Earnings season is heating up with several of the tech giants poised to deliver their latest quarterly results this week. However, ahead of some big readouts, investors seem to be on edge about one particular standout group. In what amounted to a rare sight in recent times, chip stocks saw out last week taking a hit across the board, as the segment appeared to be entering correction mode.

Chipmakers have been among the market’s top performers, largely propelled by the surge in AI. Now, investors are left pondering whether the pullback signals a bit of a sea change or actually offers an opportunity to load up before the rocket takes off again.

Considering the growth opportunity AI represents, Evercore’s Mark Lipacis, an analyst whose stock rating exploits have landed him at 4th spot amongst the thousands of Wall Street stocks pros, lays out the bullish case for the sector.

“We observe compute revenues of main data center vendors grew at 13% CAGR for C2005 -2021,” says the 5-star analyst. “We expect data center processors market to continue growing at the same CAGR, but anticipate AI -related applications to account for most of the incremental growth…”

With this in mind, Lipacis has been pointing investors toward the best AI plays out there and he considers chip stalwarts Nvidia (NASDAQ:NVDA) and Advanced Micro Devices (NASDAQ:AMD) to be just that. So, let’s take a closer look at the pair to see what Lipacis finds appealing. And with some help from the TipRanks database, we can also gauge whether the rest of the Street agrees with his bullish take.

Nvidia

Possibly no company embodies the rise of AI better than Nvidia. It’s a name that’s been grabbing all the headlines since GenAI became a thing and it’s no wonder. Once essentially a semi company focused on developing top-notch GPU solutions for the gaming industry, Nvidia has grabbed the AI opportunity by the horns and that’s for a simple reason: it makes the best chips used in data centers powering the AI tech. Its dominance is such that it is currently estimated it has more than a 90% share of the AI chip market.

That superiority has been the reason behind the stock’s ascent, and which has taken its market cap to just under $2 trillion, making it the world’s fourth most valuable company. It has also been the reason why the firm has been delivering a set of earnings reports that at first seemed to stun Wall Street but have now almost become par for the course.

A look at the most recent print, for its fiscal fourth quarter (January quarter), gives an idea as to the scale of success the company is having in the field. Revenue climbed by 265.3% year-over-year to $22.1 billion, outpacing the Street’s call by $1.55 billion. If that seems impressive, consider that the data center segment’s revenue increased by 409% to a record $18.4 billion. The profitability profile showed similar strength, with adj. EPS of $5.16 beating the forecast by $0.52. And looking ahead to FQ1, revenue is expected to reach $24.0 billion, plus or minus 2%, compared to the $22.03 billion anticipated by the analysts.

While recently there have been murmurings that other rivals could yet eat away at Nvidia’s dominance with counter offerings or by making chips in-house, Evercore’s Lipacis thinks there’s plenty more to come from Nvidia.

“We think investors underestimate 1) the importance of the chip+hardware+software ecosystem that NVDA has created, 2) that computing eras last 15-20 years and are typically dominated by a single vertically integrated ecosystem company, whose returns are measured in 100-to-1000 bagger range,” Lipacis explained. “How large is the AI data center opportunity for NVDA? We think a $600bn opportunity by 2030, which we calculate by assuming processors continue to grow at 15% annually as they have grown for the past 15 years, and that ecosystem value captured in the software and hardware is equal to or greater than the value of the chips.”

Accordingly, Lipacis rates NVDA shares an Outperform (i.e., Buy), backed by a $1,160 price target, suggesting the shares will surge ~41% over the coming year. (To watch Lipacis’s track record, click here)

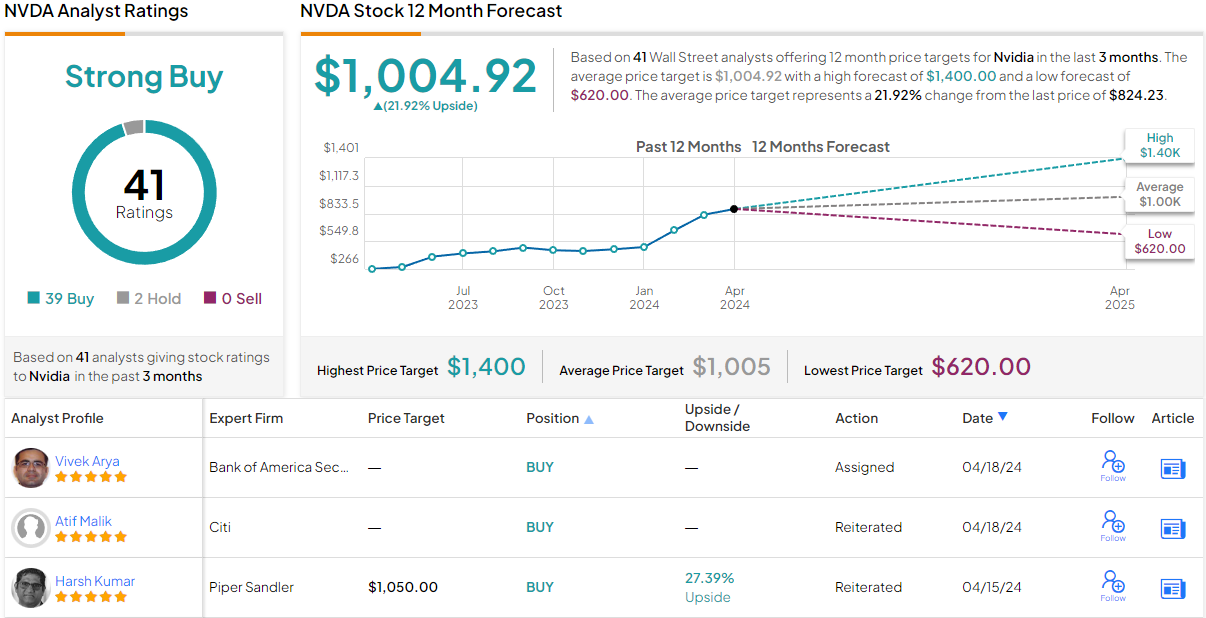

Overall, there are no fewer than 41 analyst reviews on file for NVDA, and they break down 39 to 2 in favor of Buys versus Holds. This indicates a broad view on Wall Street that the stock is a buying proposition, and makes the consensus rating a Strong Buy. Shares are priced at $824.23, and their $1,004.92 average price target suggests room for ~22% growth on the one-year time horizon. (See Nvidia stock forecast)

AMD

It’s become a bit of a cliché but talk of Nvidia often gets followed by a mention of AMD. That’s because this smaller yet still heavyweight-size chipmaker is often seen as the one company that might give Nvidia some stern competition in the AI chip segment by siphoning away some of its share.

Not for nothing is it looked at that way – because AMD has done just that before. Intel used to have absolute dibs on the CPU sector, but guided by Lisa Su, AMD took advantage of a series of missteps, offered superior products and closed the gap considerably on its once-far-bigger rival. So, it’s not out of the question it could offer a repeat scenario in the AI chip game.

While the top-line growth on tap has not been near the levels seen at Nvidia, it has been increasing at a steady pace over the past several quarters. The company’s most recent print, for 4Q23, saw revenue grow by 10.7% compared to the same period a year ago to $6.2 billion, edging ahead of the Street’s call by $60 million. Within that total haul, Data Center segment revenue generated $2.3 billion, amounting to a 38% YoY increase and a 43% sequential uptick. On the bottom-line, adj. EPS of $0.77 met analyst expectations. However, the outlook was a bit of a disappointment, with 1Q24 revenue anticipated to clock in at around $5.4 billion, plus or minus $300 million, at the midpoint below consensus at $5.57 billion.

That, though, is not much of a concern for Evercore’s Lipacis, who lays out the reasons why AMD’s prospects are sound.

“We see AMD as a beneficiary of the Tectonic Shift in Computing to Parallel Processing Era as it captures greater share of server CPUs as well as share in the merchant accelerator market with its Mi300 series products,” Lipacis explained. “We believe AMD is establishing itself as a solid 2nd source to NVDA in merchant accelerators, and that position could accelerate with progress on its chip+hardware+software ecosystem. We believe the bulk of XLNX revenue synergies remain on the come ($10B+) offering further upside over the longer-term.”

To this end, Lipacis rates AMD shares an Outperform (i.e. Buy) and his $200 price target implies ~31% upside from current levels.

Turning now to the rest of the Street, where once again, most agree with the Evercore view; based on a mix of 29 Buys vs. 6 Holds, the stock claims a Strong Buy consensus rating. The forecast calls for one-year gains of 33%, considering the average target currently stands at $202.81. (See AMD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.