaucratic bloat – are rising to hurricane force, and renewing investors’ attention to defensive stocks.

It’s only logical. The classic defensive stock, the dividend payer, ensures an income stream no matter how the markets move, and if the yield is high enough, these stocks can also generate a real rate of return despite inflation.

Knowing all this, wouldn’t you like to own find great dividend stocks? Of course you would!

Using the TipRanks database, we’ve looked up two stocks that are offering dividends of at least 10% yield – that’s more than 4x higher the average yield found in the markets today. Each of these is Strong Buy-rated, with some positive analyst reviews on record, and best of all, they all offer investors a low cost of entry, under $10 per share. Let’s take a closer look.

Oaktree Specialty Lending (OCSL)

First up on our short list, Oaktree Specialty Lending, is a provider of credit and loan products for mid-market enterprises, the small business segment that long been the engine of American ingenuity and economic success. Oaktree, which has a market cap of $1.14 billion and annual revenues above $230 million, generates its income through the success of its investment portfolio.

As of June 30 this year, Oaktree’s investment portfolio includes 151 companies, into which Oaktree has put more than $2.6 billion. Oaktree’s portfolio is primarily made up of floating-rate investments, which compose 88% of the total. More than 15% of Oaktree’s investment are in the application software segment, with other segments, including pharmaceuticals, data processing, biotech, and health care, making up smaller shares of the total.

It’s a profitable portfolio, and Oaktree’s most recent quarterly financial release, from Q3 of fiscal year 2022 – the quarter ending on June 30 – showed that the company generated solid earnings. By GAAP measures, net investment income was $40.4 million for the quarter, or 22 cents per share, up 10% year-over-year, and well above the 18-cent forecast.

Of particular interest to dividend investors, Oaktree had cash and liquid assets totaling $34.3 million at the end of the quarter, and had undrawn credit up to $455 million. This cash backing made it possible for management to raise the dividend in the Q3 declaration, bumping it up 3% to 17 cents per common share. This was the 9th quarter in a row that the dividend was raised, and the new rate was paid out on September 30.

The dividend annualizes to 68 cents per common share – and while that sounds modest, it represents a solid yield of 10.9%.

Also of note to investors, Oaktree Specialty Lending has entered into an agreement to merge with Oaktree Strategic Income II, subject Board approvals. The merger will create a combined entity, using the OCSL name and stock ticker, with a portfolio valued at more than $3 billion, and with improvements in market cap and credit quality.

JMP analyst Kevin Fultz has delved into this merger, and writes, “We believe the rationale is sound and view the merger as favorable to shareholders of OCSL as the combined company will benefit from: 1) the increased scale of $3.3B of total assets, which would create a top ten publicly traded BDC by total assets; 2) a larger market capitalization which could lead to greater trading liquidity and institutional ownership; 3) the combination of two known, complimentary investment portfolios with significant investment overlap, which we think will result in a seamless portfolio integration; 4) the larger scale of OCSL may improve access to more diverse, lower cost sources of debt capital…”

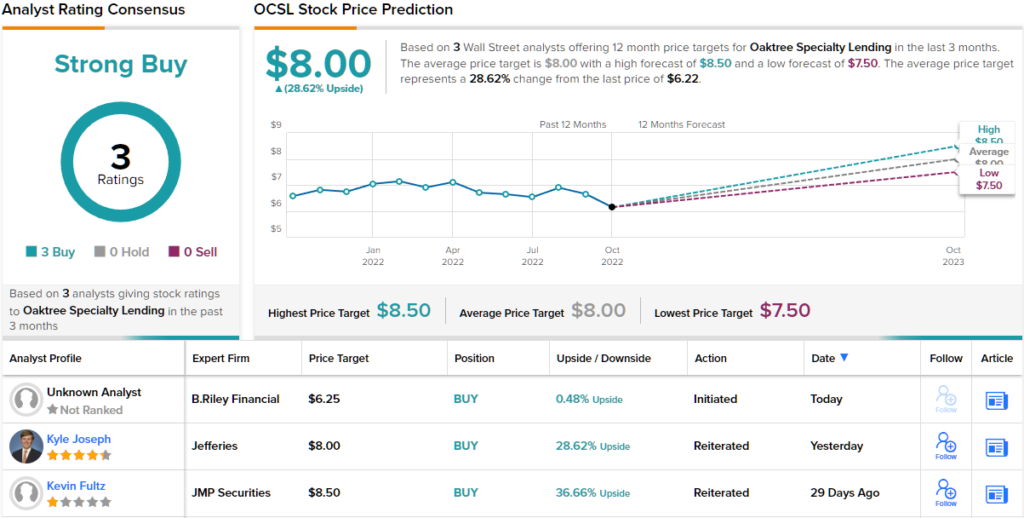

To this end, Fultz rates OCSL an Outperform (i.e. Buy) along with an $8.50 price target. If achieved, his target could offer a potential total return of ~48% with price appreciation of 37% and an annual yield of 10.9%. (To watch Fultz’s track record, click here)

While this small-cap specialty finance provider has only picked up 3 Wall Street reviews recently, these analysts all agree that this is a stock to buy, giving OCSL a Strong Buy consensus rating. The shares are priced at $6.22 and the $8 average target suggests ~29% upside on the one-year horizon. (See OCSL stock forecast on TipRanks)

Lument Finance Trust (LFT)

Next up is Lument Finance Trust, a micro-cap firm in the real estate investment trust (REIT) niche, investing in various forms of real estate, real property debt, and mortgage loans, primarily in the commercial property market. The company’s portfolio emphasizes mid-market multi-family assets, and includes other commercial property investments, such as mezzanine loans, preferred equity, and commercial MBSs. Lument looks to build a portfolio based on high-quality commercial real estate, and bases its time frame on three-year terms with options for two one-year extensions.

The quality portfolio has brought Lument generally rising revenues over the past two years. In the most recent quarter reported, 2Q22, the company had a top line of $12.6 million, which supported an income attributable to shareholders of $2.15 million – and a total distributable income of $2.45 million.

The distributable income matters to dividend investors, because it’s the metric that supports the quarterly dividend payment. As a REIT, Lument is required by tax regulations to return a high percentage of earnings directly to shareholders, and dividends are the usual mode of compliance. For Lument’s shareholders, this means a reliable long-term payment, with occasional adjustments to keep it affordable for the company. The last dividend declaration, from September 15, was for 6 cents per share, to be paid on October 17. At this rate, the annualized dividend is 24 cents per common share and yields 11.6%.

Among the bulls is Raymond James’s 5-star analyst Stephen Laws, who takes a bullish stance on LFT shares.

“We continue to expect distributable earnings to benefit from 1) increasing interest rates given the floating rate loan portfolio and 2) replenishing loan repayments in the CLO with newly originated, higher spread loans. We are maintaining our Outperform rating given the attractive portfolio characteristics, such as the high mix of multifamily, the floating rate portfolio, and the portfolio financing consisting entirely of CLO debt,” Laws wrote.

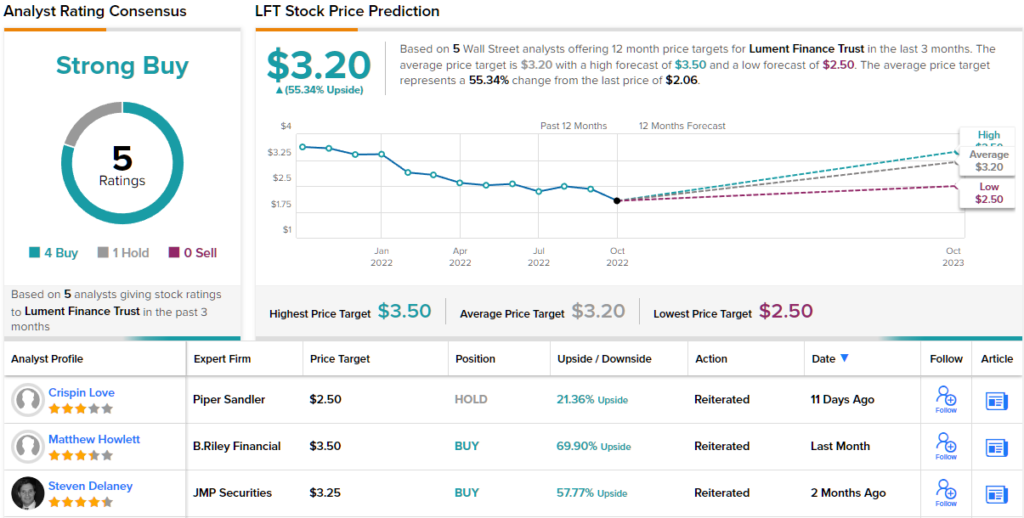

That Outperform (i.e., Buy) rating is backed by a $3.25 price target, suggesting a one-year gain of 57%. Based on the current dividend yield and the expected price appreciation, the stock has ~68% potential total return profile. (To watch Laws’ track record, click here)

All in all, five of the Street’s analysts have chimed in on LFT, and their reviews include 4 to Buy and 1 to Hold, for a Strong Buy consensus. The average price target of $3.20 implies ~55% upside from the current trading price of $2.06. (See LFT stock forecast on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.